PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844672

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844672

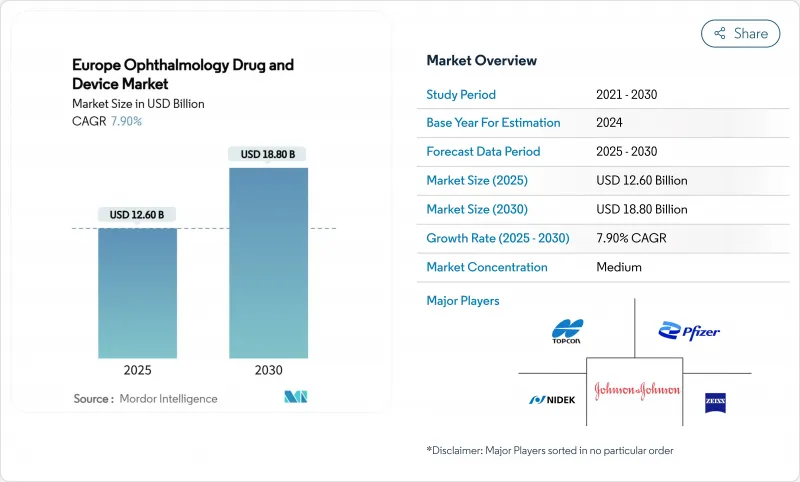

Europe Ophthalmology Drug And Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe ophthalmic devices and drugs market reached USD 12.6 billion in 2025 and is expected to climb to USD 18.8 billion by 2030, advancing at a 7.9% CAGR.

Demographic aging, rising incidence of chronic eye conditions, and steady migration toward minimally invasive surgery sustain this expansion. Hospitals continue to dominate procedure volumes, yet outpatient facilities are capturing the incremental growth as payers encourage cost-efficient care models. AI-enabled diagnostic platforms are improving screening throughput in Germany and the UK, while regulatory actions such as the EMA's 2024 Durysta withdrawal are redirecting R&D toward safer sustained-release implants. Consolidation among leading manufacturers and new vertical integration moves by EssilorLuxottica underscore the sector's shift toward end-to-end eye-care ecosystems.

Europe Ophthalmology Drug And Device Market Trends and Insights

Growing Prevalence of Chronic Eye Diseases

The incidence of age-related macular degeneration and diabetic retinopathy is climbing as Europe's population ages, generating a durable demand base for both surgical and pharmaceutical interventions. Health systems are embedding ophthalmic screening into routine primary care, and German pilots using AI achieved 100% sensitivity for diabetic-retinopathy detection, catalyzing wider adoption. The economic burden of retinal disorders is estimated to hit EUR 99.8 billion by 2030, bolstering procurement budgets for advanced diagnostic equipment and sustained-release injectables.

Expanding Geriatric Population Base

Individuals aged 65 years or older constitute Europe's fastest-growing cohort and exhibit the highest prevalence of cataract, glaucoma, and AMD. National services are tackling surgical backlogs by contracting private providers, a model that raised UK cataract procedure volumes 40% over pre-pandemic levels. A larger elderly population simultaneously fuels premium IOL demand, reflecting patient preference for spectacle independence and rapid visual recovery.

High Cost and Reimbursement Gaps for Premium Lenses/MIGS

Cataract surgery tariff disparities range from EUR 432.5 (USD 507.1) in Poland to EUR 3,411.96 (USD 4,001.21) in Portugal, causing uneven patient access to premium IOLs. Co-payment requirements depress uptake in social-insurance markets, while MIGS reimbursement remains procedure-specific, creating friction for innovators and clinicians alike. Germany's 2025 abolition of fixed prices for visual aids illustrates the fluid reimbursement landscape.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Minimally Invasive Glaucoma Surgery

- AI-Enabled Diagnostic Imaging & Remote Screening Rollout

- Stringent EU MDR Compliance Burden on SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical devices generated 46.7% of total 2024 revenue within the Europe ophthalmic devices and drugs market and continue to command premium pricing due to constant innovation. Alcon holds about 60% global share in presbyopia-correcting IOLs and has replicated similar penetration across major EU economies. Phaco platforms and femtosecond lasers secure attractive service contracts, while the fastest-expanding sub-segment is MIGS. The segment's value proposition rises as bundled cataract-plus-MIGS procedures reduce overall care episodes.

Meanwhile, new hydrogel implants and refillable ocular reservoirs target adherence gaps. Vision-care devices retain stable revenue streams via contact-lens material upgrades and blue-light-filter spectacles. Alcon's 2025 Clareon PanOptix Pro IOL, boasting 94% light utilization, exemplifies engineering efforts that sustain price premiums. Across all modalities, companies intensify R&D to capture an ageing demographic seeking spectacle independence and rapid recovery.

The Europe Ophthalmic Devices and Drugs Market Report is Segmented by Product (Devices, Drugs), Disease (Glaucoma, Cataract, Age-Related Macular Degeneration, Diabetic Retinopathy, and More), End User (Hospitals, Specialty Clinics & ASCs, Retail Pharmacies & Optical Stores, Online Pharmacies), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcon

- Carl Zeiss

- Johnson & Johnson

- Bausch + Lomb Corp.

- EssilorLuxottica

- Novartis AG (incl. Sandoz & Sandoz Vision Care)

- Roche

- Pfizer

- Glaukos Corp.

- Santen Pharmaceuticals

- Staar Surgical Co.

- Topcon Corp.

- Nidek

- HAAG-Streit

- Ziemer Group

- Canon

- Hoya Corp. / Pentax Medical

- CooperVision Inc.

- Danaher

- Abbvie

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence Of Chronic Eye Diseases

- 4.2.2 Expanding Geriatric Population Base

- 4.2.3 Rapid Adoption Of Minimally-Invasive Glaucoma Surgery (MIGS)

- 4.2.4 AI-Enabled Diagnostic Imaging & Remote Screening Rollout

- 4.2.5 Surge In Sustained-Release Ocular Drug-Delivery Approvals

- 4.2.6 EU Funding Programs For Ophthalmic R&D And Start-Ups

- 4.3 Market Restraints

- 4.3.1 High Cost & Reimbursement Gaps For Premium Lenses/MIGS

- 4.3.2 Stringent EU MDR Compliance Burden On SMEs

- 4.3.3 Sub-Optimal Patient Adherence To Multi-Dose Eyedrop Regimens

- 4.3.4 Supply-Chain-Driven API Shortages For Sterile Ophthalmic Drugs

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Devices

- 5.1.1.1 Surgical Devices

- 5.1.1.1.1 Intra-ocular Lenses

- 5.1.1.1.2 Ophthalmic Lasers

- 5.1.1.1.3 Phacoemulsification Systems

- 5.1.1.1.4 Other Surgical Devices

- 5.1.1.2 Diagnostic Devices

- 5.1.1.2.1 Optical Coherence Tomography Scanners

- 5.1.1.2.2 Fundus Cameras

- 5.1.1.2.3 Tonometers

- 5.1.1.2.4 Other Diagnostic Devices

- 5.1.1.3 Vision Care Devices

- 5.1.1.3.1 Contact Lenses

- 5.1.1.3.2 Spectacle Lenses

- 5.1.2 Drugs

- 5.1.2.1 Glaucoma Drugs

- 5.1.2.2 Retinal Disorder Drugs

- 5.1.2.3 Dry-Eye Therapies

- 5.1.2.4 Anti-Allergy / Anti-Inflammatory Drugs

- 5.1.2.5 Anti-Infective Drugs

- 5.1.2.6 Other Drugs

- 5.1.1 Devices

- 5.2 By Disease

- 5.2.1 Glaucoma

- 5.2.2 Cataract

- 5.2.3 Age-related Macular Degeneration

- 5.2.4 Diabetic Retinopathy

- 5.2.5 Inflammatory Diseases

- 5.2.6 Refractive Disorders

- 5.2.7 Other Diseases

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics & ASCs

- 5.3.3 Retail Pharmacies & Optical Stores

- 5.3.4 Online Pharmacies

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Alcon AG

- 6.3.2 Carl Zeiss Meditec AG

- 6.3.3 Johnson & Johnson Vision

- 6.3.4 Bausch + Lomb Corp.

- 6.3.5 EssilorLuxottica SA

- 6.3.6 Novartis AG (incl. Sandoz & Sandoz Vision Care)

- 6.3.7 Roche Holding AG

- 6.3.8 Pfizer Inc.

- 6.3.9 Glaukos Corp.

- 6.3.10 Santen Pharmaceutical Co. Ltd

- 6.3.11 Staar Surgical Co.

- 6.3.12 Topcon Corp.

- 6.3.13 Nidek Co. Ltd

- 6.3.14 Haag-Streit Group

- 6.3.15 Ziemer Group AG

- 6.3.16 Canon Medical Systems Corp.

- 6.3.17 Hoya Corp. / Pentax Medical

- 6.3.18 CooperVision Inc.

- 6.3.19 Leica Microsystems GmbH

- 6.3.20 Allergan (AbbVie)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment