PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846159

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846159

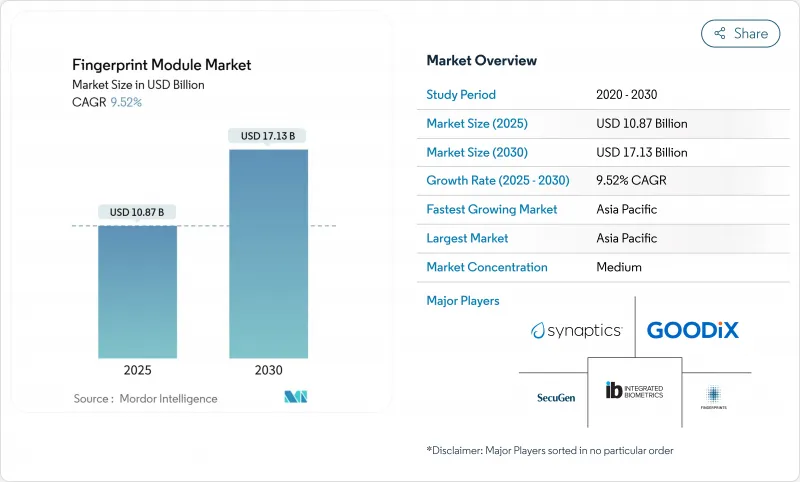

Fingerprint Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The fingerprint module market size is valued at USD 10.87 billion in 2025 and is forecast to reach USD 17.13 billion by 2030, reflecting a 9.52% CAGR.

Momentum stems from sovereign digital-identity projects, rapid smartphone authentication upgrades, and the commercial roll-out of biometric payment cards. Capacitive sensors still dominate volume demand, yet ultrasonic technology is expanding fastest as premium devices seek higher spoof-resistance. System-on-chip (SoC) integration is shrinking footprint and bill-of-materials costs, while in-display modules underpin the push for bezel-less handset designs. Volume procurement for Asia-Pacific government programs, falling average selling prices, and automotive adoption together keep the fingerprint module market on a multi-year growth arc.

Global Fingerprint Module Market Trends and Insights

Government Biometric ID Megaprojects Surge

Large-scale national identity programs are rewriting baseline demand. Ethiopia's Fayda scheme targets 90 million registrations by 2030, backed by USD 350 million in multilateral funding.Nigeria's USD 430 million digital ID project pursues universal coverage for more than 200 million citizens. Such contracts specify robust, long-life modules and create multi-year replenishment revenue. The volume sheerly outstrips consumer-device cycles, ensuring predictable pull for suppliers and stabilizing factory utilization across the fingerprint module market.

Explosive Smartphone Integration for On-Device Authentication

Flagship and mid-tier handsets now treat fingerprint biometrics as baseline functionality. Under-display modules permit full-screen designs, while ultrasonic units lift security by imaging sub-epidermal ridges. Android handset makers in North America and China have embedded dual sensing zones to quicken unlock speed, raising average content per device. This trend expands addressable volume and pressures suppliers to meet tighter thickness and power-budget envelopes.

Data-Privacy & Breach Litigation Risk

Class actions under statutes such as Illinois' BIPA have generated multimillion-dollar settlements for improper fingerprint capture, raising compliance overheads for enterprises. Corporate buyers now demand on-device template storage and revocable consent flows, extending design-in cycles and regulatory consultations. Vendors marketing the fingerprint module market solutions must add encryption, secure-element isolation, and third-party audits, which inflate the bill-of-materials and certification costs.

Other drivers and restraints analyzed in the detailed report include:

- Falling ASP of Capacitive & Optical Modules Broadens Adoption

- Biometric Payment Cards Reach Mass-Issuance Stage

- Hygiene Backlash on Touch Sensors in Post-Pandemic Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ultrasonic units contributed a minor yet fast-advancing slice of 2025 revenue and should expand at 10.2% CAGR to 2030, outpacing all other categories. Capacitive solutions still delivered the bulk of shipments, anchoring 58% fingerprint module market share in 2024. The fingerprint module market size for capacitive sensors rose on the back of low-cost Android models, whereas ultrasonic adoption correlated with premium ASP smartphones and finance-grade wearables.

Developers prize ultrasonic technology for its capacity to image sweat pores and sub-dermal capillary structures, defeating thin-film screen protectors and partial contaminants. Qualcomm's third-generation 3D Sonic packages achieve sub-200-micron Z-stack height, freeing OEMs to pursue edge-to-edge glass builds. Capacitive incumbents continue to raise spatial resolution and cut idle power below 5 µA, preserving relevance in mass-market phones and consumer IoT. Optical modules, meanwhile, land in mid-tier devices where backlighting can be reused from display engines to trim costs.

Area/touch modules accounted for 61% of 2024 due to proven reliability across consumer devices and enterprise door locks. Nonetheless, in-display sensors are forecast to climb 11.5% annually to 2030, reflecting handset makers' race for uninterrupted OLED panels. The fingerprint module market size linked to in-display designs will benefit from premium ASPs, offsetting lower density per handset.

Swipe sensors linger in point-of-sale terminals and rugged handhelds where narrow bezels remain. Hybrid touch-plus-pressure packages are gaining brand traction among notebook PC vendors, enabling palm-rest integration without enlarging the chassis. The sensor-type mix underlines the fingerprint module industry shift toward invisible biometrics that harmonize with industrial design goals.

The Fingerprint Module Market is Segmented by Technology (Optical, Capacitive, Ultrasonic, and More), Sensor Type (Area/Touch, Swipe, and More), Form Factor (Stand-Alone Module, System-On-Chip Integrated, and More), End-User Industry (Government and Law Enforcement, Consumer Electronics, and More), Application (Identity and Access Management, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific combined the world's biggest production basin with the largest deployment programs, holding 41% market share in 2024 and tracking a 9.8% CAGR to 2030. China's handset OEM ecosystem absorbs tens of millions of sensors monthly, while India's Digi Yatra expansion and airport e-gate tenders elevate domestic civil demand. ASEAN's commitment to interoperable digital public infrastructure harmonizes standards, letting suppliers ship common module footprints across multiple jurisdictions.

North America shows mature yet lucrative conditions: handset replacement cycles, wearables upgrades, and enterprise security retrofits keep volumes stable, whereas stringent privacy legislation prompts buyers to favor on-device template storage, lifting ASPs. The fingerprint module market continues to profit from U.S. automotive biometrics, where luxury brands localize sourcing to hedge supply-chain risk after North Carolina quartz mine disruptions threatened wafer output.

Europe advances on the back of GDPR-aligned national e-ID plans and bank-driven biometric card launches. Middle East & Africa's latent demand crystallizes in national ID projects such as Cameroon's 2025 biometric card roll-out under a 15-year concession. South America provides incremental gains as smartphones penetrate mid-income cohorts and governments modernize social-benefits disbursement platforms, though macro volatility elongates procurement cycles.

- Fingerprint Cards AB

- GOODIX Technology Inc.

- Synaptics Incorporated

- Integrated Biometrics LLC

- SecuGen Corporation

- HID Global Corporation

- Qualcomm Technologies Inc.

- Suprema Inc.

- Apple Inc.

- NITGEN Co., Ltd.

- NEC Corporation

- NEXT Biometrics ASA

- Anviz Global

- IDEMIA France SAS

- Thales Group

- Egis Technology Inc.

- IDEX Biometrics ASA

- Infineon Technologies AG

- Samsung Electronics Co., Ltd.

- ZKTeco Co., Ltd.

- Precise Biometrics AB

- Shenzhen SYNOCHEM Microelectronics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government biometric ID megaprojects surge

- 4.2.2 Explosive smartphone integration for on-device authentication

- 4.2.3 Falling ASP of capacitive and optical modules broadens adoption

- 4.2.4 Automotive and smart-gun makers embed fingerprint start/trigger modules

- 4.2.5 Biometric payment cards reach mass-issuance stage

- 4.3 Market Restraints

- 4.3.1 Data-privacy and breach litigation risk

- 4.3.2 Hygiene backlash on touch sensors in post-pandemic settings

- 4.3.3 Tight MEMS / IC packaging capacity limits supply elasticity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Optical

- 5.1.2 Capacitive

- 5.1.3 Ultrasonic

- 5.1.4 Thermal

- 5.1.5 Multispectral

- 5.2 By Sensor Type

- 5.2.1 Area/Touch

- 5.2.2 Swipe

- 5.2.3 In-display

- 5.2.4 Hybrid/Combo

- 5.3 By Form Factor

- 5.3.1 Stand-alone Module

- 5.3.2 System-on-Chip (SoC) Integrated

- 5.3.3 Embedded ASIC/Board-level

- 5.4 By End-user Industry

- 5.4.1 Government and Law Enforcement

- 5.4.2 Consumer Electronics

- 5.4.3 BFSI

- 5.4.4 Healthcare

- 5.4.5 Aviation

- 5.4.6 Automotive

- 5.4.7 Smart Home and IoT

- 5.4.8 Other Industrial

- 5.5 By Application

- 5.5.1 Identity and Access Management

- 5.5.2 Payment and Transaction Authentication

- 5.5.3 Time and Attendance

- 5.5.4 Border Control and Immigration

- 5.5.5 Device Unlocking

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 ASEAN-5

- 5.6.4.7 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 UAE

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fingerprint Cards AB

- 6.4.2 GOODIX Technology Inc.

- 6.4.3 Synaptics Incorporated

- 6.4.4 Integrated Biometrics LLC

- 6.4.5 SecuGen Corporation

- 6.4.6 HID Global Corporation

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Suprema Inc.

- 6.4.9 Apple Inc.

- 6.4.10 NITGEN Co., Ltd.

- 6.4.11 NEC Corporation

- 6.4.12 NEXT Biometrics ASA

- 6.4.13 Anviz Global

- 6.4.14 IDEMIA France SAS

- 6.4.15 Thales Group

- 6.4.16 Egis Technology Inc.

- 6.4.17 IDEX Biometrics ASA

- 6.4.18 Infineon Technologies AG

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 ZKTeco Co., Ltd.

- 6.4.21 Precise Biometrics AB

- 6.4.22 Shenzhen SYNOCHEM Microelectronics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment