PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844724

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844724

Healthcare Fabrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

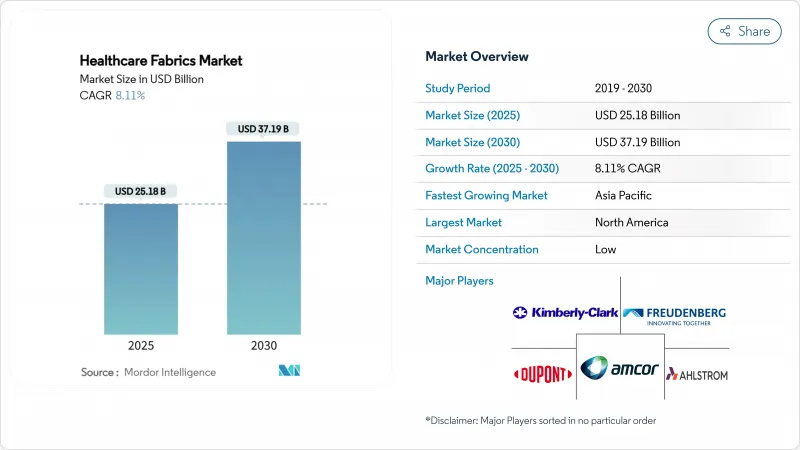

The Healthcare Fabrics Market size is estimated at USD 25.18 Billion in 2025, and is expected to reach USD 37.19 Billion by 2030, at a CAGR of 8.11% during the forecast period (2025-2030).

Rising hospital-acquired-infection (HAI) mitigation mandates, the pivot toward cellulose-based fibers, and the steady integration of sensor-enabled fabrics together widen the addressable base for the healthcare textiles market while helping providers meet infection-control and sustainability goals. Continuous material innovation, ranging from lyocell gauzes with more than 99% solvent recovery to zinc-nanocomposite barrier fabrics, allows manufacturers to offer premium products that combine durability with antimicrobial efficacy. Regulatory trends such as ISO 10993-1 biocompatibility testing in North America and upcoming PFAS restrictions in Europe amplify the need for compliant, high-performance textiles, reinforcing long-term demand. Meanwhile, Asia-Pacific's capacity expansions and national health-insurance rollouts are tilting volume growth toward emerging economies, even as North American buyers remain early adopters of smart monitoring fabrics. Consolidation plays, illustrated by Berry Global's merger that formed Magnera Corporation, underscore the strategic value of scale and vertical integration in a market where certification costs and R&D spending continue to rise.

Global Healthcare Fabrics Market Trends and Insights

Rising Demand in Developing Nations

Fast-growing health-insurance programs are stimulating hospital construction from Jakarta to Johannesburg, lifting annual procurement budgets for antimicrobial drapes, breathable uniforms, and disposable Personal Protective Equipment (PPE). India's technical-textiles sector, valued at USD 19 billion, has used 100% Foreign Direct Investment (FDI) allowances and the National Technical Textiles Mission to boost domestic capacity, slashing import dependence for specialized fibers . Personal Protective Equipment (PPE) scaling during the pandemic proved local suppliers can meet surge requirements, a lesson now informing strategic stockpiling policies. Manufacturers that localize production gain duty benefits and shorter lead times, positioning them to capture the incremental volumes generated by middle-class healthcare utilization. While price sensitivity remains high, tender documents increasingly reference International Organization for Standardization (ISO), American Society for Testing and Materials (ASTM), and European Union Medical Device Regulation (EU MDR) standards, signalling an upgrade path toward higher-margin, certified products.

Increasing Use of Cellulose Fibres in Healthcare

Lyocell and similar regenerated-cellulose fibers are displacing synthetics in wound dressings, patient clothing, and sustainable drapes because they provide hypoallergenic performance, superior moisture management, and a benign end-of-life profile. Solvent recovery rates above 99% in the N-Methylmorpholine N-oxide (NMMO) process lower environmental footprints, satisfying forthcoming European Union (EU)-wide textile eco-design rules. Antimicrobial post-treatments using chitosan derivatives, quaternary ammonium salts, or silver nanoparticles now bond effectively to cellulose matrices without degrading tensile strength. The Lenzing Group's International Sustainability & Carbon Certification (ISCC) PLUS-certified sites in Luxembourg and Richmond generate Lyocell under 100% renewable electricity, offering hospitals Scope 3 emission reductions for procurement scorecards. As Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) bans tighten, cellulose fibers stand out for safe-chemistry compliance and traceable sourcing, reinforcing their long-run growth momentum.

Lack of Consumer Awareness

Procurement managers in lower-income regions often equate textile quality with thread-count rather than antimicrobial durability or sensor accuracy, slowing upgrade cycles. The absence of harmonized smart-textile standards complicates value assessments, while limited case-study dissemination keeps total-cost-of-ownership benefits under-recognized. Industry associations are expanding training modules, but uptake varies widely. Until consistent labelling and performance-tier frameworks emerge, bulk buyers may default to lowest-capex options, curbing near-term penetration of premium fabrics.

Other drivers and restraints analyzed in the detailed report include:

- Hospital-Acquired-Infection Reduction Mandates

- Surge in Smart-Textile Integration for Patient Monitoring

- Volatile Petro-Polymer Raw-Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene sustained a 40.17% revenue lead in 2024 thanks to low resin cost, melt-blown versatility, and hydrophobicity suited for disposable barrier products. Yet the healthcare textiles market is witnessing a pivot as other material types, such as cellulose-based competitors, grow 9.65% annually on the back of bio-compatibility and PFAS-free credentials. Europe's forthcoming PFAS ban effective January 2025 raises compliance hurdles for legacy fluorochemical finishes, nudging buyers toward lyocell and chitosan-treated fabrics. Several United States hospital groups have published sourcing roadmaps that target a 30% procurement mix shift toward bio-based inputs by 2030, creating sizeable headroom for cellulose adoption. Polyester continues to service reusable privacy curtains and high-wash-count scrubs, but energy-recovery upgrades in dyeing plants are helping mitigate its carbon intensity. Niche volumes of polyethylene are preserved for micro-porous laminates offering high moisture-vapour transmission rates in critical-care drapes. Cotton's presence recedes because moisture retention increases pathogen load, prompting its substitution with blends that embed antimicrobial chemistries. Start-up innovations such as enzymatic bleaching and low-temperature reactive dye formulas point to an incremental greening of legacy fibers, but their scalability against cellulose's closed-loop process remains uncertain.

The Healthcare Fabrics Market Report is Segmented by Material (Polypropylene, Polyester, Polyethylene, Cotton, and Other Material Types), Fabric Type (Woven, Non-Woven, and Knitted), Application (Privacy Curtains, Wall Coverings, Hygiene Products, Dressing Products, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America took 38.25% revenue in 2024, underpinned by rigorous Food and Drug Administration (FDA) oversight that mandates ISO-10993-1 testing for skin-contact devices, including antimicrobial drapes and smart textiles. Providers in the United States prioritize infection-control efficacy and therefore adopt premium cellulosic or fluorine-free barrier fabrics despite higher unit prices. Supply-chain resiliency remains a board-level concern; Premier's 2023 survey showed 75% of executives expect disruptions to persist for at least two more years, prompting multi-sourcing strategies and near-shoring initiatives. Cardinal Health's AI-enabled 340,000 sq ft Fort Worth distribution hub exemplifies investment in logistics automation that shortens lead times and increases fill-rate guarantees.

Asia-Pacific is advancing at a 9.41% CAGR through 2030 as governments pour capital into hospital infrastructure and incentivize domestic technical-textile production. India's USD 19 billion technical-textiles base enjoys duty credits and 100% FDI allowances, capturing export orders and substituting imports. China expands its hold on bandage and gauze exports while channeling R&D grants toward antimicrobial and smart fabrics via the 14th Five-Year Plan, cementing its role as a global manufacturing hub for healthcare textiles technical-textiles.in. Indonesia's Jaminan Kesehatan Nasional (JKN) national insurance scheme is accelerating hospital bed additions, translating directly into higher procurement of privacy curtains and reusable bedding morganstanley.com. Medical-tourism hotspots such as Thailand and Malaysia are specifying advanced gowns and smart compression garments to attract international patients, fostering demand for higher-margin technologically advanced textiles.

Europe posts steady mid-single-digit growth, propelled by the European Environment Agency's 2024 PFAS risk assessment that places textiles on a path toward stricter chemical controls. Healthcare systems are actively replacing fluorinated barriers with bio-based coatings, a switch that benefits cellulose and polyethylene terephthalate-based fabrics treated with eco-certified chemistries. The European Green Deal's eco-design requirements are spurring investment in recyclable mono-material non-wovens and take-back logistics. South America and Middle East & Africa trail in market penetration but display pockets of rapid adoption: Brazil's private hospitals now pilot antimicrobial privacy curtains to curb nosocomial infections, while Saudi Arabia's Vision 2030 hospital projects include specifications for smart bedding that monitors patient vitals.

- Ahlstrom

- Amcor plc

- Asahi Kasei Corporation

- Avgol Industries 1953 Ltd,

- Brentano Fabrics

- Cardinal Health

- Carnegie Fabrics, LLC

- Designtex

- DuPont

- Eximius Innovative Pvt. Ltd.

- Freudenberg SE

- Herculite

- Johnson & Johnson

- KCWW (Kimberly-Clark Worldwide)

- Medline Industries, LP.

- MillerKnoll, Inc.

- Mitsui Chemicals, Inc.

- Toray Industries Inc.

- Trelleborg AB

- TWE GmbH & Co. KG,

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand in Developing Nations

- 4.2.2 Increasing Use of Cellulose Fibres in Healthcare

- 4.2.3 Hospital-acquired-infection (HAI) Reduction Mandates

- 4.2.4 Growing Adoption of Antimicrobial & Antiviral Finishes

- 4.2.5 Surge in Smart-textile Integration for Patient Monitoring

- 4.3 Market Restraints

- 4.3.1 Lack of Consumer Awareness

- 4.3.2 Volatile Petro-polymer Raw-material Prices

- 4.3.3 Inadequate Disposal Infrastructure for Single-use Fabrics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene

- 5.1.2 Polyester

- 5.1.3 Polyethylene

- 5.1.4 Cotton

- 5.1.5 Other Material Types (Cellulose-based Lyocell, etc.)

- 5.2 By Fabric Type

- 5.2.1 Woven

- 5.2.2 Non-Woven

- 5.2.3 Knitted

- 5.3 By Application

- 5.3.1 Privacy Curtains

- 5.3.2 Wall Coverings

- 5.3.3 Hygiene Products

- 5.3.4 Dressing Products

- 5.3.5 Bedding

- 5.3.6 Other Applications (Surgical Gowns & Drapes, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Ahlstrom

- 6.4.2 Amcor plc

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Avgol Industries 1953 Ltd,

- 6.4.5 Brentano Fabrics

- 6.4.6 Cardinal Health

- 6.4.7 Carnegie Fabrics, LLC

- 6.4.8 Designtex

- 6.4.9 DuPont

- 6.4.10 Eximius Innovative Pvt. Ltd.

- 6.4.11 Freudenberg SE

- 6.4.12 Herculite

- 6.4.13 Johnson & Johnson

- 6.4.14 KCWW (Kimberly-Clark Worldwide)

- 6.4.15 Medline Industries, LP.

- 6.4.16 MillerKnoll, Inc.

- 6.4.17 Mitsui Chemicals, Inc.

- 6.4.18 Toray Industries Inc.

- 6.4.19 Trelleborg AB

- 6.4.20 TWE GmbH & Co. KG,

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Textiles for Remote Monitoring and Telemedicine