PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844561

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844561

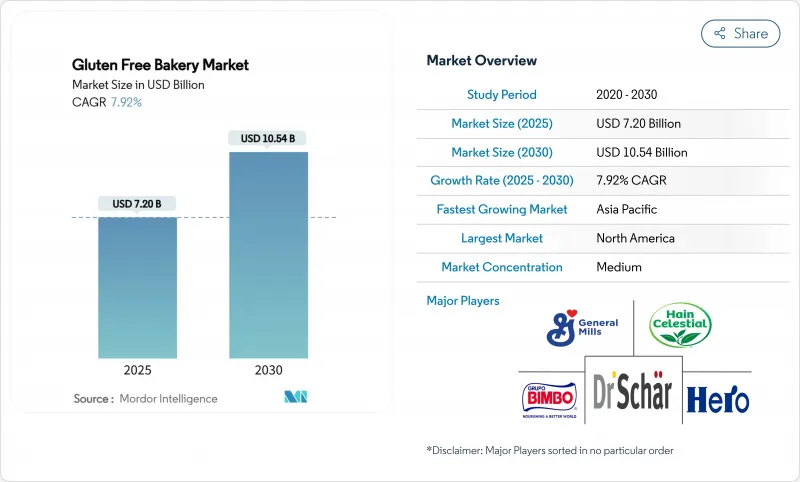

Gluten Free Bakery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The gluten-free bakery products market size is estimated to be USD 7.20 billion in 2025 and is projected to reach USD 10.54 billion by 2030, expanding at a 7.92% CAGR.

The market expansion is attributed to the increasing prevalence of celiac disease, which affects approximately 1% of the global population, and consumers who adopt gluten-free diets as a health-conscious decision, according to the National Institutes of Health. Besides, regulatory clarity also supports demand; the US FDA requires any product labeled "gluten-free" to contain less than 20 ppm gluten, giving shoppers confidence in safety and label accuracy. On the supply side, large bakeries continue to scale dedicated production lines, while smaller brands exploit online channels and direct-to-consumer (D2C) subscriptions to reach niche audiences. Persistent price premiums, cross-contamination risks, and climate-related grain shortages remain the key friction points, yet they have not slowed new-product velocity or capital investment.

Global Gluten Free Bakery Market Trends and Insights

Rising Prevalence of Celiac Disease and Gluten Sensitivity

The increasing prevalence of celiac disease, with 1 in 70 Australians affected according to the Australian Broadcasting Corporation's 2024 data and 1% prevalence in the US as reported by the Agency for Healthcare Research and Quality, generates market demand for gluten-free food options . The gluten-free bakery segment addresses the requirements of both medically diagnosed gluten-intolerant consumers and health-focused customers who select gluten-free products. Enhanced diagnostic capabilities and ongoing research into enzyme therapies and immune modulation are projected to increase consumer awareness of gluten sensitivity, strengthening the demand for gluten-free alternatives. Manufacturers are implementing product development strategies using alternative flours such as almond, rice, and quinoa to produce gluten-free baked goods that maintain quality standards comparable to conventional products. Companies implementing certified gluten-free labeling, supply chain transparency, and product quality optimization are positioned to capitalize on this expanding market. The gluten-free bakery segment, comprising artisan breads, muffins, and pastries, offers market opportunities for both large-scale manufacturers and specialized bakeries.

Clean-Label "Free-From" Positioning by Premium Bakery Brands

The gluten-free market has evolved from serving medical needs to becoming a lifestyle choice through premium positioning and clean-label messaging. This shift allows manufacturers to increase profit margins and reach broader consumer segments. In 2024, Ardent Mills expanded its portfolio by introducing Ancient Grains Plus Baking Flour Blend and Egg Replace products across its network of over 40 gluten-free facilities, focusing on plant-based and sustainable solutions. Companies like Renewal Mill are addressing both ingredient transparency and environmental concerns by developing upcycled heirloom corn flour with gluten content below 5 ppm. However, manufacturers face the challenge of maintaining product functionality while meeting clean-label demands, as traditional gluten-free formulations depend on hydrocolloids and emulsifiers to achieve desired texture and shelf life.

Premium Price Versus Conventional Bakery Items

The elevated pricing of gluten-free bakery products results from the high cost of ingredient alternatives to wheat flour, including rice, tapioca, sorghum, and almond flour. These alternative ingredients do not provide the binding and elastic properties of gluten, requiring manufacturers to implement more complex formulations for baked goods. Operational costs increase due to the necessity for dedicated gluten-free manufacturing facilities or separate production lines to prevent cross-contamination, combined with reduced production volumes. The manufacturing process requires increased labor allocation and rigorous quality control protocols due to the technical challenges of gluten-free doughs, which demonstrate reduced stability and increased adhesion compared to conventional doughs. In North American and European markets, the current competitive landscape enables manufacturers to maintain premium pricing while implementing product certifications and safety protocols. This pricing structure may shift as production capacity increases, manufacturing processes automate, and market entrants introduce cost-effective alternatives. In emerging markets, the premium pricing of gluten-free bakery products continues to impede market penetration, despite increasing consumer awareness of gluten sensitivities and health considerations among populations with constrained purchasing power.

Other drivers and restraints analyzed in the detailed report include:

- Labeling Laws and Certifications Builds Consumer Trust

- Direct-to-Consumer Subscription Models Boosting Niche Brand Reach

- Cross-Contamination Risks in Shared Facilities of Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bread maintains a commanding 36.38% market share in 2024, reflecting its status as a dietary staple that consumers prioritize when transitioning to gluten-free diets. However, the cakes, muffins, and brownies segment accelerates at 12.02% CAGR through 2030, indicating evolving consumer expectations beyond basic nutrition toward indulgent experiences. Lancaster Colony launched its first gluten-free frozen bread line under the New York Bakery brand in September 2024, featuring patent-pending formulation technology that enhances texture and flavor while maintaining certification standards. Cookies and biscuits occupy the middle ground, benefiting from portion control appeal and longer shelf life advantages that facilitate distribution and inventory management.

In January 2024, Nothing Bundt Cakes introduced new gluten-free products, aligning with the market trend of mainstream bakery chains expanding their gluten-free portfolios to address increasing consumer demand. This expansion demonstrates the segment's commercial potential beyond niche markets. The bakery products segment has diversified through the incorporation of protein-enriched and functional ingredients, meeting consumer requirements for baked goods with enhanced nutritional benefits beyond gluten-free attributes.

The Gluten Free Bakery Products Market Report is Segmented by Product Type (Bread, Cookies and Biscuits, Cakes and Muffins, and Other Gluten-Free Bakery Products), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialist Stores, Online Retail, and Other Channels), Flour Type (Corn Flour, Rice Flour, and Other Flour Types), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds 33.96% market share in 2024, supported by high consumer awareness, well-established regulatory frameworks, and premium positioning strategies that drive per capita revenue. The region's market leadership stems from sophisticated distribution networks, strong retail partnerships, and continuous product innovation. Consumer preferences in North America increasingly favor premium gluten-free options, particularly in snacks and bakery segments. The market demonstrates sustained growth potential through expanding product categories and enhanced nutritional profiles.

Asia-Pacific demonstrates the highest growth rate at 12.19% CAGR through 2030, fueled by increasing disposable incomes, urbanization trends, and growing health consciousness among middle-class consumers. The IFIA/HFE 2024 exhibition in Japan highlighted gluten-free product innovations, including specialized madeleines, demonstrating manufacturers' growing focus on Asian markets. Regional market development is supported by improving retail infrastructure and digital commerce platforms. India's FSSAI extended foreign food manufacturing facility registration deadlines to September 2024, creating market entry opportunities for international brands, as reported by the United States Department of Agriculture.

Europe shows increasing demand for gluten-free products, particularly in the bakery segment, with strong growth in countries like Germany, France, and the United Kingdom. Market participants are developing new gluten-free options in response to rising health consciousness and awareness among consumers, focusing on taste improvement and texture enhancement. For instance, IfD Allensbach reported that 2.16 million consumers in Germany purchased gluten-free products within 14 days in 2024 . Moreover, in June 2025, gluten-free food manufacturer Juvela introduced a new bakery brand, Oaf, offering bread and related products, exemplifying the market's innovation trajectory. The region's growth is further supported by stringent food labeling regulations, increased celiac disease diagnosis rates, and expanding retail distribution channels.

- Dr. Schar AG/SpA

- General Mills, Inc.

- Hain Celestial Group

- Grupo Bimbo SAB de CV

- Hero Group AG

- Flowers Foods Inc. (Canyon Bakehouse)

- Warburtons Ltd.

- Amy's Kitchen Inc.

- Bob's Red Mill Natural Foods

- Dawn Food Products Inc

- The Kellog Company

- Mission Foods

- Genius Foods Ltd.

- BFree Foods

- Kinnikinnick Foods Inc.

- Toufayan Bakeries

- Nairn's Oatcakes Ltd.

- WOW Baking Company,

- The Smart Baking Company

- Ener-G Foods

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Celiac Disease and Gluten Sensitivity

- 4.2.2 Clean-Label "Free-From" Positioning by Premium Bakery Brands

- 4.2.3 Labeling Laws and Certifications Builds Consumer Trust

- 4.2.4 Direct-to-Consumer Subscription Models Boosting Niche Brand Reach

- 4.2.5 Increasing Innovation and Variety

- 4.2.6 Influence of Celebrity Endorsments

- 4.3 Market Restraints

- 4.3.1 Premium Price Versus Conventional Bakery Items

- 4.3.2 Cross-Contamination Risks in Shared Facilities of Emerging Markets

- 4.3.3 Shorter Shelf-Life of Clean-Label Gluten-Free Bread

- 4.3.4 Climatic Volatility Affecting Specialty Flour (Sorghum, Buckwheat) Supply

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bread

- 5.1.2 Cookies and Biscuits

- 5.1.3 Cakes, and Muffins (includes cupcakes)

- 5.1.4 Other Gluten-Free Bakery Products (brownies)

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets and Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Specialist Stores

- 5.2.4 Online Retail

- 5.2.5 Other Distribution Channels

- 5.3 By Flour type

- 5.3.1 Corn Flour

- 5.3.2 Rice Flour

- 5.3.3 Other Flour Types

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Dr. Schar AG/SpA

- 6.4.2 General Mills, Inc.

- 6.4.3 Hain Celestial Group

- 6.4.4 Grupo Bimbo SAB de CV

- 6.4.5 Hero Group AG

- 6.4.6 Flowers Foods Inc. (Canyon Bakehouse)

- 6.4.7 Warburtons Ltd.

- 6.4.8 Amy's Kitchen Inc.

- 6.4.9 Bob's Red Mill Natural Foods

- 6.4.10 Dawn Food Products Inc

- 6.4.11 The Kellog Company

- 6.4.12 Mission Foods

- 6.4.13 Genius Foods Ltd.

- 6.4.14 BFree Foods

- 6.4.15 Kinnikinnick Foods Inc.

- 6.4.16 Toufayan Bakeries

- 6.4.17 Nairn's Oatcakes Ltd.

- 6.4.18 WOW Baking Company,

- 6.4.19 The Smart Baking Company

- 6.4.20 Ener-G Foods

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK