PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844463

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844463

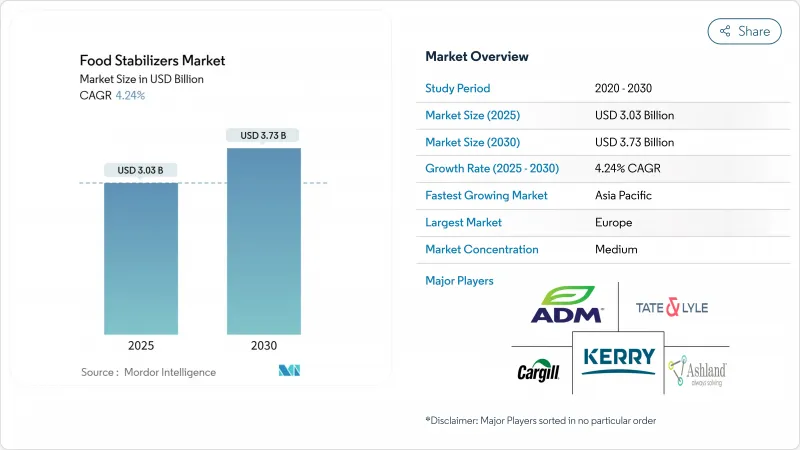

Food Stabilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The food stabilizers market size is valued at USD 3.03 billion in 2025 and is expected to reach USD 3.73 billion by 2030, growing at a CAGR of 4.24%.

Food processors drive demand as they reformulate products to achieve clean-label status while maintaining texture, shelf stability, and cost efficiency. The industry is shifting toward natural hydrocolloids, fermented gums, and modified lecithins as alternatives to synthetic emulsifiers, supported by global regulatory approval of plant-based and microbial additives. Sustainability considerations influence purchasing decisions, with increased preference for stabilizers derived from certified seaweed, recycled citrus fiber, and fermentation byproducts. Companies that combine product effectiveness with supply chain transparency gain long-term contracts, reducing their vulnerability to raw material price volatility and regulatory changes.

Global Food Stabilizers Market Trends and Insights

Surging demand for processed and convenience food globally

Urbanization and lifestyle changes are transforming food consumption patterns, driving increased processed food demand in emerging markets. This growth requires advanced stabilization technologies to maintain product quality throughout extended distribution chains and storage conditions. The rising preference for convenience foods increases the need for specialized stabilizers that withstand thermal processing while meeting clean-label requirements. The food industry continues to adapt to these evolving consumer preferences by developing innovative stabilization solutions. In Japan, the aging population is fueling demand for health-focused processed foods, with the USD 190 billion food processing industry emphasizing functional ingredients and shelf-stable products, according to the Ministry of Food Processing Industries' data from 2022. This demographic shift has prompted manufacturers to invest in research and development of stabilizers that can enhance nutritional value while extending product shelf life.

Consumer shift towards texture-enhanced clean label products

Growing health awareness among consumers is increasing the demand for transparency in food ingredients, including texture enhancers that can match the performance of synthetic additives. The focus has shifted beyond basic ingredient declarations to encompass natural texture enhancement solutions. This evolution reflects a broader industry movement toward clean-label formulations that meet consumer expectations. In 2024, Tate & Lyle introduced its formulation tool 'Tate & Lyle Sensation(TM)' to address the market need for texture optimization while maintaining clean-label standards. Rice and tapioca maltodextrin have emerged as functional substitutes for conventional stabilizers, offering thickening and binding properties without chemical modifications. These natural alternatives demonstrate versatility across various food applications, from bakery products to beverages. However, manufacturers face the challenge of achieving cost-effectiveness comparable to synthetic alternatives while ensuring consistent performance.

Regulatory compliance requirements impact food additives market

Escalating regulatory scrutiny is creating compliance complexities that constrain market growth and increase development costs across global markets. California's Food Safety Act banning four toxic additives, including potassium bromate and propylparaben, took effect in January 2025, triggering similar legislation in New York and Illinois. The European Union's updated novel food application guidance, effective February 2025, introduces enhanced requirements for microorganism-related foods, comprehensive composition data, and expanded toxicological assessments. China's implementation of food additive standard GB2760-2024 in February 2025 creates additional compliance burdens for global suppliers seeking market access. The FDA's Human Foods Program prioritizes food chemical safety in FY 2025, focusing on enhanced regulatory oversight of additives and contaminants. These regulatory developments extend product development timelines and increase costs, particularly for smaller companies lacking regulatory expertise and resources.

Other drivers and restraints analyzed in the detailed report include:

- Stabilizers extend product shelf life in food applications

- Emergence of stabilizer-infused functional confectionery

- Religious/ethical restrictions on animal-derived gelatin

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plant-based sources command 64.74% market share in 2024, reflecting established supply chains and consumer preference for recognizable natural ingredients. However, microbial sources represent the fastest-growing segment at 5.54% CAGR through 2030, driven by precision fermentation advances and sustainability advantages. Seaweed-derived stabilizers maintain steady demand, while synthetic alternatives face increasing regulatory and consumer pressure. Animal-derived sources continue declining as ethical and religious considerations drive substitution.

The microbial segment's growth acceleration stems from technological breakthroughs in fermentation efficiency and cost reduction. Companies are investing in single-cell protein production and metabolic engineering to create stabilizers with enhanced functionality compared to plant-derived alternatives. Regulatory support for biotechnology-derived ingredients, including the FDA's GRAS notification process, facilitates market entry for innovative microbial stabilizers. The challenge lies in scaling production to achieve cost competitiveness with established plant-based alternatives while maintaining quality consistency.

The Food Stabilizers Market Report is Segmented by Source (Plant, Microbial, Seaweed, Synthetic, and Animal), Application (Bakery and Confectionary, Dairy and Dairy-Alternatives, Meat and Poultry, Beverages, Sauces and Dressing, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe holds a 32.44% market share in 2024, supported by comprehensive regulatory frameworks and consumer demand for natural ingredients. The European Food Safety Authority's rigorous evaluation processes for food additives establish significant market entry barriers while ensuring stability for approved ingredients. EFSA's new guidance for novel food applications, starting February 2025, implements stricter requirements for microorganism-related foods and safety assessments. While this may extend approval timelines, it enhances consumer trust. The region's sustainability focus increases demand for biodegradable stabilizers and environmentally responsible packaging. European manufacturers are expanding seaweed cultivation and processing operations, with the seaweed hydrocolloids market growing at 5% annually due to health-conscious consumer preferences.

Asia-Pacific projects a 5.74% CAGR through 2030, driven by urbanization, middle-class expansion, and increased processed food consumption in developing economies. Japan's aging population creates demand for functional foods with longer shelf life, while India's food processing sector grows through government support and foreign investments.

North America shows consistent growth through clean-label trends and supportive regulations. The FDA's approval of 3 new natural color additives in 2025 demonstrates regulatory backing for clean-label innovation, while California's restrictions on synthetic additives prompt industry-wide product reformulation. South America and Middle East and Africa present growth potential, with Brazil's expanding food processing industry and the Middle East's increasing demand for halal-certified stabilizers driving regional development.

- Cargill, Incorporated

- Tate & Lyle Plc

- Archer Daniels Midland Company

- Ashland Co. Ltd.

- Kerry Group plc

- Palsgaard

- Nexira

- Gelita AG

- Ingredion Inc.

- BASF SE

- CP Kelco

- DuPont Nutrition & Biosciences

- DSM-Firmenich

- Givaudan SA

- Ajinomoto Co.

- Jungbunzlauer

- Taiyo Kagaku

- Fiberstar

- Corbion N.V.

- Roquette Freres

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for processed and convenince food globally

- 4.2.2 Consumer shift towards texture-enhanced clean label products

- 4.2.3 Stabilizers extend product shelf life in food applications

- 4.2.4 Emergence of stablizer-infused functional confectionary

- 4.2.5 Use of stablizers in meat analogs to mimic animal protein texture

- 4.2.6 Demand for gluten-free, texturally rich foods driving natural stalizer uptake

- 4.3 Market Restraints

- 4.3.1 Regulatory compliance requirements impact food additives market

- 4.3.2 Religious/ethical restrictions on animal-derived gelatin

- 4.3.3 Challenges in formulating with stabilizers in low-pH or high-salt products

- 4.3.4 Consumer demand for minimal ingredients list hindering stalizer usage

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source

- 5.1.1 Plant

- 5.1.2 Microbial

- 5.1.3 Seaweed

- 5.1.4 Synthetic

- 5.1.5 Animal

- 5.2 By Application

- 5.2.1 Bakery and Confectionary

- 5.2.2 Dairy and Dairy-alternatives

- 5.2.3 Meat and Poultry

- 5.2.4 Beverages

- 5.2.5 Sauces and Dressing

- 5.2.6 Jams and Jellies

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Spain

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Tate & Lyle Plc

- 6.4.3 Archer Daniels Midland Company

- 6.4.4 Ashland Co. Ltd.

- 6.4.5 Kerry Group plc

- 6.4.6 Palsgaard

- 6.4.7 Nexira

- 6.4.8 Gelita AG

- 6.4.9 Ingredion Inc.

- 6.4.10 BASF SE

- 6.4.11 CP Kelco

- 6.4.12 DuPont Nutrition & Biosciences

- 6.4.13 DSM-Firmenich

- 6.4.14 Givaudan SA

- 6.4.15 Ajinomoto Co.

- 6.4.16 Jungbunzlauer

- 6.4.17 Taiyo Kagaku

- 6.4.18 Fiberstar

- 6.4.19 Corbion N.V.

- 6.4.20 Roquette Freres

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK