PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844527

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844527

Decorative Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

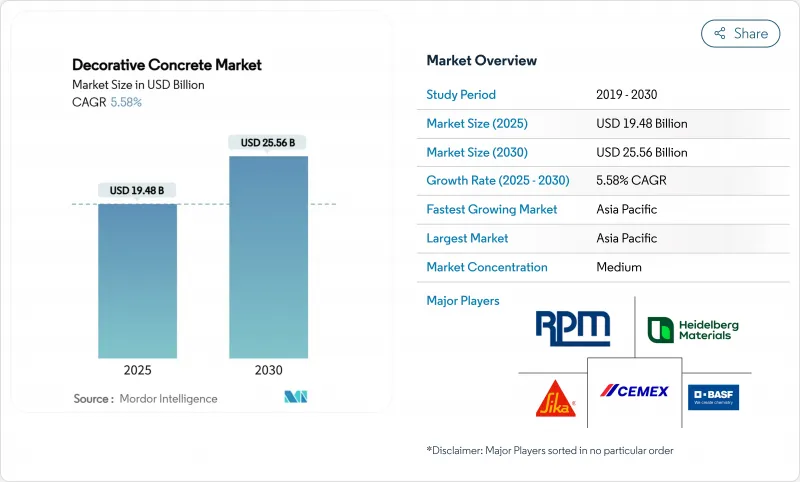

The Decorative Concrete Market size is estimated at USD 19.48 billion in 2025, and is expected to reach USD 25.56 billion by 2030, at a CAGR of 5.58% during the forecast period (2025-2030).

This sustained expansion reflects a decisive shift in global construction priorities toward materials that marry long-term durability with design versatility, especially as residential remodeling budgets remain elevated and commercial facilities continue to modernize. Heightened post-pandemic home-improvement outlays, an aging housing stock with a median age of 41 years, and growing preference for low-maintenance surfaces are reinforcing demand. In parallel, commercial refurbishments are adopting polished and stamped concrete to meet foot-traffic durability targets, while net-zero building mandates push producers toward bio-based admixtures and low-VOC mixes. Tariffs on imported cement, coupled with volatile pigment supply, amplify cost pressures but also open opportunities for vertically integrated suppliers and innovators in carbon-reduced formulations.

Global Decorative Concrete Market Trends and Insights

Rising Residential Remodeling and Refurbishment Spend Post-Pandemic

Elevated remodeling budgets have shifted toward fewer but higher-value projects, strengthening demand for surface upgrades that combine aesthetics with long service life. Average homeowner spend increased 12% in 2023 despite a brief dip in overall project volume, signaling a willingness to pay for premium finishes that raise property value and support aging-in-place needs. Decorative concrete aligns well because its 20-30-year life span outperforms many alternative pavements, limiting future repair cycles. An aging housing stock motivates extensive outdoor and basement renovations where stamped slabs and polished floors deliver quick visual impact. Mortgage rates trending toward 5.5% by mid-2025 should further unlock renovation funding, amplifying demand throughout the forecast window.

Preference for Stamped Concrete in New-Build Outdoor Living Spaces

Advances in stamping mats and integral coloring have dispelled dated perceptions of stamped surfaces and now enable convincingly natural textures that last beyond two decades when properly sealed. Unit installation costs retain a favorable spread versus quarried stone, enabling contractors to target broader demographic segments. Cool-tone pigments and geometric templates resonate with modern landscaping trends while permeable variants address storm-water mandates in dense urban projects. Integrated LED channels and metallic highlights differentiate premium installations, particularly around pool decks where cooler surface temperatures and slip resistance improve safety.

High Upfront Cost of Specialty Pigments, Molds and Sealers

Decorative concrete commands USD 200-300 per cubic yard against USD 100-150 for standard mixes, a gap driven by expensive iron-oxide pigments, silicone molds, and multi-layer sealing systems. Contractors pass these costs to homeowners and small developers, curbing uptake in price-sensitive regions. Labor premiums also arise because stamped or polished finishes require slower placement rates and specialized finishing skills. Smaller contractors hesitate to purchase proprietary stamp libraries or diamond-polishing equipment, limiting service availability in secondary cities and slowing rural penetration.

Other drivers and restraints analyzed in the detailed report include:

- Net-Zero and Green-Building Certification Pushing Colored/Low-VOC Mixes

- Growth of Decorative Concrete Overlays in Fast-Track Renovation Projects

- Volatility in Cement and Pigment Supply Chains Inflating Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stamped concrete retained a 40.21% decorative concrete market share in 2024, underpinned by its adaptability across driveways, patios, and commercial plazas. Enhanced tool libraries offer slate, timber, and even integrated logo impressions, enabling contractors to court hospitality and branded retail chains. Polished concrete, while holding a smaller base, is forecast to grow at a 6.19% CAGR to 2030 as facility managers appreciate seamless floors that resist forklift abrasion and ease cleaning protocols. Decorative concrete market size benefits from overlays that extend surface life without structural demolition, and from emerging self-healing capsules that release lime to seal microcracks and prolong service intervals. Overall, diversified type options help suppliers meet both budget and performance briefs, reinforcing the decorative concrete market's resilience.

Continued R&D targets color-fast dyes and rapid-cure sealers that shorten turnover cycles. Colored mixes leverage finer pigment dispersions to avoid streaking, whereas translucent dye systems permit artistic gradients favored in boutique venues. Fiber-reinforced designs alleviate shrinkage cracking, while UV-resistant topcoats guard against fade in open-air entertainment spaces. Collectively, these advances widen use cases and deepen penetration into high-visibility architectural elements, bolstering long-term decorative concrete market growth.

The Decorative Concrete Market Report is Segmented by Type (Stamped Concrete, Polished Concrete, Concrete Overlay, Stained Concrete, Colored Concrete, Concrete Dye, Other Types), Application (Footpath and Driveway, Patio, and More), End-User Industry (Residential, Non-Residential), and Geography (Asia-Pacific, North America, Europe, and More ). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.83% of 2024 revenue and posts a leading 6.53% CAGR to 2030, reinforcing its dual role as market leader and primary growth driver. China alone consumed 6.6 gigatons of cement between 2011-2013, dwarfing 20th-century U.S. usage, and still accounts for more than half of global output. Massive housing-relocation schemes and megaprojects such as Indonesia's USD 5 billion industrial park underscore structural demand, while permeable decorative slabs respond to stringent storm-water ordinances in rapidly urbanizing cities. Local producers are scaling low-clinker binders to align with national decarbonization pledges, broadening the product mix and tempering import dependence.

North America faces pronounced cost volatility after 2025 import tariffs but retains growth potential supported by mortgage-rate easing and continued public-sector outlays. An aging housing stock boosts residential resurfacing, while the Bipartisan Infrastructure Law extends opportunities in public plazas and transit hubs. Supply-chain headwinds encourage integrated suppliers to expand captive quarry and terminal capacity, securing raw materials and stabilizing decorative concrete market pricing.

Europe's stringent carbon directives recalibrate specifications toward low-embodied materials, catalyzing uptake of bio-based admixtures and recycled aggregates. Producers investing in waste-heat recovery kilns and bio-char co-firing earn procurement preference under EU Taxonomy rules, reinforcing regional competitive advantages. Meanwhile, Middle East, Africa, and South America register steady gains anchored by urban population growth, though currency volatility and limited installer capacity temper immediate upside potential. Across all regions the decorative concrete market demonstrates capacity to align with local policy imperatives and construction-sector cycles, sustaining a broad demand base.

- 3M

- BASF

- Boral

- CEMEX S.A.B. de C.V.

- Dex-O-Tex

- Elite Crete Systems

- Heidelberg Materials

- Holcim

- Palermo Concrete Inc

- Parchem Construction Supplies

- PPG Industries Inc

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Subana Technologies Pvt. Ltd.

- Tarmac

- The Euclid Chemical Company

- The Sherwin-Williams Company

- UltraTech Cement Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising residential remodeling and refurbishment spend post-pandemic

- 4.2.2 Preference for stamped concrete in new-build outdoor living spaces

- 4.2.3 Net-zero and green-building certification pushing colored/low-VOC mixes

- 4.2.4 Growth of decorative concrete overlays in fast-track renovation projects

- 4.2.5 Adoption of bio-based admixtures to cut embodied-carbon footprint

- 4.3 Market Restraints

- 4.3.1 High upfront cost of specialty pigments, molds and sealers

- 4.3.2 Volatility in cement and pigment supply chains inflating prices

- 4.3.3 Shortage of certified decorative concrete installers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Stamped Concrete

- 5.1.2 Polished Concrete

- 5.1.3 Concrete Overlay

- 5.1.4 Stained Concrete

- 5.1.5 Colored Concrete

- 5.1.6 Concrete Dye

- 5.1.7 Other Types

- 5.2 By Application

- 5.2.1 Footpath and Driveway

- 5.2.2 Patio

- 5.2.3 Pool Deck

- 5.2.4 Floor

- 5.2.5 Wall

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 BASF

- 6.4.3 Boral

- 6.4.4 CEMEX S.A.B. de C.V.

- 6.4.5 Dex-O-Tex

- 6.4.6 Elite Crete Systems

- 6.4.7 Heidelberg Materials

- 6.4.8 Holcim

- 6.4.9 Palermo Concrete Inc

- 6.4.10 Parchem Construction Supplies

- 6.4.11 PPG Industries Inc

- 6.4.12 RPM International Inc.

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 Subana Technologies Pvt. Ltd.

- 6.4.16 Tarmac

- 6.4.17 The Euclid Chemical Company

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 UltraTech Cement Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment