PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844621

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844621

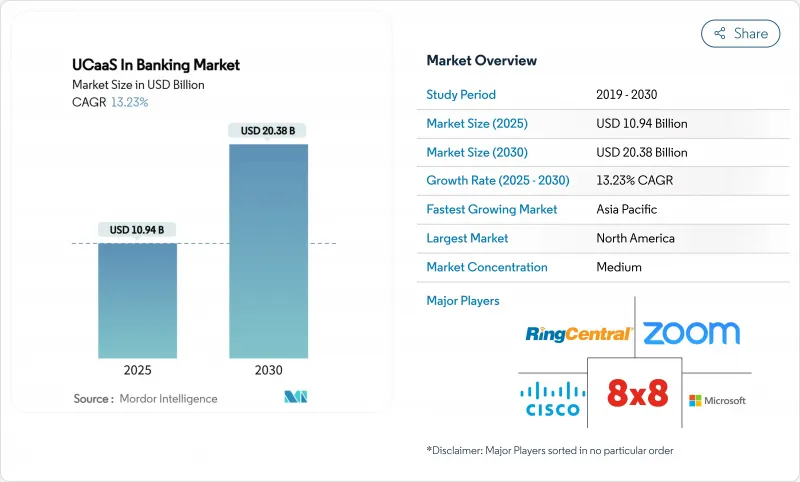

UCaaS In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The UCaaS in banking market size stood at USD 10.94 billion in 2025 and is forecast to reach USD 20.38 billion by 2030, advancing at a 13.23% CAGR.

The expansion reflects a decisive industry shift toward cloud-native communications that sustain hybrid workforces and satisfy strict regulatory audit trails. Heightened demand for seamless customer engagement, accelerated fintech partnerships, and accelerated time-to-market for new digital products further uplift adoption. Public-cloud UCaaS remains pervasive, yet hybrid architectures are gaining ground as banks seek fine-grained data-sovereignty control without forfeiting the flexibility of elastic capacity. Strategic deployments-such as Barclays' global roll-out of Microsoft Teams-spotlight how integrated platforms rationalize legacy voice estates, consolidate collaboration tools and contain total cost of ownership. Competitive intensity is shaped by telecom incumbents battling cloud-native specialists that embed artificial-intelligence (AI) functions such as real-time language translation, sentiment scoring and compliance surveillance.

Global UCaaS In Banking Market Trends and Insights

BYOD and Workforce Mobility

Banking institutions are dismantling desk-phone dependencies as hybrid workforces normalize personal device use. UCaaS tools that encrypt traffic end-to-end, enforce role-based policies and federate identity allow staff to connect from any location without jeopardizing compliance. Mizuho Securities' decision to migrate external communications to Zoom under an active-host billing model underscores how flexible licensing reduces dormant seat costs while sustaining auditability. BYOD strategies cut hardware outlays and elevate employee satisfaction, yet they demand advanced mobile-device-management and geo-fencing to meet sectoral data-loss-prevention rules. The interplay between mobility enablement and UCaaS security solidifies competitive advantage for banks able to blend flexibility with rigorous supervision.

Need for Enterprise-wide UC Integration

Historically, siloed voice, chat and trading-floor channels obstructed fluid collaboration. Contemporary UCaaS platforms unify these touchpoints and embed workflow triggers so alerts and documents flow between branches, contact centers and compliance desks. NTT Communications underpins more than 190 countries with a single-tenant global UC fabric, allowing multinational banks to standardize dial plans, reporting and policy enforcement while trimming maintenance overhead. Integration imperatives intensify during mergers, when newly acquired branches must migrate rapidly. Leading solutions now apply AI to route queries to the best-suited specialist, elevating first-call-resolution metrics and optimizing workforce allocation. Unified lineage across channels also simplifies e-discovery requests, which regulators expect within hours.

Low Cloud-UC Awareness in Tier-2/3 Banks

Community institutions often lack specialist staff to evaluate UCaaS proposals, defaulting to incumbent telcos for plain-old telephony. A U.S. Treasury-commissioned assessment warns that limited cloud acumen exposes smaller banks to hidden resiliency and cyber risks, prolonging legacy usage and constraining modernization. Educational accelerators, blueprint templates and managed-service bundles therefore play a pivotal role in lowering entry barriers. Providers that extend migration incentives, turnkey security controls and regulatory documentation can unlock this underserved cohort.

Other drivers and restraints analyzed in the detailed report include:

- Digital-only Banking Expansion

- AI-Enabled UCaaS for Compliance Monitoring

- Stringent Data-Security and Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephony accounted for 42.5% of the UCaaS in banking market size in 2024 as voice remains indispensable for fraud verification, trade execution and customer identity confirmation. Collaboration suites, however, are projected to drive an 18.50% CAGR through 2030 as video, persistent chat and shared-document workspaces coalesce into a single pane. The convergence reduces swivel-chair actions for relationship managers, speeding onboarding and issue resolution. Five9 reports that natural-language-processing routers now direct 80% of inbound calls to the correct skill group without human triage, trimming abandonment rates. Unified messaging compresses email, SMS and secure chat feeds into threaded histories, boosting compliance auditability. Video-banking kiosks extend advisory services to rural zones, while communication-platform APIs embed two-factor-authentication voice calls directly into mobile apps. This modularity ensures banks add channels without re-architecting back-end cores, reinforcing platform stickiness and raising switching costs.

Demand for embedded communications intensifies as banks deploy contextual notifications-loan-approval pings, FX-rate alerts and card-usage anomalies-through in-app banners, RCS and OTT messengers. Webex CPaaS banking modules deliver out-of-the-box templates for WhatsApp and Apple Messages, accelerating deployment while retaining encryption and audit logging. Such API-first models empower developers to orchestrate journeys where a chatbot escalates to secure video when high-value transactions exceed preset thresholds. Gartner predicts that by 2030, API-driven channels will account for half of financial-services outbound traffic, underscoring telephony's gradual transition from standalone product to foundational service within integrated suites.

Public-cloud captured 61.4% of UCaaS in banking market share in 2024 on the back of turnkey scalability and consumption pricing. Yet hybrid approaches, forecasting a 19.20% CAGR to 2030, reflect heightened boardroom focus on jurisdictional compliance and latency-sensitive workloads. First Horizon Bank's Webex Contact Center migration showcased a layered architecture where recordings of regulated staff remained on-prem while AI analytics processed anonymized data in Cisco's multitenant cloud. This blueprint allowed the bank to maintain 20,000 endpoints and 750 agents under one console without breaching fiduciary data-handling obligations.

Private-cloud remains an option for global systemically important banks with bespoke encryption and sovereignty mandates, although capital and staffing requirements curb its wider appeal. Hybrid strategies support phased migration: institutions can retire aging PBXs site by site, funneling traffic via session-border controllers to a cloud core. Continuous-integration pipelines then deliver feature drops such as noise suppression or auto-redaction without downtime. Given rising environmental, social and governance commitments, workload elasticity also lowers idle energy use, helping banks hit carbon-cut targets.

Global Unified Communication-As-A-Service (UCaaS) in Banking Market is Segmented by Component (Telephony, Unified Messaging, Contact Center, Collaboration Platform, and More), Deployment Model (Public Cloud, Hybrid Cloud, and Private Cloud), Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), Banking Application (Retail Banking, Corporate and Wholesale Banking, and More), and Geography.

Geography Analysis

North America retained 36.7% UCaaS in banking market share in 2024, capitalizing on mature cloud regulations and sizeable budgets for enterprise modernization. Barclays, UBS and Citigroup exemplify large-scale deployments that marry collaboration suites with AI copilots to streamline advisor workflows . Despite headway, many regional banks remain tethered to depreciating PBXs, as less than 40% of businesses have completed migration. Hybrid rollouts therefore dominate, balancing transformation momentum with risk-management caution.

Asia-Pacific leads growth at 14.80% CAGR through 2030 as mobile-first demographics spur digital banks to embed voice and messaging directly in apps. Japanese carriers such as NTT and SoftBank export UCaaS footprints globally, while partnerships between Vonage and local integrators digitize contact-center estates throughout Southeast Asia. Conversational-AI adoption rises in concert, lifting first-contact resolution and enabling 24/7 multilingual servicing.

Europe emphasizes data-sovereignty, prompting banks to prefer region-locked clouds or sovereign partnerships. UniCredit's USD 400 million acquisition of Vodeno delivers a cloud-native platform with built-in smart-contract engines, aligning with PSD2 open-banking requisites while expanding white-label capabilities. In the Middle East and Africa, cloud adoption leapfrogs legacy PBX phases; for instance, Ecobank's alliance with Google Cloud powers analytics-driven inclusion programs across 35 nations. These markets underline UCaaS' role in bridging service gaps where physical branches remain sparse.

- Microsoft Corporation

- Cisco Systems, Inc.

- RingCentral, Inc.

- 8x8, Inc.

- Zoom Video Communications, Inc.

- Avaya LLC

- Fuze, Inc.

- West Technology Group, LLC (formerly West UC)

- VOSS Solutions

- NetFortris, Inc.

- TetraVX (Netrix, LLC)

- Kurmi Software SAS

- Vonage Holdings Corp.

- Dialpad, Inc.

- Mitel Networks Corporation

- Revation Systems, Inc.

- NICE Ltd.

- Genesys Telecommunications Labs, Inc.

- Google LLC

- Amazon Web Services, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 BYOD and workforce mobility

- 4.2.2 Need for enterprise-wide UC integration

- 4.2.3 Digital-only banking expansion

- 4.2.4 AI-enabled UCaaS for compliance monitoring

- 4.2.5 5G private branch networks

- 4.2.6 Embedded CPaaS in banking apps

- 4.3 Market Restraints

- 4.3.1 Low cloud-UC awareness in tier-2/3 banks

- 4.3.2 Stringent data-security and residency mandates

- 4.3.3 Legacy on-prem PBX lock-ins

- 4.3.4 Vendor API lock-in risk

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Telephony

- 5.1.2 Unified Messaging

- 5.1.3 Contact Center

- 5.1.4 Collaboration Platform

- 5.1.5 Video Conferencing

- 5.1.6 Communication-Platform APIs

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Banking Application

- 5.4.1 Retail Banking

- 5.4.2 Corporate and Wholesale Banking

- 5.4.3 Investment Banking

- 5.4.4 Payment and FinTech Subsidiaries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 RingCentral, Inc.

- 6.4.4 8x8, Inc.

- 6.4.5 Zoom Video Communications, Inc.

- 6.4.6 Avaya LLC

- 6.4.7 Fuze, Inc.

- 6.4.8 West Technology Group, LLC (formerly West UC)

- 6.4.9 VOSS Solutions

- 6.4.10 NetFortris, Inc.

- 6.4.11 TetraVX (Netrix, LLC)

- 6.4.12 Kurmi Software SAS

- 6.4.13 Vonage Holdings Corp.

- 6.4.14 Dialpad, Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Revation Systems, Inc.

- 6.4.17 NICE Ltd.

- 6.4.18 Genesys Telecommunications Labs, Inc.

- 6.4.19 Google LLC

- 6.4.20 Amazon Web Services, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment