PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844572

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844572

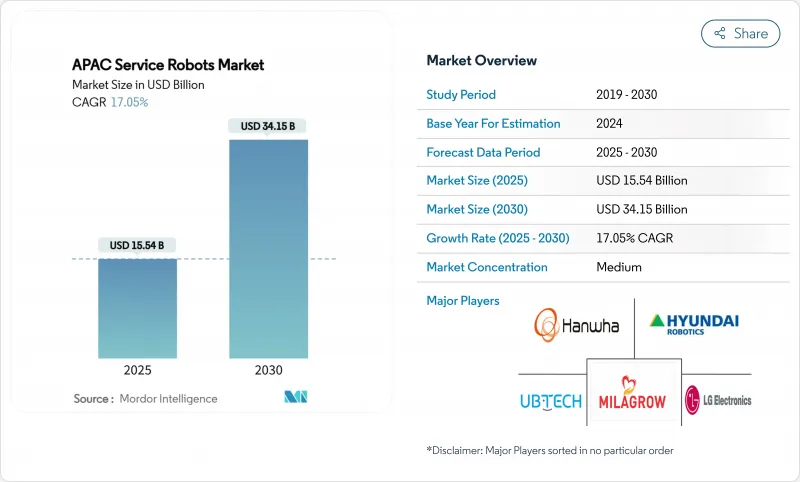

Asia-Pacific Service Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Asia Pacific Service Robotics Market was worth USD 15.54 billion in 2025 and is forecast to expand to USD 34.15 billion by 2030, posting a 17.05% CAGR during 2025-2030.

A surge in automation programs across China, Japan and South Korea is redefining workforce strategies, while e-commerce, healthcare modernization and government-backed digital agendas accelerate adoption. Logistics automation is no longer an efficiency play-it has become an operational necessity as tight labor markets and last-mile delivery pressures intensify. Healthcare providers now treat robots as core clinical assets that improve patient outcomes and relieve staff shortages. Convergence of 5G and on-board AI is enabling real-time remote control and data analytics, broadening deployment options into public services and critical infrastructure inspection. Although high integration costs and fragmented safety standards still temper uptake among SMEs, Robotics-as-a-Service models are starting to close the affordability gap.

Asia-Pacific Service Robots Market Trends and Insights

E-commerce boom driving logistics AMRs

Rising online retail volumes across Asia have pushed warehouse operators toward autonomous mobile robots (AMRs) that shrink fulfillment times and mitigate labor shortages. Chinese vendor Syrius Robotics plans to ship 3,000 AMRs annually to Japanese sites-10 times its current run-rate-as local overtime caps restrict driver availability. Localized manufacturing by Libiao Robotics further illustrates how near-shore production sidesteps supply-chain friction and import duties. Payback periods now average under 2.5 years, making AMRs a viable option for mid-sized distributors. Regulatory changes therefore act as a demand catalyst, turning AMRs into essential infrastructure within the APAC Service Robots Market.

Aging-population healthcare demand

Japan's share of citizens aged 65+ reached 27.3% in 2025, prompting hospitals and care homes to deploy robots for patient lifting, diaper changing and medication logistics. The AIREC caregiving robot from Waseda University showcases advanced physical assistance that surpasses basic monitoring. Robot integration has cut staff turnover and freed personnel for empathy-intensive tasks, while automated meal transport yields EUR 9,596 (USD 10,356) in annual savings per clinic. China's new international standard for elderly-care robots positions domestic suppliers for leadership in global applications, accelerating the Asia Pacific Service Robotics Market toward healthcare value creation.

High installation and integration cost

Although hardware prices keep falling-the average humanoid is projected to reach USD 20,000-30,000 in 2025-total integration outlays often run two to three times the purchase cost due to site retrofits and staff training. For many SMEs, capital constraints delay adoption in the APAC Service Robots industry. RaaS vendors now offer subscription models covering maintenance and updates, helping customers bypass large upfront expense.

Other drivers and restraints analyzed in the detailed report include:

- Government incentives and Made-in-APAC programs

- 5G/AI convergence enabling remote autonomy

- Fragmented safety/certification regimes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Professional robots generated the bulk of 2024 revenues, holding 69% of APAC Service Robots market share. Their leadership rests on tangible ROI: AMR fleets cut picking time by 50% while powered exoskeletons reduce workplace injuries. Logistics systems remain the highest-revenue subsegment, propelled by omnichannel retail and same-day delivery obligations. Medical robots command premium prices for surgical precision and hospital logistics, whereas exoskeletons address lifting and fatigue issues on assembly lines. Public-relation robots offer concierge services in hospitality but adoption is moderated by cultural acceptance and language nuance.

Personal robots are scaling quickly, posting a 22.46% CAGR forecast through 2030. Domestic cleaning units lead shipments, illustrated by Ecovacs hitting RMB 16.54 billion (USD 2.3 billion) in 2024 revenue despite margin pressure. Elderly-care companions and wearable assistance devices promise the next leg of growth as aging societies drive demand. Entertainment models-pet-inspired bots and STEM education kits-round out the segment, enhancing long-tail sales across the APAC Service Robots Market.

Hardware captured 64% of 2024 revenue. Actuators remain the costliest element as torque density advances, and sensor fusion raises ASPs for LiDAR and depth cameras. Johnson Electric reported double-digit Asian growth in motion systems linked to robotics demand.

Software is cementing its role as the value engine, set to post 24.21% CAGR to 2030. Cloud-connected orchestration, perception algorithms and fleet-management dashboards convert raw hardware into adaptable solutions. OMRON intends to surpass JPY 100 billion (USD 682 million) in data-solution sales by 2027, symbolizing the transition from product vendor to platform orchestrator. Services-maintenance, analytics, training-unlock recurring revenue in the APAC Service Robots industry.

The Asia-Pacific Service Robots Market Report is Segmented by Type (Professional Robots, Personal Robots), Application (Military and Defense, Agriculture, Construction and Mining, and More), Component (Hardware, Software, and Services), Operating Environment (Ground, Aerial, and Marine), Mobility (Mobile Robots, and Stationary Robots), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- UBTECH Robotics Inc.

- Ecovacs Robotics Co. Ltd.

- SIASUN Robot and Automation Co. Ltd.

- LG Electronics Inc.

- SoftBank Robotics Corp.

- Omron Corp.

- Hyundai Robotics Co. Ltd.

- Panasonic Holdings - Robotics BU

- DJI Innovations

- Geek+ Robotics Co. Ltd.

- Milagrow HumanTech

- Reeman Intelligent Tech

- Rainbow Robotics Co. Ltd.

- Roborock Technology Co. Ltd.

- UB-Tech (Shanghai) Intelligent

- Yamaha Motor - Robotics BU

- Doosan Robotics Inc.

- Hanwha Robotics

- Keenon Robotics

- TMi Robotics (TMiRob)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom driving logistics AMRs

- 4.2.2 Aging-population healthcare demand

- 4.2.3 Government incentives and Made-in-APAC programs

- 4.2.4 5G/AI convergence enabling remote autonomy

- 4.2.5 Humanoid robots for EV-battery lines (under-the-radar)

- 4.2.6 Infrastructure-inspection robots for aging assets (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 High installation and integration cost

- 4.3.2 Fragmented safety / certification regimes

- 4.3.3 Data-privacy and cyber-security concerns

- 4.3.4 Import dependence on precision actuators and sensors (under-the-radar)

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Robots Type

- 5.1.1 Professional Robots

- 5.1.1.1 Logistic Systems

- 5.1.1.2 Medical Robots

- 5.1.1.3 Powered Human Exoskeletons

- 5.1.1.4 Public-Relation Robots

- 5.1.2 Personal Robots

- 5.1.2.1 Domestic

- 5.1.2.2 Entertainment

- 5.1.2.3 Elderly and Handicap Assistance

- 5.1.1 Professional Robots

- 5.2 By Application

- 5.2.1 Military and Defense

- 5.2.2 Agriculture, Construction and Mining

- 5.2.3 Transportation and Logistics

- 5.2.4 Healthcare

- 5.2.5 Government

- 5.2.6 Other Applications

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.1.1 Actuators

- 5.3.1.2 Sensors

- 5.3.1.3 Controllers

- 5.3.2 Software

- 5.3.3 Services

- 5.3.1 Hardware

- 5.4 By Operating Environment

- 5.4.1 Ground

- 5.4.2 Aerial

- 5.4.3 Marine

- 5.5 By Mobility

- 5.5.1 Mobile Robots

- 5.5.2 Stationary Robots

- 5.6 By Country

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 UBTECH Robotics Inc.

- 6.4.2 Ecovacs Robotics Co. Ltd.

- 6.4.3 SIASUN Robot and Automation Co. Ltd.

- 6.4.4 LG Electronics Inc.

- 6.4.5 SoftBank Robotics Corp.

- 6.4.6 Omron Corp.

- 6.4.7 Hyundai Robotics Co. Ltd.

- 6.4.8 Panasonic Holdings - Robotics BU

- 6.4.9 DJI Innovations

- 6.4.10 Geek+ Robotics Co. Ltd.

- 6.4.11 Milagrow HumanTech

- 6.4.12 Reeman Intelligent Tech

- 6.4.13 Rainbow Robotics Co. Ltd.

- 6.4.14 Roborock Technology Co. Ltd.

- 6.4.15 UB-Tech (Shanghai) Intelligent

- 6.4.16 Yamaha Motor - Robotics BU

- 6.4.17 Doosan Robotics Inc.

- 6.4.18 Hanwha Robotics

- 6.4.19 Keenon Robotics

- 6.4.20 TMi Robotics (TMiRob)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment