PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846171

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846171

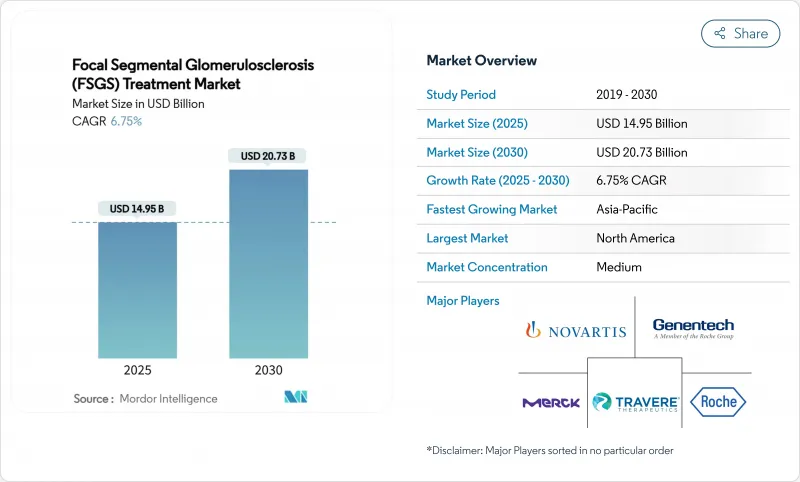

Focal Segmental Glomerulosclerosis (FSGS) Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Focal Segmental Glomerulosclerosis Treatment Market size is estimated at USD 14.95 billion in 2025, and is expected to reach USD 20.73 billion by 2030, at a CAGR of 6.75% during the forecast period (2025-2030).

The steady rise reflects the worldwide surge in disease recognition, rapid adoption of immunomodulating drugs and the launch of first-in-class therapies that directly target podocyte injury. The FSGS treatment market is also benefiting from a robust orphan-drug pipeline, streamlined approval pathways and the growing use of biomarker-guided regimens that shorten time to response. Precision medicine is reshaping prescribing behaviour, while value-based care agreements are helping payers manage the high upfront cost of novel biologics. Competitive activity remains intense, with large pharma firms buying promising biotech assets to gain an early foothold in the FSGS treatment market.

Global Focal Segmental Glomerulosclerosis (FSGS) Treatment Market Trends and Insights

Increasing Prevalence of FSGS Linked to Metabolic Disorders

The continuing rise of diabetes and obesity is directly fuelling FSGS incidence, as metabolic stress accelerates podocyte loss and glomerular sclerosis. Pharmaceutical developers are therefore testing dual-pathway agents that modulate both metabolic and renal signals. Earlier screening of hypertensive and diabetic patients is boosting diagnostic volumes, which in turn enlarges the addressable base of the FSGS treatment market. Clinicians are embedding metabolic control measures into care pathways, creating long-term demand for combo regimens that integrate glycaemic and lipid management with podocyte-protective drugs.

Robust Therapeutic Pipeline & R&D Funding

Vertex's inaxaplin, Travere's sparsentan and several antisense constructs have secured FDA Breakthrough Therapy or Orphan Drug designations, shortening regulatory timelines. Venture funding for kidney startups jumped 45% in 2024, which is encouraging smaller biotechs to pursue complement inhibitors, podocyte-regeneration biologics and gene-silencing molecules. Pipeline breadth is making the FSGS treatment market increasingly attractive to strategic investors, accelerating deal flow and advancing first-time modalities toward commercial launch.

High Cost & Limited Access to Dialysis and Transplant

Annual U.S. dialysis expenditure averages USD 89,000 per patient and a kidney transplant costs about USD 442,500. Limited transplant supply and long waiting lists amplify the burden. Payers therefore scrutinize the cost-effectiveness of every new entrant and are slow to endorse high-price cell or gene therapies without long-term outcome data. In low- and middle-income countries, dialysis capacity constraints create a stark treatment gap and temper uptake of premium drugs, muting part of the FSGS treatment market's growth potential.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Incentives for Rare Kidney Disease Drugs

- Advances in Single-Cell Renal Transcriptomics Enabling Precision Targets

- Clinical Trial Recruitment Challenges in Rare Disease

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary FSGS captured 61.08% of the FSGS treatment market in 2024 and is set to post a 9.01% CAGR through 2030. The strong share reflects sensitivity to immunomodulators and emerging targeted agents that block immune-mediated podocyte loss. APOL1 genotyping has become routine, and patients with high-risk alleles are enrolling in trials of genotype-specific inhibitors such as inaxaplin. The FSGS treatment market size for primary disease is therefore projected to outpace secondary FSGS, whose therapy still hinges on addressing diabetes, hypertension or drug toxicity.

Genetic testing is spawning micro-segments defined by APOL1 status, collapsing sub-populations into discrete commercial opportunities. AI-enhanced digital pathology further refines classification, allowing drug makers to align compounds with the most responsive cohorts. These precision tactics increase trial success probability and heighten investor confidence, reinforcing the central role of primary FSGS in steering the overall trajectory of the FSGS treatment market.

The Focal Segmental Glomerulosclerosis (FSGS) Treatment Market Report is Segmented by Disease Type (Primary FSGS, Secondary FSGS), Disease Management (Diagnosis, Treatment), End User (Hospitals & Transplant Centers, Specialty Clinics & Nephrology Practices, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 38.74% of 2024 revenue on the back of early biologic uptake, concentrated nephrology expertise and broad insurance coverage. The United States alone hosts more than 40,000 diagnosed patients, forming the largest single-country pool for upcoming precision therapies. Canada benefits from universal reimbursement that smooths access, while Mexico's expanding private-care segment is stimulating demand for advanced nephrology services.

Europe ranks second, supported by the EMA's PRIME pathway and coordinated health-technology assessment that fast-track high-need drugs. Germany, France and the United Kingdom spearhead usage of proteinuria-lowering agents, whereas Southern Europe leverages EU structural funds to upgrade renal-care infrastructure. Conditional marketing approvals granted after interim phase-3 readouts are allowing earlier patient access and reinforcing the FSGS treatment market's momentum across the continent.

Asia Pacific is the fastest-growing arena, scheduled to post an 18.60% CAGR to 2030. China's drive to include rare-disease drugs on provincial formularies is widening the reimbursement base, and Japan's established nephrology culture accelerates new-drug uptake. Korea's Kidney Health Plan 2033 commits to nationwide early detection, tele-nephrology and biopsy standardisation. India and Australia present divergent dynamics: India faces rural-urban access gaps yet offers the largest volume upside, while Australia leverages strong research networks to lead regional trials. Together, these forces ensure that the FSGS treatment market continues to globalise, with multinational firms tailoring launch plans to varied reimbursement and infrastructure realities.

- Roche

- Genentech

- Novartis

- Merck

- Teva Pharmaceutical Industries

- Travere Therapeutics Inc.

- Vertex Pharmaceuticals

- AstraZeneca

- Pfizer

- Bristol-Myers Squibb

- Otsuka Pharmaceutical Co. Ltd.

- Equillium Inc.

- Goldfinch Bio

- Reata Pharmaceuticals Inc.

- Ionis Pharmaceuticals

- Chinook Therapeutics Inc.

- Omeros Corporation

- LabCorp

- Arkana Laboratories

- Allina Health Laboratory

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of FSGS Linked to Metabolic Disorders

- 4.2.2 Robust Therapeutic Pipeline & R&D Funding

- 4.2.3 Regulatory Incentives for Rare Kidney Disease Drugs

- 4.2.4 Advances in Single-Cell Renal Transcriptomics Enabling Precision Targets

- 4.2.5 Rising Health-Equity Initiatives Expanding Early Biopsy in High-Risk Ethnic Populations

- 4.2.6 Increasing Adoption of Kidney Function Biomarkers for Early Diagnosis

- 4.3 Market Restraints

- 4.3.1 High Cost & Limited Access to Dialysis and Transplant

- 4.3.2 Clinical Trial Recruitment Challenges in Rare Disease

- 4.3.3 Adverse Effects & Relapse Rates with Current Immunosuppressants

- 4.3.4 Limited Long-Term Data for APOL1-Targeted Therapies

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Disease Type

- 5.1.1 Primary FSGS

- 5.1.2 Secondary FSGS

- 5.2 By Disease Management

- 5.2.1 Diagnosis

- 5.2.1.1 Kidney Biopsy

- 5.2.1.2 Creatinine Test

- 5.2.1.3 Other Diagnostics

- 5.2.2 Treatment

- 5.2.2.1 Drug Therapy

- 5.2.2.1.1 Corticosteroids

- 5.2.2.1.2 Calcineurin Inhibitors

- 5.2.2.1.3 Immunosuppressants

- 5.2.2.1.4 Biologics

- 5.2.2.1.5 APOL1 Inhibitors & Emerging Therapies

- 5.2.2.2 Dialysis

- 5.2.2.2.1 Hemodialysis

- 5.2.2.2.2 Peritoneal Dialysis

- 5.2.2.3 Kidney Transplant

- 5.2.1 Diagnosis

- 5.3 By End User

- 5.3.1 Hospitals & Transplant Centers

- 5.3.2 Specialty Clinics & Nephrology Practices

- 5.3.3 Dialysis Centers

- 5.3.4 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd.

- 6.3.2 Genentech Inc.

- 6.3.3 Novartis AG

- 6.3.4 Merck KGaA

- 6.3.5 Teva Pharmaceutical Industries Ltd.

- 6.3.6 Travere Therapeutics Inc.

- 6.3.7 Vertex Pharmaceuticals Incorporated

- 6.3.8 AstraZeneca plc

- 6.3.9 Pfizer Inc.

- 6.3.10 Bristol Myers Squibb Company

- 6.3.11 Otsuka Pharmaceutical Co. Ltd.

- 6.3.12 Equillium Inc.

- 6.3.13 Goldfinch Bio

- 6.3.14 Reata Pharmaceuticals Inc.

- 6.3.15 Ionis Pharmaceuticals Inc.

- 6.3.16 Chinook Therapeutics Inc.

- 6.3.17 Omeros Corporation

- 6.3.18 Labcorp

- 6.3.19 Arkana Laboratories

- 6.3.20 Allina Health Laboratory

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment