PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844584

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844584

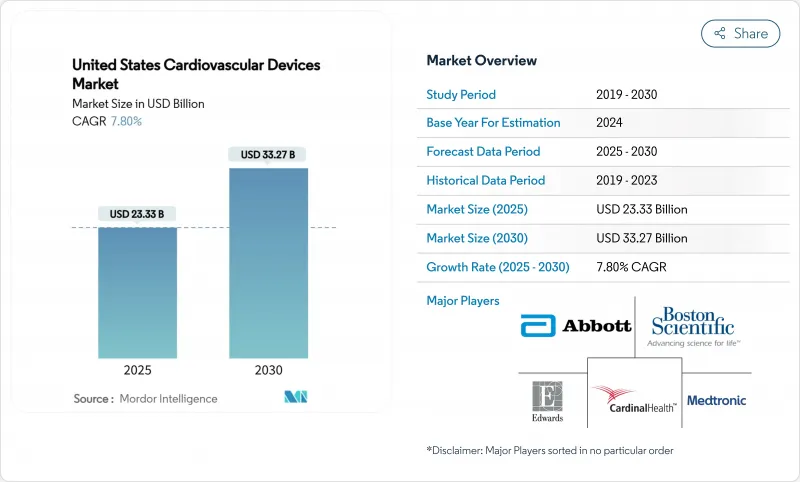

United States Cardiovascular Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States cardiovascular devices market size was USD 23.33 billion in 2025 and is on track to reach USD 33.27 billion in 2030, expanding at a 7.36% CAGR during 2025-2030.

Growth stems from rising cardiovascular disease prevalence-affecting 126.9 million adults-and steady procedure volumes that stimulate recurring device demand. Artificial-intelligence-enabled diagnostics, transcatheter therapeutic breakthroughs, and payment reforms that reward cost-saving technologies are reshaping competitive priorities. Providers increasingly bundle diagnostic and interventional tools to secure volume-based discounts, subtly shifting bargaining power toward large health systems. Venture-capital inflows, particularly in structural-heart start-ups, expand the innovation pipeline even as hospital capital constraints intensify.

United States Cardiovascular Devices Market Trends and Insights

Obesity-linked PAD surge driving use of drug-coated balloons

Peripheral artery disease now affects 10 million Americans, with 2 million facing critical limb-threatening ischemia. Trial evidence showing a 51.3% fall in target-lesion failure after sirolimus delivery is accelerating hospital adoption of drug-coated balloons, especially for below-the-knee work. Hospitals in high-obesity Southern states are restocking coated balloons, while large systems negotiate multiprocedure discounts that lower per-unit pricing. Device makers respond by adding smaller diameters and extended coating life to suit infrapopliteal anatomy. Payers increasingly cover these balloons once registry data confirm reduced repeat interventions, reinforcing uptake momentum.

ACC/AHA reimbursement revisions incentivizing CRT-D upgrades

The 2025 criteria broaden access to cardiac resynchronization therapy defibrillators and reward extended battery life, yielding USD 15,120 in Medicare savings per patient over six years. Hospitals are pre-ordering premium CRT-D models to capture both clinical benefit and cost share. Early claims data reveal a 17% year-on-year jump in elective generator replacements as providers expedite swaps before older devices reach elective-replacement indicators. Manufacturers highlight remote-monitoring firmware that dovetails with home-care expansion, strengthening the therapy's economic case.

Venture-capital influx into percutaneous mitral repair start-ups

Capstan Medical's USD 110 million Series C epitomizes investor faith in mitral and tricuspid valves, a field where half of severe mitral-regurgitation patients still lack surgery. Venture backing lets entrants lock in premium component pricing and run longer trials, positioning them as attractive acquisition targets. Structural-heart majors now allocate dedicated scouting teams to incubators, intensifying competition for intellectual property. Hospitals anticipate broader device menus that can tailor therapy to anatomy and comorbidity, potentially lifting procedure counts.

Other drivers and restraints analyzed in the detailed report include:

- Growth of office-based & ASC cath-labs via CMS site-of-service differential

- Hospital capital budget freezes after Medicare rate cuts

- Stringent regulatory requirements and product recalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic & surgical products captured 77.20% of United States cardiovascular devices market share in 2024, underpinned by stents, valve implants, and rhythm-management devices that anchor high-value procedures. Drug-eluting stents remain mainstay, yet bioresorbable options and intravascular lithotripsy catheters-now under Johnson & Johnson-offer added revenue streams. Physicians value single-vendor kits that bundle guidewires and imaging catheters, a tactic that deepens wallet share for integrated suppliers.

Diagnostic & monitoring devices are forecast to clock an 8.56% CAGR to 2030, the fastest of any category. Cloud analytics such as EchoGo Amyloidosis, which posts 84.5% sensitivity and 89.7% specificity, convert ultrasound systems into subscription revenue. Growing reliance on remote physiologic monitoring pushes device makers to embed cellular radios, shifting BOM cost to connectivity chips while opening service-fee income.

The United States Cardiovascular Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices [ECG Systems, Remote Cardiac Monitor, and More], Therapeutic & Surgical Devices [Coronary Stents, Catheters, Cardiac Rhythm Management, Heart Valves, Ventricular Assist Devices, and More]), Indication (Coronary Artery Disease, Arrhythmia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Edward Lifesciences

- Johnson & Johnson

- Terumo

- Beckton Dickinson

- W. L. Gore & Associates

- Siemens Healthineers

- MicroPort CRM (MicroPort Scientific)

- BIOTRONIK

- LivaNova

- Getinge

- Teleflex

- Cordis

- Merit Medical Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Obesity-Linked PAD Surge Driving Use of Drug-Coated Balloons

- 4.2.2 ACC/AHA Reimbursement Revisions Incentivizing CRT-D Upgrades

- 4.2.3 Growth of Office-Based & ASC Cath-Labs via CMS Site-of-Service Differential

- 4.2.4 Venture Capital Influx into Percutaneous Mitral Repair Start-ups

- 4.2.5 Rapid Adoption of TAVR Post-FDA Low-Risk Approval & Expanded CMS Coverage

- 4.2.6 Infection-Control Policies Boosting Demand for Single-Use Diagnostic Catheters

- 4.3 Market Restraints

- 4.3.1 Hospital Capital Budget Freezes After Medicare Rate Cuts

- 4.3.2 Stringent regulatory requirements and product recall

- 4.3.3 Semiconductor Shortages Disrupting ICD Generator Supply

- 4.3.4 Stringent 510(k) Predicate Requirements for Bioresorbable Scaffolds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 ECG Systems

- 5.1.1.2 Remote Cardiac Monitor

- 5.1.1.3 Cardiac MRI

- 5.1.1.4 Cardiac CT

- 5.1.1.5 Echocardiography / Ultrasound

- 5.1.1.6 Fractional Flow Reserve (FFR) Systems

- 5.1.2 Therapeutic & Surgical Devices

- 5.1.2.1 Coronary Stents

- 5.1.2.1.1 Drug-Eluting Stents

- 5.1.2.1.2 Bare-Metal Stents

- 5.1.2.1.3 Bioresorbable Stents

- 5.1.2.2 Catheters

- 5.1.2.2.1 PTCA Balloon Catheters

- 5.1.2.2.2 IVUS/OCT Catheters

- 5.1.2.3 Cardiac Rhythm Management

- 5.1.2.3.1 Pacemakers

- 5.1.2.3.2 Implantable Cardioverter Defibrillators

- 5.1.2.3.3 Cardiac Resynchronization Therapy Devices

- 5.1.2.4 Heart Valves

- 5.1.2.4.1 TAVR/TAVI

- 5.1.2.4.2 Mechanical Valves

- 5.1.2.4.3 Tissue/Bioprosthetic Valves

- 5.1.2.5 Ventricular Assist Devices

- 5.1.2.6 Artificial Hearts

- 5.1.2.7 Grafts & Patches

- 5.1.2.8 Other Cardiovascular Surgical Devices

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Indication

- 5.2.1 Coronary Artery Disease

- 5.2.2 Arrhythmia

- 5.2.3 Heart Failure

- 5.2.4 Valvular Heart Disease

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Home care Settings

- 5.3.3 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Medtronic plc

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corporation

- 6.3.4 Edwards Lifesciences Corporation

- 6.3.5 Johnson & Johnson

- 6.3.6 Terumo Corporation

- 6.3.7 Becton, Dickinson and Company

- 6.3.8 W. L. Gore & Associates, Inc.

- 6.3.9 Siemens Healthineers AG

- 6.3.10 MicroPort CRM (MicroPort Scientific)

- 6.3.11 Biotronik

- 6.3.12 LivaNova PLC

- 6.3.13 Getinge AB

- 6.3.14 Teleflex Incorporated

- 6.3.15 Cordis Corporation

- 6.3.16 Merit Medical Systems, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment