PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844590

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844590

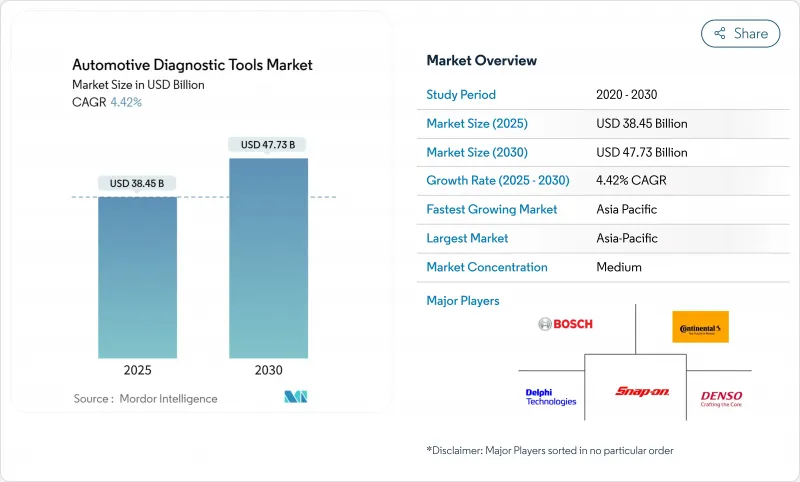

Automotive Diagnostic Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The automotive diagnostic tools market size stood at USD 38.45 billion in 2025 and is forecast to reach USD 47.73 billion by 2030, growing at a 4.42% CAGR.

Software-defined vehicle platforms, tighter cybersecurity norms, and electrification mandates are steering tool specifications toward high-voltage safety, remote connectivity, and cloud analytics. Wireless interfaces, over-the-air update support, and ISO/SAE 21434-ready encryption now form baseline purchase criteria for large service networks. Platform integration strategies that bundle fault-code reading, ADAS calibration, and predictive maintenance analytics on a single screen are gaining traction with dealers and fleet operators. Asia-Pacific supplies the strongest volume pull as regional electric-vehicle output and government subsidies accelerate scan-tool adoption.

Global Automotive Diagnostic Tools Market Trends and Insights

Rapid electrification of powertrains

Battery-electric models use high-voltage circuits, thermal packs, and bidirectional chargers that standard OBD-II readers cannot interrogate. California will require a unified EV diagnostic interface by 2026, forcing tool vendors to decode battery health, insulation resistance, and charger faults across brands. Charging-station analyzers such as Fluke FEV150 now join service bays to validate grid interaction. Suppliers answer with purpose-built EV testers like THINKTOOL CE EVD, covering more than 80 brands. Workforce certification lags vehicle rollout, so data-rich tools that guide less-experienced technicians win share.

Tightening OBD-III/remote diagnostics rules

SAE J1979-2 obliges combustion-engine vehicles sold from 2027 to support unified diagnostic services, while the forthcoming J1979-3 standard targets zero-emission models. CARB and EU regulators also press for real-time, cloud-based fault reporting that shifts service from the garage to the data center. Large tool makers invest in secure-gateway credentials and ISO/SAE 21434 processes that small rivals may struggle to fund. Heavy-duty engines above 14,000 lb GVWR face parallel monitoring mandates under 40 CFR 86.010-18. Remote architecture enables fleets to schedule service before breakdowns, reducing unplanned downtime.

High up-front cost of advanced scan tools

Top-tier ADAS calibration rigs and high-voltage analyzers can exceed USD 50,000 per bay, a stretch for small garages. Japan's subsidy of up to JPY 160,000 per shop offsets only a fraction of the total hardware plus training spend. Subscription updates compound ownership cost yet remain essential for secure-gateway access. These economics push independents toward franchise networks or remote-service platforms such as asTech that rent OEM tools on demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing demand for predictive maintenance analytics

- Rising global light-vehicle parc

- Cyber-security certification hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OBD scanners secured the largest slice of the automotive diagnostic tools market at 44.58% in 2024 because they work on every post-1996 passenger model. The automotive diagnostic tools market size attached to this category still grows, yet modern service bays demand combined ADAS, high-voltage, and cloud-sync features that legacy handhelds lack. Snap-on's spring 2025 code library adds millions of tests and secure gateways for Mercedes-Benz, underscoring the race to embed OEM depth inside universal hardware.

Electric-System analyzers, posting the fastest 6.18% CAGR, hinge on Bluetooth 5.0 and dual-band Wi-Fi modules that maintain throughput during live telemetry uploads. Pressure leak testers and battery insulation probes complement the core scanner by ensuring thermal safety in EV packs, with Redline Detection equipment gaining fleet-safety endorsements. Suppliers integrate multiple sensor harnesses into one chassis to spread cost across tasks and justify price premiums amid budget-sensitive workshops.

Passenger cars retained 61.35% of the automotive diagnostic tools market share in 2024, supported by routine emissions and safety inspections. Fleet-oriented vans and trucks, however, drive tool specification trends. Light commercial vehicles grow at 6.35% CAGR to 2030 as e-commerce accelerates delivery cycles that punish downtime. Platforms like International Trucks' OnCommand Connection feed real-time performance data to cloud dashboards, prompting proactive service orders that cut roadside events.

Heavy rigs over 14,000 lb GVWR comply with stricter CFR diagnostics, expanding protocol support requirements inside multi-brand devices. Bosch Vehicle Health reports now highlight coolant and oil deviations on mixed fleets, letting maintenance managers address issues before engine damage. As electrification reaches delivery vans, tool makers must bridge combustion and battery analytics in a single workflow, smoothing technician learning curves and inventory.

The Automotive Diagnostic Scan Tools Market Report is Segmented by Tool Type (OBD Scanners, Professional Scan Tools, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion (Internal Combustion Engine and More), Connectivity (Wired and Wireless and Bluetooth / Wi-Fi), End User (OEM Dealerships and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific holds 36.41% of the automotive diagnostic tools market share in 2024 and expands the fastest at 7.84% CAGR. China's 50% surge in EV production during 2023, plus a 10 trillion-yuan automotive revenue base, keeps tool demand buoyant. Beijing's push toward autonomous-mobility fleets by 2025 requires V2X-aware diagnostics that validate radar alignment and lidar cleanliness before dispatch. Japan begins obligatory OBD inspections in October 2024 and subsidizes scan-tool purchases for workshops to ensure compliance. India's aftermarket joint ventures between ASK Auto and AISIN extend parts and service networks across South Asia, lifting scan-tool penetration in tier-2 cities.

North America follows with strong regulatory momentum. California's Advanced Clean Cars II rule forces standardized EV diagnostics by 2026, and CARB pilots remote-OBD concepts that remove the need for physical inspection visits. Fleets adopt Uptake's AI health reports to optimize maintenance budgets, reinforcing tool upgrades that push data into cloud dashboards. OEM dealerships add secure-gateway unlocks for brands like Mercedes-Benz through Snap-on's 2025 software wave.

Europe aligns with UN R155 cybersecurity rules that demand type-approval audits for diagnostic interfaces. Large suppliers embed ISO/SAE 21434 frameworks to meet these audits, and franchise workshops benefit from corporate compliance coverage. Training schemes certified by the Institute of the Motor Industry close skill gaps, especially for high-voltage servicing.

- Robert Bosch GmbH

- Snap-on Inc.

- Continental AG

- Delphi/BorgWarner Technologies

- ACTIA Group

- Autel Intelligent Tech

- Launch Tech Co.

- Softing AG

- Vector Informatik GmbH

- KPIT Technologies Ltd.

- Hella KGaA Hueck & Co.

- Texa S.p.A.

- Siemens Digital Industries Software

- Foxwell Tech

- OBD Solutions LLC

- Denso Corporation

- Innova Electronics

- Pico Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid electrification of powertrains

- 4.2.2 Tightening OBD-III/remote diagnostics regulations (U.S., EU)

- 4.2.3 Growing demand for predictive maintenance analytics

- 4.2.4 Rising global light-vehicle parc

- 4.2.5 Integration of OTA software update diagnostics

- 4.2.6 Escalating in-vehicle electronics complexity

- 4.3 Market Restraints

- 4.3.1 High up-front cost of advanced scan tools

- 4.3.2 Cyber-security certification hurdles for connected tools

- 4.3.3 Skills gap in independent aftermarket workshops

- 4.3.4 Fragmented communication standards across OEMs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Tool Type

- 5.1.1 OBD Scanners

- 5.1.2 Professional Scan Tools

- 5.1.3 Electric-System Analyzers

- 5.1.4 Pressure & Leak Testers

- 5.1.5 Code Readers

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Propulsion

- 5.3.1 Internal Combustion Engine

- 5.3.2 Battery-Electric Vehicle

- 5.3.3 Hybrid & Plug-in Hybrid

- 5.4 By Connectivity

- 5.4.1 Wired

- 5.4.2 Wireless / Bluetooth / Wi-Fi

- 5.5 By End User

- 5.5.1 OEM Dealerships

- 5.5.2 Independent Aftermarket Garages

- 5.5.3 Fleet Operators

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Snap-on Inc.

- 6.4.3 Continental AG

- 6.4.4 Delphi/BorgWarner Technologies

- 6.4.5 ACTIA Group

- 6.4.6 Autel Intelligent Tech

- 6.4.7 Launch Tech Co.

- 6.4.8 Softing AG

- 6.4.9 Vector Informatik GmbH

- 6.4.10 KPIT Technologies Ltd.

- 6.4.11 Hella KGaA Hueck & Co.

- 6.4.12 Texa S.p.A.

- 6.4.13 Siemens Digital Industries Software

- 6.4.14 Foxwell Tech

- 6.4.15 OBD Solutions LLC

- 6.4.16 Denso Corporation

- 6.4.17 Innova Electronics

- 6.4.18 Pico Technology Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Remote Diagnostics-as-a-Service

- 7.2 ADAS & Autonomous Calibration Tools

- 7.3 Subscription-based Software Licensing