PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844697

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844697

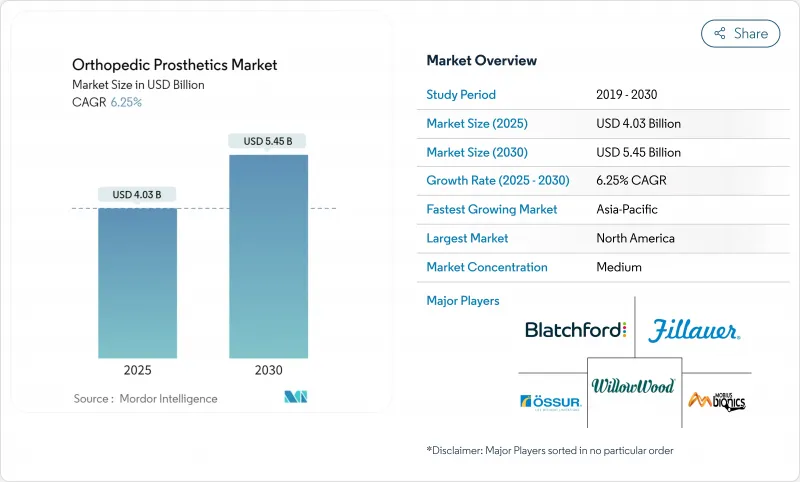

Orthopedic Prosthetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The orthopedic prosthetics market size stood at USD 1.82 billion in 2025 and is forecast to reach USD 2.79 billion by 2030, advancing at an 8.9% CAGR.

Continuous growth is supported by rising diabetes-linked amputations, breakthrough neural-interface limbs, and widening access to lower-cost 3-D printing capabilities that shorten production cycles and improve customization. Demographic aging, coupled with osteoarthritis prevalence, enlarges the addressable user base, while defense-veteran rehabilitation programs in Asia-Pacific accelerate technology diffusion across emerging economies. Competitive differentiation now pivots on real-time sensory feedback, carbon-fiber alternatives, and cybersecurity readiness for connected devices, creating a dynamic landscape in which incumbents and start-ups pursue vertical integration and niche specialization. Tight reimbursement environments and titanium supply shortages temper near-term margins but also motivate manufacturers to streamline supply chains and localize additive manufacturing hubs.

Global Orthopedic Prosthetics Market Trends and Insights

Rising Diabetes-Linked Amputations Drive Market Expansion

More than 1 million diabetes-related lower-limb amputations occur yearly, sharply lifting demand for sophisticated socket designs that reduce shear forces and improve infection control for fragile skin surfaces. Specialized foot-care pathways in the United States, China, and India now funnel patients toward earlier prosthetic intervention, bringing forward replacement cycles and expanding recurring component sales. Manufacturers responding to this volume uptick are investing in lighter carbon-composite pylons that accommodate neuropathic gait patterns and reduce energy expenditure. The phenomenon is particularly acute in urban Asia-Pacific where rapid lifestyle changes drive higher diabetes prevalence, aligning regional market expansion with public-health priorities and donor-funded limb-loss initiatives.

Ageing Population Amplifies Osteoarthritis-Related Demand

Median ages are climbing above 40 years in Northern Europe, Japan, and Australia, widening the pool of seniors requiring joint replacements and, in revision scenarios, partial limb prostheses. Baby-boomer cohorts differ from earlier generations by insisting on high-activity prosthetic knees that support golfing, hiking, and light-jogging. Consequently, design priorities have shifted toward adaptive damping microprocessor units that modulate swing phase in real time. Payers increasingly reimburse for such higher-end devices when linked to fall-reduction evidence, reinforcing the upgrade cycle for elderly athletes. Hospitals have introduced geriatric-orthopedics programs integrating bone-density screening with prosthetic selection, further supporting sustained device turnover.

Reimbursement Inconsistencies Constrain Market Access

Medicare beneficiaries in the United States still pay USD 3,580 out-of-pocket per limb despite insurance, a barrier prompting device abandonment that reduces replacement cycles and aftermarket sales. France's 25% reimbursement cut in 2025 led to supplier exits and sporadic implant shortages, underscoring how policy swings reshape supply availability. Start-ups counteract margin pressure by leasing rather than selling microprocessor knees, bundling software updates and maintenance into subscription plans aligned with payer budget cycles.

Other drivers and restraints analyzed in the detailed report include:

- Microprocessor and Myoelectric Technology Breakthrough

- 3-D Printing Democratizes Access in Emerging Markets

- Workforce Shortages Limit Service Delivery Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lower-extremity solutions represented 55.75% of the orthopedic prosthetics market size in 2024, anchored by high-incidence transtibial and transfemoral procedures. Demand concentration creates scale economies that manufacturers leverage to fund R&D for next-generation rotary adapters that tolerate higher torsional loads during sports. Liners, while a smaller revenue pool, deliver 9.67% CAGR through 2030 by addressing skin-sweat management and residual-limb volume fluctuation, two factors strongly correlated with device abandonment. New thermoplastic elastomer gels infused with antimicrobial nanoparticles extend liner replacement intervals, generating recurring sales with minimal clinical oversight. Specialty-sports prosthetics, though niche, attract premium pricing and act as branding showcases that inspire mainstream upper-limb upgrades. The orthopedic prosthetics market share for sockets climbs gradually as custom 3-D printed lattices displace hand-laminated fiberglass shells, reducing weight by 30% and improving airflow for marathon runners.

The Orthopedic Prosthetics Market Report is Segmented by Product Type (Upper Extremity Prosthetics, Lower Extremity Prosthetics, Liners, Sockets, Modular Components, Specialty & Sports Prosthetics), Technology (Conventional, Electric Powered/Myoelectric, and More), End-User (Hospitals, Prosthetic Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.23% regional revenue share in 2024, powered by insurance coverage that reimburses high-end microprocessor knees and arms, as well as dense networks of certified practitioners. The United States drives regional innovation, hosting landmark AMI and OMP research that secures technology-leadership halo effects across the orthopedic prosthetics market. Canada leverages cross-provincial tele-orthotics platforms to extend access to northern communities, whereas Mexico integrates maquiladora clusters to co-manufacture lightweight pylons for export.

Asia-Pacific, forecast to rise at a 10.93% CAGR, combines outsized diabetes prevalence with ambitious universal-health coverage rollouts. China's local innovators accelerate low-cost 3-D printed sockets that undercut imports by 35%. India's public procurement of modular feet for district-level trauma centers further lifts volume. Japan and South Korea push the frontier in sensory feedback, driving regional demand for advanced firmware upgrades. Australia, despite practitioner scarcity, maintains high adoption of AI-guided alignment tools that compensate for workforce gaps. Regional humanitarian projects, such as remote prosthetic aid in conflict zones, illustrate cross-border dissemination of design files over satellite networks.

Europe presents a mature, regulation-intensive environment where price caps squeeze margins yet clinical practice standards remain rigorous. Germany pioneers carbon-fiber recycling initiatives to mitigate material scarcity, while the United Kingdom fast-tracks digital orthopedics pilots under the NHS Long-Term Plan. France's reimbursement cuts create localized shortages, prompting parallel-import channels and sparking debate on sustainable pricing. South America, Middle East, and Africa collectively account for modest share today yet post high single-digit growth as 3-D printing hubs emerge in Brazil and the UAE, gradually reducing lead times for culturally attuned cosmetic covers and shock-absorbing feet.

- Ossur

- Ottobock

- Zimmer Biomet

- Stryker

- Smiths Group

- DePuy Synthes (J&J)

- Medtronic

- Enovis (DJO)

- Blatchford

- WillowWood

- Freedom Innovations

- Touch Bionics

- Steeper Group

- College Park Industries

- Ultraflex Systems

- Fillauer

- SHL Medical

- ReWalk Robotics

- Proteor

- Ability Dynamics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising diabetes-linked amputations

- 4.2.2 Ageing population & osteoarthritis prevalence

- 4.2.3 Advancements in microprocessor & myoelectric limbs

- 4.2.4 Expansion of 3-D printing service hubs in emerging markets

- 4.2.5 Defence-veteran rehab funding surge in Asia-Pacific

- 4.2.6 E-commerce aftermarket component sales growth

- 4.3 Market Restraints

- 4.3.1 High device cost & inconsistent reimbursement

- 4.3.2 Shortage of certified prosthetists in developing nations

- 4.3.3 Titanium & carbon-fibre supply bottlenecks

- 4.3.4 Cyber-security scrutiny of smart prosthetics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Upper Extremity Prosthetics

- 5.1.2 Lower Extremity Prosthetics

- 5.1.3 Liners

- 5.1.4 Sockets

- 5.1.5 Modular Components

- 5.1.6 Specialty & Sports Prosthetics

- 5.2 By Technology

- 5.2.1 Conventional

- 5.2.2 Electric Powered / Myoelectric

- 5.2.3 Hybrid

- 5.2.4 3-D Printed / Additively Manufactured

- 5.2.5 Robotic / Microprocessor Controlled

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Prosthetic Clinics

- 5.3.3 Rehabilitation Centers

- 5.3.4 Ambulatory Surgical Centers

- 5.3.5 Home-care Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Ossur

- 6.3.2 Ottobock

- 6.3.3 Zimmer Biomet

- 6.3.4 Stryker

- 6.3.5 Smith & Nephew

- 6.3.6 DePuy Synthes (J&J)

- 6.3.7 Medtronic

- 6.3.8 Enovis (DJO)

- 6.3.9 Blatchford

- 6.3.10 WillowWood

- 6.3.11 Freedom Innovations

- 6.3.12 Touch Bionics

- 6.3.13 Steeper Group

- 6.3.14 College Park Industries

- 6.3.15 Ultraflex Systems

- 6.3.16 Fillauer

- 6.3.17 SHL Medical

- 6.3.18 ReWalk Robotics

- 6.3.19 Proteor

- 6.3.20 Ability Dynamics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment