PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844530

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844530

Colorectal Cancer Diagnostics And Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

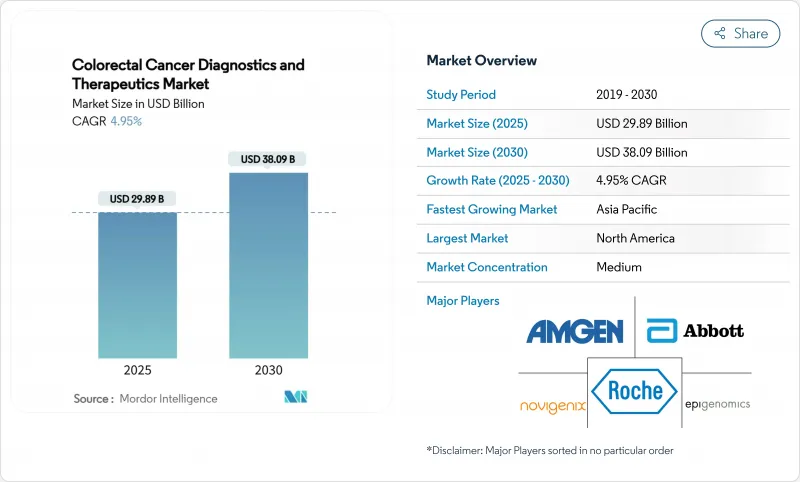

The colorectal cancer diagnostics and therapeutics market is valued at USD 29.89 billion in 2025 and is forecast to reach USD 38.09 billion by 2030, advancing at a 4.95% CAGR.

The current expansion is paced by precision medicine, AI-enabled screening, and the steady roll-out of immunotherapy options that raise survival outcomes while sustaining premium pricing. Non-invasive tests-stool DNA, blood-based assays, and AI-assisted colonoscopy-bring previously unscreened populations into clinical pathways, while dual-checkpoint blockade reshapes first-line therapy for biomarker-defined patients. Reimbursement alignment in the United States and policy convergence in Europe accelerate uptake, and Asia Pacific leapfrogs legacy bottlenecks through government-funded technology programs. Cost pressures and capacity constraints persist, yet the colorectal cancer diagnostics and therapeutics market continues to monetize innovation faster than screening volumes plateau in mature economies.

Global Colorectal Cancer Diagnostics And Therapeutics Market Trends and Insights

Rising Incidence of Colorectal Cancer

Early-onset incidence climbed from 5.43 to 6.13 per 100,000 between 1990 and 2021, and modeling signals continued acceleration through 2030. High-income settings see lifestyle convergence that elevates risk at younger ages, while Asia Pacific records incidence rates of 7.51 per 100,000 for males and 6.22 for females. Longer survivorship boosts lifetime screening and follow-up demand, anchoring sustained revenue visibility in the colorectal cancer diagnostics and therapeutics market.

Rapid Adoption of Next-Generation Stool-DNA and Blood-Based Screening Tests

FDA approvals for Shield (83.1% sensitivity), Cologuard Plus (93.9%), and ColoSense (94.4%) in 2024 expanded the non-invasive testing toolkit. These modalities address the 40% of eligible adults who have historically skipped colonoscopy, potentially adding 15-20 million U.S. lives to the annual screening pool. Investor confidence solidified with Geneoscopy's USD 105 million Series C round in January 2025.

High Drug Cost and Treatment-Related Toxicities

Targeted therapy regimens average USD 150,000-200,000 per year, a burden that curtails uptake where out-of-pocket spending exceeds 60% of total healthcare costs. Combination immunotherapy requires intensive safety monitoring as grade 3/4 adverse events can reach 81%, stretching oncology budgets and care infrastructure in the colorectal cancer diagnostics and therapeutics industry.

Other drivers and restraints analyzed in the detailed report include:

- Technological Leaps in Targeted Therapies and Immunotherapy Pipelines

- Expansion of Guideline-Based Screening to 45-Year-Olds in Key Markets

- Sub-Optimal Screening Adherence in Low-Resource Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics generated strong tailwinds, posting a 13.6% CAGR that outpaced screening activity. Opdivo + Yervoy secured first-line status for MSI-H/dMMR disease and reset revenue expectations at premium price points. KRAS, EGFR, and HER2 targets widen addressable pools, boosting the colorectal cancer diagnostics and therapeutics market size for personalized regimens. Diagnostics retained 27.9% of colorectal cancer diagnostics and therapeutics market share in 2024, underwritten by multitarget stool DNA, blood biomarkers, and AI colonoscopy that make screening more convenient. Medtronic's GI Genius raised adenoma detection by 14.4% and secured a three-year VA contract for nearly 100 additional units. Shield and ColoSense advanced blood and RNA-based testing, yet payers still calibrate coverage for their higher per-test costs.

Diagnostics monetization pivots from volume to diversification. Exact Sciences rolled out Cologuard Plus with 93.9% sensitivity, reducing false positives and reinforcing its leadership. Blood-based assays grow fast among younger cohorts who prefer needle sticks to invasive scopes, an alignment that improves adherence. Molecular residual-disease tests extend value across the treatment continuum by flagging minimal disease after surgery, further enlarging colorectal cancer diagnostics and therapeutics market size opportunities through follow-up testing.

The Colorectal Cancer Diagnostics and Therapeutics Market is Segmented by Modality (Diagnostic Techniques {Stool-Based Tests, Blood-Based Biomarker Tests, Endoscopy-Based Imaging, Radiology & Molecular Endoscopy, and More} and Therapeutics {Chemotherapy, Targeted Therapy, Immunotherapy, and More}, and Geography (North America, Europe, Asia Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's leadership is anchored in reimbursement breadth and innovation velocity. Medicare coverage for CT colonography in 2025 removes a procedural cost hurdle, complementing blood and stool tests already reimbursed under preventive codes. Sixty percent of colorectal cancer drug trials run in U.S. and Canadian centers, accelerating FDA clearances that ripple worldwide. VA deployment of 100 GI Genius units underscores institutional migration to AI diagnostics. Regulatory pathways such as Breakthrough Device and Priority Review condense timelines, yet rising scrutiny on therapy cost inflates time-to-profit hurdles for recent launches.

Asia Pacific outruns all regions at 7.70% CAGR. Government programs extend screening to rural China and subsidize AI colonoscopy in Japan, helping technology leapfrog traditional bottlenecks. Incidence rates of 7.51 per 100,000 for males and 6.22 for females press policymakers to act. Manufacturing clusters reduce equipment costs while medical tourism funnels regional patients to technology hubs in Thailand and India, amplifying demand inside the colorectal cancer diagnostics and therapeutics market.

Europe's trajectory is stable, fueled by well-established national programs. Utilization still varies: 75% in Denmark yet under 10% in lower-income members. EMA centralized approvals elongate pipeline timelines compared with the FDA; however, once clearance is granted, reimbursement coverage through universal systems leads to rapid penetration. Middle East & Africa promise future upside, especially in GCC states where oil revenues finance cancer centers equipped with AI imaging and immunotherapies.

- Abbott Laboratories

- Amgen

- Roche

- Exact Sciences Corp.

- Quest Diagnostics

- Labcorp Holdings Inc.

- Siemens Healthineers

- Guardant Health

- Medtronic plc (GI Genius)

- Merck

- Bristol-Myers Squibb

- Sanofi

- Bayer

- Pfizer

- Johnson & Johnson

- BGI Genomics Co. Ltd.

- Epigenomics

- VolitionRx Ltd.

- Clinical Genomics Technologies

- EDP Biotech Corp.

- Novigenix

- Taiho Pharmaceutical Co.

- Regeneron Pharmaceuticals

- Eli Lilly and Company

- Onyx/Biotechne (example mCRC assets)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence and Prevalence Of Colorectal Cancer

- 4.2.2 Rapid Adoption Of Next-Generation Stool-DNA And Blood-Based Screening Tests

- 4.2.3 Technological Leaps In Targeted Therapies & Immunotherapy Pipelines

- 4.2.4 Expansion Of Guideline-Based Screening To 45-Year-Olds In Key Markets

- 4.2.5 Molecular Residual-Disease (MRD) Tests Reshaping Adjuvant-Therapy Decisions

- 4.2.6 Value-Based Reimbursement That Rewards Early Detection

- 4.3 Market Restraints

- 4.3.1 High Drug Cost & Treatment-Related Toxicities

- 4.3.2 Sub-Optimal Screening Adherence In Low-Resource Settings

- 4.3.3 Limited Immunotherapy Efficacy In MSS Tumors Causing High Trial Attrition

- 4.3.4 Data-Integration & Privacy Hurdles For AI-Driven Diagnostics Platforms

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Modality

- 5.1.1 Diagnostics Techniques

- 5.1.1.1 Stool-Based Tests

- 5.1.1.1.1 Fecal Immunochemical Test (FIT)

- 5.1.1.1.2 guaiac-FOBT

- 5.1.1.1.3 Multi-target Stool-DNA (mt-sDNA)

- 5.1.1.2 Blood-Based Biomarker Tests

- 5.1.1.2.1 ctDNA assays

- 5.1.1.2.2 Epigenetic methylation panels

- 5.1.1.3 Endoscopy-Based Imaging

- 5.1.1.3.1 Colonoscopy

- 5.1.1.3.2 AI-assisted Colonoscopy

- 5.1.1.3.3 Flexible Sigmoidoscopy

- 5.1.1.4 Radiology & Molecular Endoscopy

- 5.1.1.5 Histopathology / Digital Pathology

- 5.1.2 Therapeutics

- 5.1.2.1 Chemotherapy

- 5.1.2.1.1 Fluoropyrimidines (5-FU, Capecitabine)

- 5.1.2.1.2 Oxaliplatin-based regimens (FOLFOX)

- 5.1.2.1.3 Irinotecan-based regimens (FOLFIRI)

- 5.1.2.2 Targeted Therapy

- 5.1.2.2.1 Anti-EGFR (Cetuximab, Panitumumab)

- 5.1.2.2.2 Anti-VEGF (Bevacizumab, Aflibercept)

- 5.1.2.2.3 BRAF / HER2 / KRAS G12C inhibitors

- 5.1.2.3 Immunotherapy

- 5.1.2.3.1 PD-1 / PD-L1 inhibitors

- 5.1.2.3.2 CTLA-4 combos

- 5.1.2.3.3 CAR-T / Oncolytic Viruses

- 5.1.2.4 Other Therapeutics (Radioembolization, Vaccines)

- 5.1.1 Diagnostics Techniques

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia Pacific

- 5.2.4 Middle East & Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East & Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Overview, Market-Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Amgen Inc.

- 6.3.3 F. Hoffmann-La Roche AG

- 6.3.4 Exact Sciences Corp.

- 6.3.5 Quest Diagnostics Inc.

- 6.3.6 Labcorp Holdings Inc.

- 6.3.7 Siemens Healthineers AG

- 6.3.8 Guardant Health Inc.

- 6.3.9 Medtronic plc (GI Genius)

- 6.3.10 Merck & Co., Inc.

- 6.3.11 Bristol Myers Squibb Co.

- 6.3.12 Sanofi SA

- 6.3.13 Bayer AG

- 6.3.14 Pfizer Inc.

- 6.3.15 Johnson & Johnson (Janssen)

- 6.3.16 BGI Genomics Co. Ltd.

- 6.3.17 Epigenomics AG

- 6.3.18 VolitionRx Ltd.

- 6.3.19 Clinical Genomics Technologies

- 6.3.20 EDP Biotech Corp.

- 6.3.21 Novigenix SA

- 6.3.22 Taiho Pharmaceutical Co.

- 6.3.23 Regeneron Pharmaceuticals Inc.

- 6.3.24 Eli Lilly & Co.

- 6.3.25 Onyx/Biotechne (example mCRC assets)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment