PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939118

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939118

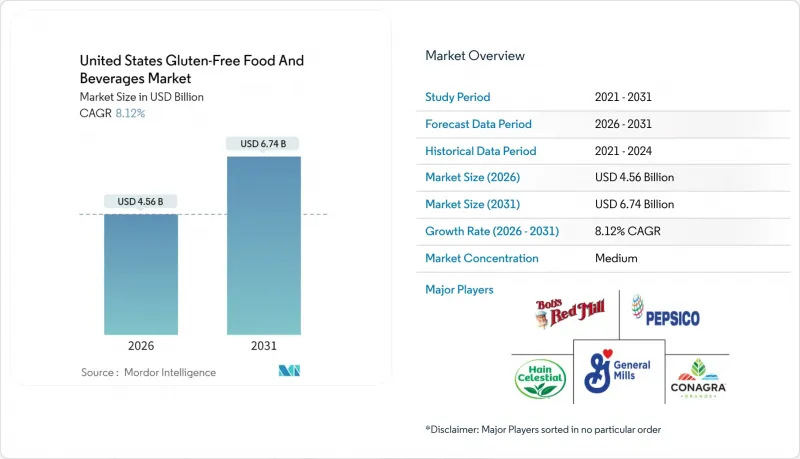

United States Gluten-Free Food And Beverages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States gluten-free food and beverages market size in 2026 is estimated at USD 4.56 billion, growing from 2025 value of USD 4.22 billion with 2031 projections showing USD 6.74 billion, growing at 8.12% CAGR over 2026-2031.

The rising awareness about celiac disease and the adoption of special dietary lifestyles primarily drive the market. This has resulted in a shift in consumer preference from conventional products toward gluten-free processed foods. The demand for gluten-free food and beverages is constantly rising due to the increased cases of gluten intolerance among customers. The usage of genetically modified crops and sensitivity to gut health are among the major reasons that have altered the digestive tracts of the human body, leading to the intolerance of gluten products. The demand for gluten-free food and beverages is also driven by consumers inclined toward fitness and a healthy diet. As gluten products are commonly filled with carbohydrates and other fats, consumers in the market are choosing gluten-free product options.

United States Gluten-Free Food And Beverages Market Trends and Insights

Rising awareness of celiac disease and gluten intolerance

The prevalence of celiac disease in the United States is approximately 1%, with enhanced screening methods revealing varying diagnosis rates across ethnic groups: 1.08% in White populations, 0.36% in Hispanic populations, and 0.16% in Black Americans, according to ahqr.gov. Non-celiac gluten sensitivity affects approximately 6% of consumers, significantly expanding the market beyond those with medical requirements. Healthcare providers now regularly screen adults with persistent unexplained symptoms, including digestive issues, fatigue, and skin conditions, leading to consistent growth in new gluten-free consumers. Product manufacturers have developed ethnically diverse offerings, including Mexican-style tortillas, Southern cornbread mixes, and traditional ethnic breads adapted to gluten-free formulations. This market expansion has transformed gluten-free products from a medical necessity to a mainstream dietary choice, supporting demand across both premium and value product segments and driving innovation in taste, texture, and nutritional profiles.

Government regulations supporting gluten-free labeling

The FDA's 21 CFR 101.91 regulation requires products labeled "gluten-free" to contain less than 20 parts per million (ppm) of gluten. In 2024, the FDA expanded documentation requirements to include fermented and hydrolyzed foods. While national standards facilitate interstate commerce and increase consumer confidence, they create significant compliance challenges for small producers without established testing capabilities. Large manufacturers can better absorb compliance costs through economies of scale and use certifications as a competitive advantage in the market. The regulatory framework encourages companies to invest in dedicated production facilities and testing laboratories, which increases product variety and reduces cross-contamination risks. This investment in infrastructure and quality control measures helps manufacturers maintain consistent gluten-free standards across their product lines and ensures compliance with FDA regulations. The standardization of gluten-free requirements has also led to improved supply chain management and more rigorous supplier verification processes throughout the industry.

Higher cost of gluten-free products compared to conventional ones

The higher prices of gluten-free products stem from specialized ingredients, dedicated production lines, and rigorous testing protocols. These products require separate manufacturing facilities to prevent cross-contamination and undergo extensive quality control measures to ensure safety. Consumers who require gluten-free products for medical conditions often express concerns about the elevated pricing, particularly those with celiac disease who have no alternative options. Retailers are addressing this through private-label offerings and promotional discounts, while manufacturers are expanding production capacity to reduce overhead costs. Many companies are investing in automated production systems and establishing direct relationships with ingredient suppliers to optimize costs. The price difference between gluten-free and conventional products is expected to decrease as production efficiency improves and demand stabilizes, driven by technological advancements in manufacturing processes and increased competition in the market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing health consciousness among consumers

- Growth in E-commerce and online retail channels

- Risk of cross-contamination during manufacturing processes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bakery products hold the largest market share at 40.78% in 2025, supported by significant advancements in gluten-free flour formulations that improve taste and texture quality. These improvements address historical challenges in replicating traditional wheat-based products, particularly in bread, pastries, and cookies. The beverages segment is projected to grow at 11.32% CAGR through 2031, as consumers increasingly seek functional and clean-label alternatives, including plant-based milk alternatives, protein shakes, and fortified drinks. The market players are catering to this trend by launching new products in the market. For instance, in March 2024, Tirlan launched a new Truly Gluten Free Premium Irish Oat drink made with Irish oats into the US market.

Snacks and ready-to-eat products maintain a strong market presence through efficient manufacturing processes and innovative packaging solutions that extend shelf life while preserving product integrity. The condiments, seasonings, and spreads segments grow by implementing dedicated production processes that minimize cross-contamination risks, with manufacturers investing in separate production lines and stringent quality control measures. The dairy and dairy substitutes category expands through plant-based offerings, exemplified by companies such as Lil Bucks, which produces sprouted buckwheat products targeting younger consumers with high protein and fiber content. These products incorporate innovative ingredients and processing techniques to match traditional dairy products' taste and nutritional profiles.

The United States Gluten-Free Food and Beverages Market Report is Segmented by Product Type (Bakery Products, Snacks and RTE Products, Beverages, and More), by Source (Animal-Based and Plant-Based), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialist Retailers, and More), and Region (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- General Mills Inc.

- Conagra Brands Inc.

- PepsiCo Inc.

- The Hain Celestial Group Inc.

- Bob's Red Mill Natural Foods, Inc.

- Dawn Food Products Inc.

- Mars, Incorporated

- The Coca-Cola Company

- Amy's Kitchen Inc.

- The Kraft Heinz Company

- B&G Foods Inc.

- DR SCHAR AG/S.p.A.

- Flowers Foods, Inc.

- Mondel?z International, Inc

- SACO Foods, Inc.

- English Bay Chocolate Factory ULC

- Blue Diamond Growers

- Namaste Foods, LLC

- Quinn Foods LLC

- Dare Foods Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising awareness of celiac disease and gluten intolerance

- 4.2.2 Government regulations supporting gluten-free labeling

- 4.2.3 Increasing health consciousness among consumers

- 4.2.4 Growth in E-commerce and online retail channels

- 4.2.5 Growth in demand for clean-label and allergen-free products

- 4.2.6 Celebrity endorsements and media influence promoting gluten-free diets

- 4.3 Market Restraints

- 4.3.1 Higher cost of gluten-free products compared to conventional ones

- 4.3.2 Risk of cross-contamination during manufacturing processes

- 4.3.3 Challenges in replicating taste and texture of gluten-containing products

- 4.3.4 Lack of standardization in gluten-free certification

- 4.4 Regulatory Landscape

- 4.5 Technology Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bakery Products

- 5.1.1.1 Breads and Cakes

- 5.1.1.2 Cookies and Biscuits

- 5.1.1.3 Other Bakery Products

- 5.1.2 Snacks and RTE Products

- 5.1.3 Beverages

- 5.1.4 Condiments, Seasonings and Spreads

- 5.1.5 Dairy and Dairy Substitutes

- 5.1.6 Meats and Meat Substitutes

- 5.1.7 Other Gluten-Free Products

- 5.1.1 Bakery Products

- 5.2 By Source

- 5.2.1 Plant-Based

- 5.2.2 Animal-Based

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Specialist Retailers

- 5.3.4 Online Retail Stores

- 5.3.5 Other Distribution Channels

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Mills Inc.

- 6.4.2 Conagra Brands Inc.

- 6.4.3 PepsiCo Inc.

- 6.4.4 The Hain Celestial Group Inc.

- 6.4.5 Bob's Red Mill Natural Foods, Inc.

- 6.4.6 Dawn Food Products Inc.

- 6.4.7 Mars, Incorporated

- 6.4.8 The Coca-Cola Company

- 6.4.9 Amy's Kitchen Inc.

- 6.4.10 The Kraft Heinz Company

- 6.4.11 B&G Foods Inc.

- 6.4.12 DR SCHAR AG/S.p.A.

- 6.4.13 Flowers Foods, Inc.

- 6.4.14 Mondel?z International, Inc

- 6.4.15 SACO Foods, Inc.

- 6.4.16 English Bay Chocolate Factory ULC

- 6.4.17 Blue Diamond Growers

- 6.4.18 Namaste Foods, LLC

- 6.4.19 Quinn Foods LLC

- 6.4.20 Dare Foods Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK