PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844461

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844461

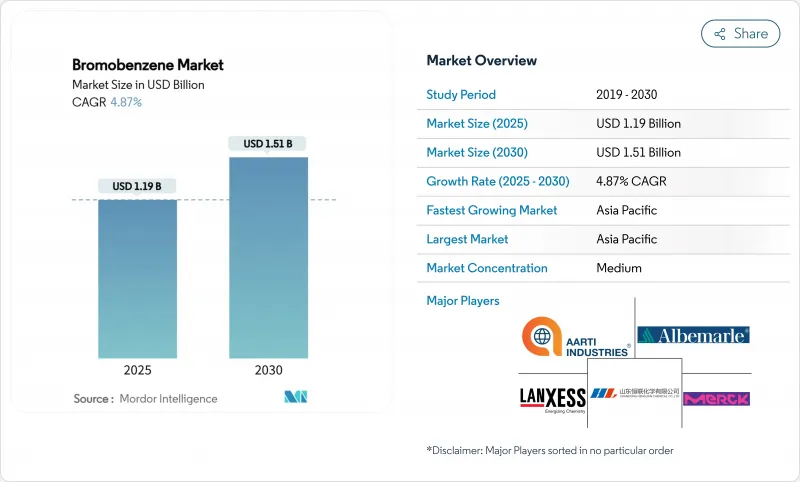

Bromobenzene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Bromobenzene Market size is estimated at USD 1.19 billion in 2025, and is expected to reach USD 1.51 billion by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

This expansion is rooted in bromobenzene's indispensable role as a Grignard reagent precursor that underpins high-value pharmaceutical intermediates and specialty chemicals. Continuous outsourcing of complex synthesis to contract manufacturing organizations, especially in Asia Pacific, keeps utilisation rates high while sustained semiconductor capital expenditure widens demand for electronics-grade solvent grades. Firms that integrate upstream bromine extraction with downstream bromobenzene processing maintain cost advantages that preserve margins in spite of raw-material price swings. Regulatory tightening in Europe and North America raises compliance costs, yet the compound's synthetic selectivity and lower volatility compared with many chlorinated analogues support a stable demand floor. The bromobenzene market also benefits from process innovations such as continuous-flow Grignard production that lift yields, curb waste, and open new application windows in advanced materials.

Global Bromobenzene Market Trends and Insights

Rising Pharmaceutical Outsourcing in Asia Pacific

Surging life-science outsourcing is reshaping bromobenzene demand profiles across India, China and Southeast Asia. Regional contract development and manufacturing organizations have scaled bromination and organometallic synthesis lines to secure Western supply contracts for psychoactive and oncology APIs. Regulatory harmonisation under ICH guidelines simplifies technology transfer while China's abundant bromine feedstock cuts logistics costs, reinforcing price competitiveness for downstream phenylmagnesium bromide production.

Expansion of Grignard-Based Manufacturing for High-Value Intermediates

Pharmaceutical, agrochemical, and materials firms are widening their use of Grignard cross-coupling to access complex scaffolds at higher throughput. Continuous-flow reactors raise space-time productivity and suppress side reactions, making bromobenzene-derived phenylmagnesium bromide a cost-efficient nucleophile for difficult carbon-carbon bond formations. Emerging rhodium-catalyzed homo-couplings extend bromobenzene's reach to integrin inhibitor syntheses and other frontier therapeutics.

Price Competition from Chlorinated Aromatics

Chlorobenzene's 15-20% price discount challenges bromobenzene adoption in cost-sensitive formulations. The differential widened in 2024 after bromine feedstock prices spiked on supply disruptions, prompting some formulators to redesign synthesis routes around chlorinated aromatics. Producers counter by highlighting bromobenzene's superior selectivity and lower reaction temperatures, yet aggressive price matching erodes margins.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for High-Purity Solvents in Electronics

- Surge in Contract Production of Psychoactive APIs

- Stricter REACH/TSCA Restrictions on Organobromines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phenylmagnesium bromide represented 43.22% of the bromobenzene market in 2024, underscoring its ubiquity as a Grignard reagent for carbon-bond construction across pharmaceutical and specialty-chemical workflows. Flow-chemistry retrofits improved space utilisation and cut solvent volumes, lifting reactor uptime for this marquee product. Pharmaceutical integrators continue to prioritise phenylmagnesium bromide procurement because substitutions often compromise yield or stereochemistry. This demand stability shields the bromobenzene market from wider organobromine volatility. Continuous process intensification and a patent-protected electrochemical bromination route capable of 90% Faradaic efficiency are poised to enhance competitiveness, yet entrenched batch methods remain dominant in many Asian plants.

Other products, including ortho- and para-brominated derivatives plus specialised research chemicals, together form a diversified tail that services agrochemical, material-science and fragrance intermediates. Although these niches are smaller in volume, they command higher per-kilogram margins that temper revenue cyclicality. Phencyclidine, holding 5.11% share, illustrates the pattern: tight regulatory controls constrain scale, yet recurring demand from validated therapeutic protocols keeps price realisations elevated. Over the long run, incremental gains in continuous-flow selectivity may allow small-volume products to chip away at phenylmagnesium bromide's share, but the broader bromobenzene market will likely remain product-concentrated through 2030.

The Bromobenzene Market Report is Segmented by Product (Phenylmagnesium Bromide, Phencyclidine, Other Products), Application (Grignard Reagent, Solvent, Chemical Intermediate, Pharmaceuticals, Electronics-Grade Solvents, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific, with a 42.14% share in 2024, is the operational and demand epicentre of the bromobenzene market. China is a significant producer of elemental bromine, which supports nearby bromobenzene and downstream phenylmagnesium bromide plants. These facilities cater to both local formulators and fulfill export contracts. India's Aarti Industries and other domestic groups are spending INR 1,500-1,800 crore on debottlenecking and backward integration to secure bromine availability and meet stricter impurity limits demanded by European buyers. Japanese and Korean electronics clusters generate incremental volumes for ultra-pure solvent grades. Southeast Asian countries add low-cost tolling capacity that supports the region's overall CAGR through 2030.

North America remains a critical technology hub for the bromobenzene market, even though its consumption is lower than Asia Pacific. The United States hosts advanced pharmaceutical research pipelines that specify bromobenzene-derived intermediates for next-generation oncology and CNS actives. Albemarle Corporation's brine operations in Arkansas strengthen local supply resilience and moderate price volatility. Canadian and Mexican buyers secure regional feedstock through spot imports, though their domestic production remains limited. Regulatory momentum under TSCA encourages investment in greener synthesis but also raises registration thresholds that smaller users find burdensome.

Europe operates under the strictest regulatory regime yet sustains specialty demand streams in high-value applications. German fine-chemical producers deploy closed-loop bromine recovery to curtail emissions, ensuring continuity of supply despite REACH dossier costs. Pharmaceutical multinationals headquartered in Switzerland, France, and the United Kingdom drive demand for GMP-grade bromobenzene intermediates used in small-batch, high-potency drug substances. Eastern European chemical parks attract contract formulations that benefit from lower labour costs and EU single-market access. Despite limited consumption in the Middle East and Africa, Jordan's significant bromine production capacity positions it as a pivotal regional raw-material hub, potentially spurring future bromobenzene projects. South America remains a small but rising consumer as Brazilian and Argentine agrochemical producers explore aromatic bromides for new active ingredients.

- Aarti Industries Limited

- Albemarle Corporation

- Exxon Mobil Chemical

- Hawks Chemical Company

- Heranba Industries Ltd

- Lanxess AG

- Merck KGaA

- Pragna Group

- Shandong Henglian Chemical Co. Ltd

- Shanghai Wescco Chemical Co. Ltd

- Sontara Organo Industries

- Zhejiang Xieshi New Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising pharmaceutical outsourcing in Asia Pacific

- 4.2.2 Expansion of Grignard-based manufacturing for high-value intermediates

- 4.2.3 Growing demand for high-purity solvents in electronics

- 4.2.4 Surge in contract production of psychoactive APIs

- 4.2.5 Transition to low-VOC solvents in coatings

- 4.3 Market Restraints

- 4.3.1 Price competition from chlorinated aromatics

- 4.3.2 Stricter REACH/TSCA restrictions on organobromines

- 4.3.3 Volatility in bromine supply from Dead Sea producers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Phenylmagnesium Bromide

- 5.1.2 Phencyclidine

- 5.1.3 Other Products

- 5.2 By Application

- 5.2.1 Grignard Reagent

- 5.2.2 Solvent

- 5.2.3 Chemical Intermediate

- 5.2.4 Pharmaceuticals

- 5.2.5 Electronics-grade Solvents

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aarti Industries Limited

- 6.4.2 Albemarle Corporation

- 6.4.3 Exxon Mobil Chemical

- 6.4.4 Hawks Chemical Company

- 6.4.5 Heranba Industries Ltd

- 6.4.6 Lanxess AG

- 6.4.7 Merck KGaA

- 6.4.8 Pragna Group

- 6.4.9 Shandong Henglian Chemical Co. Ltd

- 6.4.10 Shanghai Wescco Chemical Co. Ltd

- 6.4.11 Sontara Organo Industries

- 6.4.12 Zhejiang Xieshi New Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment