PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844636

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844636

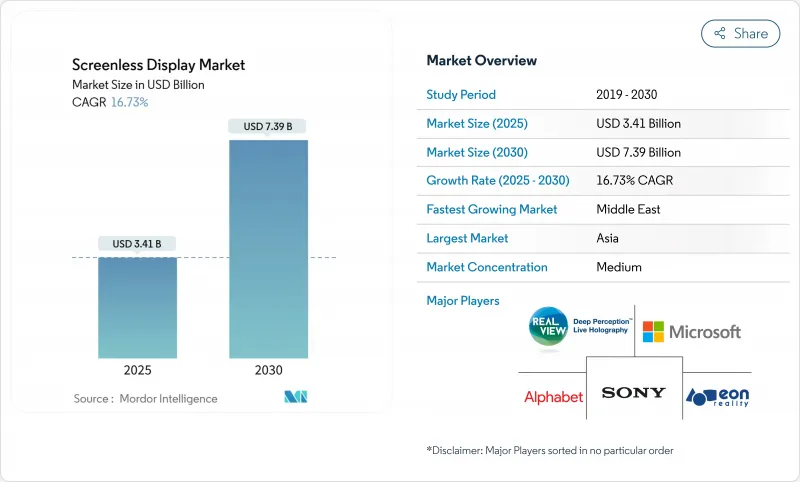

Screenless Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The screenless display market reached USD 3.41 billion in 2025 and is on track to expand at a 16.73% CAGR to USD 7.39 billion by 2030.

Near-term growth stems from maturing mini-LED and µLED supply chains, early regulatory clarity around retinal prosthetics, and automotive demand for augmented-reality (AR) windshields. Over the medium term, neural-interface breakthroughs, sovereign digital-transformation programs in Asia and the Middle East, and falling optical-component costs widen commercial use cases. Military procurement, notably the U.S. Army's IVAS 1.2 order, underpins volume ramps that help drive scale benefits into civilian markets. Meanwhile, persistent supply constraints in waveguide-grade glass and photonic-safety limits on high-nits retinal projection temper the growth curve but do not derail the long-range trajectory of the screenless display market.

Global Screenless Display Market Trends and Insights

Rapid mini-LED and µLED adoption enabling brighter holographic projection

Holographic systems now achieve brightness above 10^7 nits, overcoming ambient-light washout that once constrained outdoor use. Pixel densities nearing 3,400 ppi allow high-resolution imagery, and sidewall passivation paired with CMOS back-planes lowers cost per lumen. The result is heightened interest from automotive, defense, and retail sectors that require sunlight-readable images.

Automotive ADAS shift toward AR windshields

European and Asian regulations incentivize embedding lane-level guidance, hazard alerts, and speed cues directly onto windshields, reducing driver refocus time from multiple seconds to sub-500 ms. Chinese AR-HUD suppliers eliminated wedge films, cutting optical losses by 30%, while EU OEMs integrate lidar data to contextualize overlays for Level 3 autonomy.

Photonic safety limits for high-nits retinal projection

Laser-scanned retinal displays must meet FDA 21 CFR 1040 exposure caps, curbing peak luminance in bright sun settings . EU CE marking imposes parallel constraints, extending validation loops and adding certification cost layers for manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Retina-to-chip interfaces for neuro-visual prosthetics

- Military demand for low-SWaP head-up displays

- Limited supply of waveguide-grade glass (Corning/Schott oligopoly)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synaptic/direct-neural interfaces are slated to climb at a 19.4% CAGR through 2030, although visual image displays retained 60.9% of the screenless display market in 2024. The screenless display market size for visual image-based solutions amounted to 60.9% of total revenue in 2024. Neural systems benefit from military R&D spillovers and rising venture investment in cortical prosthetics. Visual image platforms maintain dominance through cost-effective HUD architectures widely used in automotive and aviation.

Complementary approaches such as retinal laser projection address patients unwilling or unable to undergo invasive neural surgery. Advances in nanoparticle photostimulation reduce surgical risk and may bridge today's gap between non-invasive and implantable modalities. As reimbursement codes for neuro-visual devices firm up, unit economics become more favorable, further catalyzing neural segment momentum.

Implantable and wearable micro-projectors will outpace all other form factors at a 20.2% CAGR to 2030 despite head-up displays' 47.5% revenue lead in 2024. The head-up display segment captured 47.5% of screenless display market share in 2024 on the back of entrenched use in premium vehicles and fighter cockpits. The 256-pixel wireless subretinal implant validates that resolution adequate for letter recognition is now technically feasible, laying a path toward commodity-scale manufacturing later in the decade.

Head-mounted displays continue benefiting from the consumer VR cycle, yet app-ecosystem fatigue dampens unit sell-through. Quasicrystal metasurfaces under development for holographic kiosks expand advertising use cases but remain several cost-downs away from mass deployment. Over the forecast horizon, healthcare and defense procurement will shape demand for body-integrated solutions that offer hands-free situational data without external optics.

The Screenless Display Market Report is Segmented by Technology (Visual Image Displays, Retinal Projection Displays, and More), Display Type (Head-Up Display (HUD), Head-Mounted Display (HMD), Holographic Projection Kiosks, and More), Component (Hardware, Software and Firmware, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 34.7% of 2024 revenue as Chinese OEMs raced to embed AR-HUDs in new-energy vehicles and Japanese optics firms supplied global integrators. Government grants funneled via China's "Intelligent Connected Vehicle" roadmap subsidize early-stage suppliers, while Japan's precision-glass makers refine high-index melts that feed the wider supply chain. South Korea's display fabs invest in mirrorless windshield projection modules that shrink z-height and cost, positioning the peninsula as a future component hub.

North America sustains leadership in neural-interface IP and defense volume programs. The screenless display market size for military and security applications will swell once IVAS shifts from low-rate initial production to full-rate production post-2026. Silicon Valley continues to attract venture funds for multimodal XR platforms, and cross-border auto production in Mexico supports regional HUD assembly.

The Middle East grows at 19.1% CAGR, catalyzed by Vision 2030 diversification funds channeled into smart-city pilots. Gulf airlines explore holographic way-finding kiosks to improve airport throughput, and sovereign-wealth funds back local glass-fab start-ups aimed at challenging the Corning/Schott oligopoly. Europe maintains a cohesive regulatory stance that mandates ADAS integration, ensuring AR windshields gain traction first in German and French premium models before cascading to mid-tier vehicles.

- Alphabet Inc. (Google)

- Microsoft Corp.

- Sony Group Corp.

- Samsung Electronics Co. Ltd.

- Magic Leap Inc.

- Avegant Corp.

- RealView Imaging Ltd.

- Synaptics Inc.

- Holoxica Ltd.

- EON Reality Inc.

- Leia Inc.

- Vuzix Corp.

- MicroVision Inc.

- DigiLens Inc.

- Dispelix Oy

- Lumus Ltd.

- Panasonic Corp.

- Apple Inc.

- Jade Bird Display

- WaveOptics Ltd.

- Mojo Vision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Mini-LED and µLED Adoption Enabling Brighter Holographic Projection

- 4.2.2 Automotive ADAS Shift Toward AR Windshields in Europe and Asia

- 4.2.3 Retina-to-Chip Interfaces for Neuro-Visual Prosthetics (United States and Israel)

- 4.2.4 Military Demand for Low-SWaP Head-Up Displays (NATO Programs)

- 4.2.5 Smartphone OEM Push for "Ambient Mode" Screenless Notifications

- 4.2.6 Multimodal XR Platforms Opening Developer Ecosystems (US-Centric)

- 4.3 Market Restraints

- 4.3.1 Photonic Safety Limits for High-Nits Retinal Projection

- 4.3.2 Limited Supply of Waveguide-Grade Glass (Corning/Schott Oligopoly)

- 4.3.3 GPU Thermal Budget in Wearables Constraining Battery Life

- 4.3.4 Regulatory Lag on Class-II Implantable Displays (FDA/EMA)

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 Visual Image Displays

- 5.1.2 Retinal Projection Displays

- 5.1.3 Synaptic/Direct-Neural Interface

- 5.2 By Display Type

- 5.2.1 Head-Up Display (HUD)

- 5.2.2 Head-Mounted Display (HMD)

- 5.2.3 Holographic Projection Kiosks

- 5.2.4 Implantable and Wearable Micro-Projectors

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.1.1 Light Engine and Lasers

- 5.3.1.2 Waveguides and Optical Combiners

- 5.3.1.3 ICs and Controllers

- 5.3.2 Software and Firmware

- 5.3.3 Services (Design, Integration, Maintenance)

- 5.3.1 Hardware

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Aerospace and Defense

- 5.4.4 Healthcare and Life-Sciences

- 5.4.5 Industrial and Logistics

- 5.4.6 Retail and Advertisement

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alphabet Inc. (Google)

- 6.4.2 Microsoft Corp.

- 6.4.3 Sony Group Corp.

- 6.4.4 Samsung Electronics Co. Ltd.

- 6.4.5 Magic Leap Inc.

- 6.4.6 Avegant Corp.

- 6.4.7 RealView Imaging Ltd.

- 6.4.8 Synaptics Inc.

- 6.4.9 Holoxica Ltd.

- 6.4.10 EON Reality Inc.

- 6.4.11 Leia Inc.

- 6.4.12 Vuzix Corp.

- 6.4.13 MicroVision Inc.

- 6.4.14 DigiLens Inc.

- 6.4.15 Dispelix Oy

- 6.4.16 Lumus Ltd.

- 6.4.17 Panasonic Corp.

- 6.4.18 Apple Inc.

- 6.4.19 Jade Bird Display

- 6.4.20 WaveOptics Ltd.

- 6.4.21 Mojo Vision

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment