PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844692

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844692

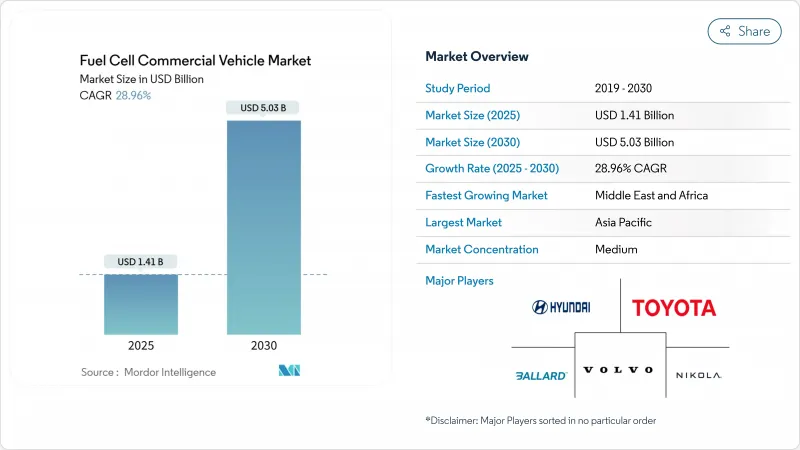

Fuel Cell Commercial Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The hydrogen fuel cell commercial vehicle market is valued at USD 1.41 billion in 2025 and is projected to reach USD 5.03 billion by 2030, translating into a 28.96% CAGR.

A tight regulatory climate, the rapid fall in renewable-based hydrogen costs, and a widening corporate net-zero freight commitments push sales volumes higher yearly. Technology gains notably a fuel-cell system cost target of USD 80/kW by 2025, helping large fleets cross total-cost-of-ownership thresholds on routes over 400 km. Regional hydrogen corridors anchored around Rotterdam and Los Angeles remove early-stage infrastructure anxiety while port authorities set firm zero-emission freight targets. These forces encourage OEMs to scale production, lower per-unit costs, and launch commercial models for long-haul logistics, not just urban buses.

Global Fuel Cell Commercial Vehicle Market Trends and Insights

Stringent Emission Regulations for Commercial Vehicles

The EU "Fit-for-55" package requires a 90% emissions cut from heavy-duty vehicles by 2040, with interim targets of 45% by 2030 and 65% by 2035. To curb emissions from the transportation sector, revised CO2 standards now encompass a broader spectrum of heavy-duty vehicles (HDVs). The updated regulations now include buses, coaches, trailers, and vocational trucks, collectively accounting for over 90% of HDV sales. OEMs are accelerating fuel-cell programs to meet the tougher standards, particularly for long-haul operations where battery mass and charging downtime remain challenging.

Zero-Emission Mandates for Urban Bus Fleets in North America

California's Innovative Clean Transit Regulation compels transit operators to transition to 100% zero-emission fleets by 2040. Purchases must already be 25% zero-emission, reaching 50% by 2026. Federal grants of USD 1.5 billion in 2024 funded roughly 600 additional buses, and full-size fuel-cell electric bus deployments grew 55% year-over-year. Agencies prefer fuel-cell platforms for blocks above 250 km, requiring dual battery packs if executed with pure BEVs, compromising seating capacity. Operators also report that ambient-temperature-insensitive refuelling simplifies service planning in cold northern climates.

Fuel-Cell Durability Concerns in Heavy-Duty Cycles

Despite recent technological advances, fuel cell systems for heavy-duty applications still grapple with significant durability concerns. Heavy trucks require systems capable of at least 25,000 operating hours. The Million Mile Fuel Cell Truck Consortium targets 30,000 hours by 2030. UCLA's 2025 breakthrough of more than 200,000 hours in lab tests addresses lifetime anxiety but is still moving toward scaled commercial validation. These technologies have yet to be widely commercialized and integrated into production vehicles.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Freight Alliances Accelerating OEM Purchase Commitments

- Port-Centric Hydrogen Corridors Spurring Early Adoption

- Competition from Battery-Electric Trucks in Short-Haul

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Buses held 45.76% of the hydrogen fuel cell commercial vehicle market share in 2024 as transit agencies tapped dedicated funding lines to replace aging diesel fleets. Solaris captured 65% of European fuel-cell bus registrations, reflecting OEM specialization in depot-based operations. Orders such as Orange County Transportation Authority's 40 FCEBs underscore the segment's traction. Momentum benefits from predictable routes and return-to-depot refueling, traits that fit 350-bar compressed-gas systems and simplify daily operations for maintenance teams. Procurement frameworks that bundle vehicles with fueling contracts further improve budget certainty for public-sector buyers.

Trucks are forecast to outpace buses with a 31.10% CAGR from 2025 to 2030, moving the hydrogen fuel cell commercial vehicle market toward freight logistics. Nikola's 500-mile TRE FCEV and Hyundai's XCIENT class-8 platform are positioned for hub-to-hub logistics, exploiting 20-minute refueling and higher payload headroom over BEVs. Corporate freight alliances provide offtake guarantees that help banks underwrite new refueling stations. As green hydrogen supply stabilizes, total-cost parity on 400-600 km lanes is expected to unlock nationwide rollouts across Nordic and Central European freight corridors.

PEMFC technology commanded 81.25% of the hydrogen fuel cell commercial vehicle market in 2024, valued for its rapid start-up and tolerance to frequent load changes. Platinum loading per stack continues to fall, closing cost gaps while meeting city-bus duty cycles. Fleet trials in California show PEMFC buses exceeding 20,000 hours with degradation under 10%, reinforcing operator confidence in multi-shift service.

Solid Oxide Fuel Cell (SOFC) is expected to grow at a 31.25% CAGR through 2030. Electrical efficiency up to 60%, combined with tolerance for lower-purity hydrogen, supports long-haul and auxiliary-power integration scenarios. Material science progress has trimmed operating temperatures to 700 °C, allowing quicker heat-up and smaller thermal-management components. Reduced reliance on platinum-group metals promises lower stack costs at scale, setting the stage for expanded adoption once durability reaches 30,000 hours.

The Fuel Cell Commercial Vehicle Market Report is Segmented by Vehicle Type(Buses and More), Fuel Cell (Proton Exchange Membrane Fuel Cell and More), Power Range (Below 100 KW and More), Driving Range (Below 400km and More), End-Use (Public Transit Fleets and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific region led the hydrogen fuel cell commercial vehicle market with a 41.62% share in 2024, underpinned by China's 125,000 tpa green-hydrogen capacity and large-scale component manufacturing. Cost advantages in electrolyser production and domestic procurement quotas have built a localised value chain spanning stacks, power electronics, and tanks. Japan and South Korea reinforce the region's edge with long-running R&D programs and early OEM production lines.

Europe follows closely, driven by binding CO2 cuts that require 45% lower heavy-duty emissions by 2030 and 90% by 2040. Refueling coverage reached 187 stations by May 2024, and fuel-cell bus registrations rose 82% during the same period. Cross-border projects, such as the H2Accelerate collaboration, aim to link Scandinavia to Northern Italy with 150 stations by 2030.

North America benefits from a blend of federal incentives and state mandates. California's ARCHES hub, backed by USD 1.2 billion, targets 45,000 tons/day of hydrogen by 2045. The U.S. Department of Energy wants 30% of new medium- and heavy-duty sales to be zero-emission by 2030, propelling truck OEM pilot fleets across the Pacific Northwest, the Gulf Coast, and the Great Lakes.

The Middle East and Africa region is expected to be the forecast to grow at 29.05% CAGR to 2030, is building on abundant solar and wind resources plus existing gas pipeline networks. Saudi Arabia and the UAE are constructing pilot truck corridors linking ports with inland distribution centers, aiming to decarbonize a freight sector that accounts for a quarter of regional emissions.

- Hyundai Motor Company

- Toyota Motor Corporation

- Ballard Power Systems

- Volvo Group (cellcentric JV)

- Nikola Corporation

- PACCAR Inc.

- Mercedes-Benz Group AG

- Honda Motor Co.

- SAIC Motor Corporation

- Foton Motor Group

- Tata Motors Limited

- Solaris Bus & Coach sp. z o.o.

- Plug Power Inc.

- Hyzon Motors Inc.

- Cummins Inc.

- Wrightbus Ltd.

- Zhejiang Geely Holding Group

- Dongfeng Motor Corporation

- Xiamen King Long Motor Group

- Gaussin S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Emission Regulations for Commercial Vehicles

- 4.2.2 Zero-Emission Mandates for Urban Bus Fleets in North America

- 4.2.3 Hydrogen Production Cost Declines from Renewable Electrolysis in China

- 4.2.4 Corporate Net-Zero Freight Alliances Accelerating OEM Purchase Commitments

- 4.2.5 TCO Parity for Long-Haul Trucks Above 400 km in Nordics

- 4.2.6 Port-Centric Hydrogen Corridors Spurring Early Adoption

- 4.3 Market Restraints

- 4.3.1 High Infrastructure Costs for Hydrogen Refuelling Stations

- 4.3.2 Slow Roll-out of Green Hydrogen Supply in Emerging Markets

- 4.3.3 Fuel-Cell Durability Concerns in Heavy-Duty Cycles

- 4.3.4 Competition from Battery-Electric Trucks in Short-Haul

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers / Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Buses

- 5.1.2 Trucks

- 5.1.3 Vans

- 5.1.4 Other Vehicle Types (Pickup Trucks, etc.)

- 5.2 By Fuel Cell Type

- 5.2.1 Proton Exchange Membrane Fuel Cell (PEMFC)

- 5.2.2 Phosphoric Acid Fuel Cell (PAFC)

- 5.2.3 Solid Oxide Fuel Cell (SOFC)

- 5.2.4 Others

- 5.3 By Power Range

- 5.3.1 Below 100 kW

- 5.3.2 100 kW - 200 kW

- 5.3.3 Above 200 kW

- 5.4 By Driving Range

- 5.4.1 Below 400 km

- 5.4.2 400 km - 600 km

- 5.4.3 Above 600 km

- 5.5 By End-User

- 5.5.1 Public Transit Fleets

- 5.5.2 Long-Haul Freight & Logistics

- 5.5.3 Last-Mile Delivery

- 5.5.4 Municipal & Utility Services

- 5.5.5 Other Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 South Africa

- 5.6.5.3 Saudi Arabia

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Hyundai Motor Company

- 6.4.2 Toyota Motor Corporation

- 6.4.3 Ballard Power Systems

- 6.4.4 Volvo Group (cellcentric JV)

- 6.4.5 Nikola Corporation

- 6.4.6 PACCAR Inc.

- 6.4.7 Mercedes-Benz Group AG

- 6.4.8 Honda Motor Co.

- 6.4.9 SAIC Motor Corporation

- 6.4.10 Foton Motor Group

- 6.4.11 Tata Motors Limited

- 6.4.12 Solaris Bus & Coach sp. z o.o.

- 6.4.13 Plug Power Inc.

- 6.4.14 Hyzon Motors Inc.

- 6.4.15 Cummins Inc.

- 6.4.16 Wrightbus Ltd.

- 6.4.17 Zhejiang Geely Holding Group

- 6.4.18 Dongfeng Motor Corporation

- 6.4.19 Xiamen King Long Motor Group

- 6.4.20 Gaussin S.A.

7 Market Opportunities & Future Outlook