PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844523

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844523

South America Cosmetics Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

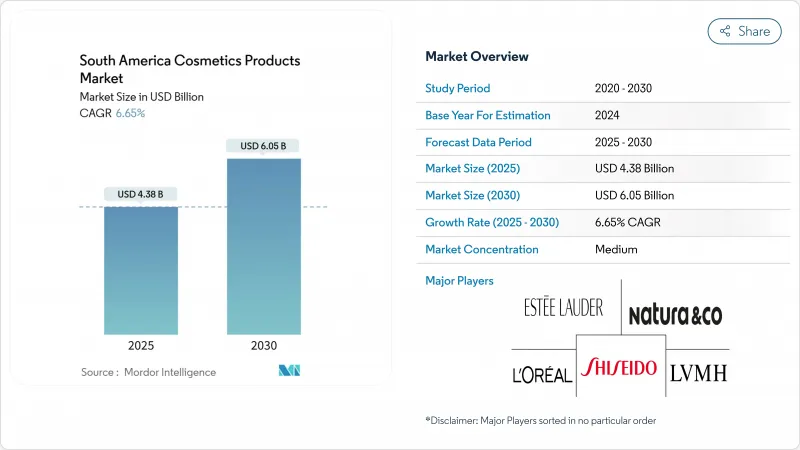

The South American cosmetics market size stands at USD 4.38 billion in 2025 and is projected to reach USD 6.05 billion by 2030, advancing at a 6.65% CAGR over the forecast window.

In South America, the cosmetics market is experiencing a significant uptrend, driven by the widespread adoption of digital commerce, a growing emphasis on sustainability, and the introduction of premium product offerings. Brazil serves as the regional cornerstone, while Argentina contributes to the momentum. Both countries are benefiting from rising disposable incomes, the expansion of formal retail networks, and the rapid adoption of mobile-first shopping experiences. On the supply side, local industry leaders such as Natura and Co. are strategically leveraging biodiversity sourcing to minimize import-related risks. Meanwhile, multinational corporations like L'Oreal are investing heavily in research and development, particularly in AI-driven skin diagnostic technologies, to strengthen their market presence. As the South American cosmetics market continues to enhance its omnichannel capabilities, the adoption of direct-to-consumer models and the implementation of micro-fulfillment pilots are optimizing inventory management, reducing working capital requirements, and accelerating product testing cycles.

South America Cosmetics Products Market Trends and Insights

Growing consumer focus on personalization and product experience

In South America, beauty personalization has evolved from shade matching to crafting entire rituals, blending products, digital services, and post-purchase interactions into an identity-affirming ecosystem. By analyzing detailed consumption patterns, brands streamline inventory, reducing SKU proliferation without sacrificing choice, thereby minimizing risk and freeing capital. Natura exemplifies this with its use of Amazonian botanicals, creating provenance narratives that resonate with regional pride and differentiate ingredient decks. Diagnostic tools, in-store or at-home, now craft tailored regimens, turning one-time shoppers into loyal subscribers. Brands target demographics like Gen Z and active-aging groups, enabling price variations without harming brand value. Consumers prioritize sensory elements texture, scent, packaging, alongside functionality, with premium textures, sustainable packaging, and appealing fragrances driving decisions. Inclusive products addressing diverse skin tones, hair types, and cultural preferences are in demand. Local and independent brands leverage this trend with hyper-targeted offerings celebrating Latin American heritage and diversity.

Influence of social media and digital beauty trends

Social platforms such as Instagram and TikTok have redefined the purchase funnel, shifting discovery and evaluation phases onto feeds that compress awareness and intent into a single scroll. Brazilian independent labels, for example, now routinely launch pilot runs below 10,000 units to test algorithmic traction before committing to full-scale manufacture. At the organisational level, digital intensity drives cross-functional hiring needs, content creators, data scientists, and supply chain analysts must coordinate under compressed timelines. The industry's pivot toward influencer-led commerce also forces a re-think of intellectual property risk, as misalignment with contracted creators can inflict brand damage at a scale that traditional advertising seldom reached. In 2024, social media accounted for 81% of internet activities in Brazil, according to CETIC (Centre of Excellence in Information and Communication Technologies). This significant engagement is driving the influence of digital beauty trends in the region .

Limited regulatory harmonization across countries

South American countries, including Brazil, Argentina, Colombia, and Chile, enforce distinct regulatory frameworks for cosmetics, covering areas such as ingredient approvals, labeling requirements, testing protocols, and registration processes. For example, Brazil's Health Regulatory Agency (ANVISA) is increasing documentation requirements under its 2024-2025 agenda by revising e-labeling standards and safety certification pathways, favoring companies with larger compliance teams. Similarly, Argentina's ANMAT Resolution 155/98 maintains stringent registration protocols. The lack of harmonized standards creates a strategic advantage for companies that integrate compliance as a core capability, enabling them to turn regulatory fragmentation into a competitive barrier against resource-limited entrants. As a result, leading manufacturers are centralizing regulatory expertise within shared-service hubs that support multiple Latin American markets. This approach enhances operational efficiency and unlocks scale benefits often overlooked in cost-of-goods analyses.

Other drivers and restraints analyzed in the detailed report include:

- Strong emphasis on branding and marketing activities

- Rising disposable incomes drive demand for premium cosmetics

- Dependence on imports for high-quality raw materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, lip and nail make-up products accounted for 46.61% of South America's cosmetics market, driven by their low unit prices and rapid replenishment cycles. Impulse purchases at drugstores and the emergence of hybrid polish formulas, which promise week-long wear without the need for UV lamps, bolster this segment. While eye cosmetics hold a smaller market share, they are projected to grow at a 6.95% CAGR through 2030. This growth is fueled by post-mask consumers gravitating towards expressive brows, lightweight mascaras, and transfer-proof liners. Furthermore, digital try-on features in eye sub-segments have led to a threefold increase in click-to-cart ratios on brand apps.

Further analysis of secondary market effects reveals that the rising sales of long-wear eye pigments are directly influencing the demand for complementary cleansing SKUs. Retailers are capitalizing on this trend by bundling waterproof makeup removers with mascara promotions, thereby enhancing cross-selling opportunities. Moreover, the growing emphasis on eye-area microbiome care is enabling brands to position themselves strategically within the premium skincare segment. This approach is effectively dissolving traditional category boundaries, fostering a more integrated and dynamic competitive landscape within the South American cosmetics market.

In 2024, mass products dominate the South American cosmetics market, accounting for a substantial 91.47% market share. This overwhelming dominance reflects the socioeconomic dynamics of the region and highlights the strategic prioritization of affordability by leading market players. In particular, Brazil exemplifies this trend, where prominent domestic companies such as Natura and Grupo Boticario have developed extensive and efficient distribution networks. These networks enable them to cater to consumers across diverse income groups, ensuring widespread accessibility to their products.

Meanwhile, the premium segment is emerging as a significant growth driver, with a projected CAGR of 7.32% through 2030. This robust growth trajectory indicates a notable shift in consumer preferences, fueled by increasing disposable incomes and a growing emphasis on beauty and personal care. The expansion of the premium segment is most evident in urban centers across Argentina, Chile, and Brazil. In these markets, international luxury brands are actively enhancing their presence by investing in both physical retail outlets and digital platforms. This strategic expansion aims to capture the attention and spending power of the region's rapidly growing affluent consumer base.

The South America Beauty Products Market Report is Segmented by Product Type (Facial Cosmetics, Eye-Cosmetics and More), Category (Mass, and Premium), Ingredient (Conventional/Synthetic, and Natural and Organic), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and More), and Geography (Brazil, Argentina, Chile, Peru, Colombia and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Natura and Co.,

- LVMH Moet Hennessy Louis Vuitton

- L'Oreal S.A.

- Prebel

- Estee Lauder Companies Inc.

- Procter and Gamble Co.

- Hypera Pharma

- Beiersdorf AG

- Shiseido Company Ltd.

- Kevenue Inc

- Puig S.L.

- Revlon Inc.

- Mary Kay Inc.

- Coty Inc.

- Surya Brasil

- Best Bronze

- Belcorp

- Yanbal International

- Hinode Group

- Oriflame Coemtics AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing consumer focus on personalization and product experience

- 4.2.2 Influence of social media and digital beauty trends

- 4.2.3 Strong emphasis on branding and marketing activities

- 4.2.4 Rising disposable incomes drive demand for premium cosmetics

- 4.2.5 Expansion of e-commerce platforms enhances product accessibility.

- 4.2.6 Growing awareness of sustainable and organic cosmetics fuels market growth.

- 4.3 Market Restraints

- 4.3.1 Limited regulatory harmonization across countries

- 4.3.2 Dependence on imports for high-quality raw materials

- 4.3.3 Limited access to advanced manufacturing technologies affects product innovation.

- 4.3.4 Economic instability in the region impacts consumer purchasing power.

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Facial Cosmetics

- 5.1.2 Eye Cosmetics

- 5.1.3 Lip and Nail Make-up Products

- 5.2 By Category

- 5.2.1 Premium Products

- 5.2.2 Mass Products

- 5.3 By Ingredient Type

- 5.3.1 Natural and Organic

- 5.3.2 Conventional/Synthetic

- 5.4 By Distribution Channel

- 5.4.1 Specialty Stores

- 5.4.2 Supermarkets/Hypermarkets

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Natura and Co.,

- 6.4.2 LVMH Moet Hennessy Louis Vuitton

- 6.4.3 L'Oreal S.A.

- 6.4.4 Prebel

- 6.4.5 Estee Lauder Companies Inc.

- 6.4.6 Procter and Gamble Co.

- 6.4.7 Hypera Pharma

- 6.4.8 Beiersdorf AG

- 6.4.9 Shiseido Company Ltd.

- 6.4.10 Kevenue Inc

- 6.4.11 Puig S.L.

- 6.4.12 Revlon Inc.

- 6.4.13 Mary Kay Inc.

- 6.4.14 Coty Inc.

- 6.4.15 Surya Brasil

- 6.4.16 Best Bronze

- 6.4.17 Belcorp

- 6.4.18 Yanbal International

- 6.4.19 Hinode Group

- 6.4.20 Oriflame Coemtics AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK