PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844616

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844616

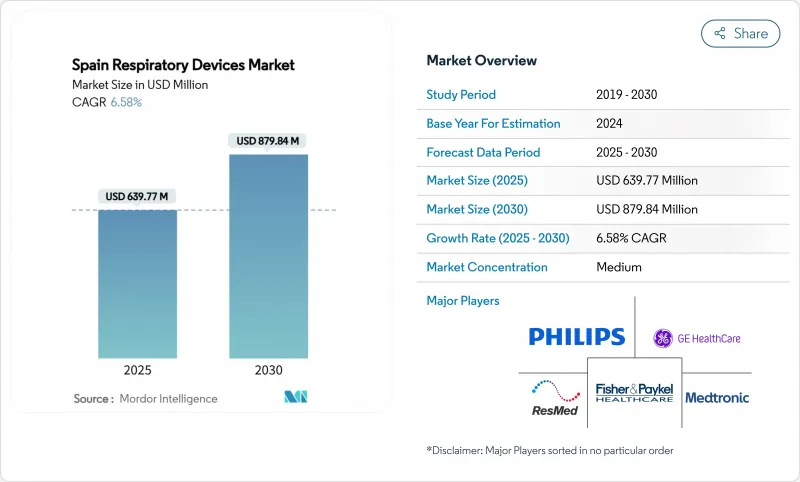

Spain Respiratory Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Spain Respiratory Devices Market size is estimated at USD 639.77 million in 2025, and is expected to reach USD 879.84 million by 2030, at a CAGR of 6.58% during the forecast period (2025-2030).

Robust public health coverage, the rapid expansion of home-based care, and continuous innovation in therapeutic equipment underpin this trajectory. Accelerated population ageing intensifies demand for ventilators and oxygen systems, while a growing burden of chronic obstructive pulmonary disease (COPD) and sleep apnea broadens the addressable patient pool. Government incentives that promote local manufacturing and digital health adoption further support revenue growth. At the same time, heightened regulatory costs, workforce shortages, and stricter environmental rules temper short-term momentum yet encourage scale advantages for established suppliers.

Spain Respiratory Devices Market Trends and Insights

Growing Prevalence of COPD, Asthma, Tuberculosis, and Sleep Apnea

COPD affects 11.8% of Spanish adults and drove a 35.9% rise in hospital discharges for respiratory diseases, a pattern that strengthens long-term sales of ventilators, nebulizers, and spirometers. Sleep apnea remains widely underdiagnosed despite affecting nearly half of older adults at elevated dementia risk, creating fresh headroom for positive airway pressure devices and home sleep testing kits. Advances in tuberculosis PCR kits with 100% sensitivity expand demand for portable diagnostic systems in public health laboratories. Together, these epidemiological shifts lengthen device replacement cycles and enlarge the Spain respiratory devices market far beyond acute care settings.

Rapid Ageing of Spain's Population

The cohort aged 90 years or older swelled 58.29% from 2013 to 2023, reaching 608,321 citizens. An ageing index of 142.35% highlights growing demand for non-invasive ventilation, oxygen concentrators, and airway clearance devices tailored to home use. With single-person households forecast to account for 33.5% of all households by 2039, manufacturers prioritise intuitive interfaces and remote monitoring features that let older adults remain independent. Hospitals already maintain dedicated non-invasive ventilation units in 83% of facilities, signalling sustained procurement for ageing-related disorders. These demographic realities embed structural growth in the Spain respiratory devices market.

High Upfront Cost of Advanced Devices

Hospitals operate under strict budget ceilings even after recent public-health outlays, causing extended procurement cycles for premium ventilators and AI-enabled monitors. Regional authorities lean on cost-per-quality-adjusted-life-year thresholds that favour proven mid-range products. The Canary Islands' decision to reduce its IGIC tax on medical devices to zero illustrates how targeted fiscal levers can mitigate affordability constraints. In the absence of nationwide VAT relief, price sensitivity will continue to cap immediate growth in the Spain respiratory devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Home-based Respiratory Care and Tele-monitoring

- Surge in e-cigarette-related Lung Injuries

- EU MDR Compliance Delaying Product Launches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic devices accounted for 56.54% of 2024 revenue, reflecting a clinical preference for continuous airway pressure systems, ventilators, and oxygen concentrators. Positive airway pressure innovations such as KPAP enhance comfort and adherence among sleep apnea patients, locking in recurring mask and tubing sales. Ventilator development programs funded under national recovery schemes lower price barriers, further widening penetration. Nebulizers remain critical for COPD management, while portable oxygen systems support growing homecare demand. The Spain respiratory devices market size for therapeutic equipment is projected to rise in tandem with ageing-linked comorbidities.

Diagnostic and monitoring devices hold a smaller base but record the fastest 7.65% CAGR. Connected spirometers, wearable capnographs, and home sleep tests gain popularity amid wider telehealth rollouts. Early diagnosis of respiratory disease lowers hospital admissions, strengthening policy support for screening tools. As a result, diagnostic platforms capture a rising share of the Spain respiratory devices market.

The Spain Respiratory Devices Market Report is Segmented by Product Type (Diagnostic & Monitoring Devices, Therapeutic Devices, Disposables), Indication (COPD, Asthma, Sleep Apnea, Cystic Fibrosis, Tuberculosis, Other Respiratory Disorders), End User (Hospitals and Clinics, Homecare Settings, Ambulatory Surgical Centers, Long-Term Care Facilities), and Geography (Spain). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Koninklijke Philips

- Resmed

- Dragerwerk AG

- Fisher & Paykel Healthcare

- Medtronic

- Hamilton Medical

- GE Healthcare

- Smiths Medical MD, Inc.

- Fosun Pharma (Breas Medical AB)

- Invacare

- GlaxoSmithKline

- Rotech Healthcare

- Becton Dickinson & Co.

- Air Liquide

- Teleflex

- Drive DeVilbiss Healthcare

- Apex Medical

- Lowenstein Medical GmbH

- Vyaire Medical

- Vapotherm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of COPD, Asthma, TB & Sleep-Apnea

- 4.2.2 Rapid Ageing of Spain's Population

- 4.2.3 Expansion of Home-Based Respiratory Care & Tele-Monitoring

- 4.2.4 Surge In E-Cigarette-Related Lung Injuries

- 4.2.5 Post-COVID Government Incentives for Local Ventilator Output

- 4.2.6 Adoption of AI-Enabled Predictive Maintenance for Ventilators

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Advanced Devices

- 4.3.2 EU MDR Compliance Delaying Product Launches

- 4.3.3 Shortage of Respiratory Therapists

- 4.3.4 Environmental Curbs on Single-Use Plastics In Disposables

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 Spirometers

- 5.1.1.2 Sleep Test Devices

- 5.1.1.3 Peak Flow Meters

- 5.1.1.4 Other Diagnostic & Monitoring Devices

- 5.1.2 Therapeutic Devices

- 5.1.2.1 Positive Airway Pressure (PAP) Devices

- 5.1.2.2 Humidifiers

- 5.1.2.3 Nebulizers

- 5.1.2.4 Ventilators

- 5.1.2.5 Inhalers

- 5.1.2.6 Oxygen Concentrators

- 5.1.2.7 Other Therapeutic Devices

- 5.1.3 Disposables

- 5.1.3.1 Breathing Circuits

- 5.1.3.2 Masks

- 5.1.3.3 Filters

- 5.1.3.4 Other Disposables

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Indication

- 5.2.1 COPD

- 5.2.2 Asthma

- 5.2.3 Sleep Apnea

- 5.2.4 Cystic Fibrosis

- 5.2.5 Tuberculosis

- 5.2.6 Other Respiratory Disorders

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Homecare Settings

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Long-term Care Facilities

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Koninklijke Philips N.V.

- 6.3.2 ResMed

- 6.3.3 Dragerwerk AG

- 6.3.4 Fisher & Paykel Healthcare Ltd

- 6.3.5 Medtronic plc

- 6.3.6 Hamilton Medical AG

- 6.3.7 GE HealthCare

- 6.3.8 Smiths Medical MD, Inc.

- 6.3.9 Fosun Pharma (Breas Medical AB)

- 6.3.10 Invacare Corporation

- 6.3.11 GlaxoSmithKline plc

- 6.3.12 Rotech Healthcare Inc.

- 6.3.13 Becton Dickinson & Co.

- 6.3.14 Air Liquide Healthcare

- 6.3.15 Teleflex Inc.

- 6.3.16 DeVilbiss Healthcare LLC

- 6.3.17 Apex Medical Corp.

- 6.3.18 Lowenstein Medical GmbH

- 6.3.19 Vyaire Medical Inc.

- 6.3.20 Vapotherm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment