PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846185

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846185

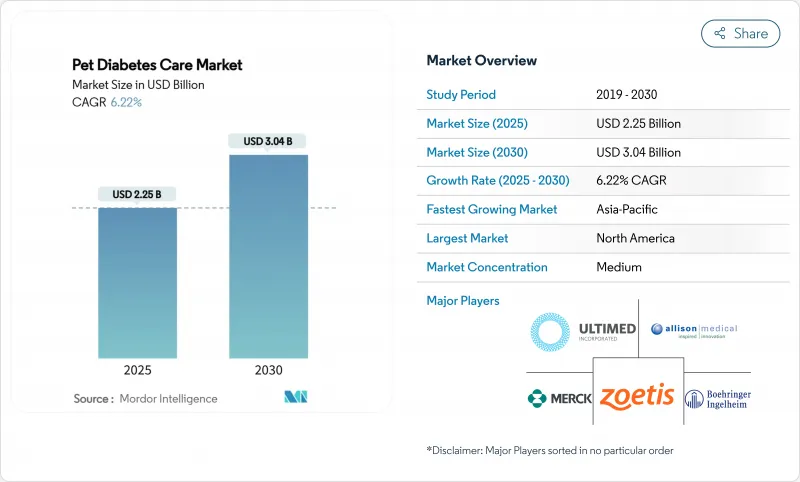

Pet Diabetes Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Pet Diabetes Care Market size is estimated at USD 2.25 billion in 2025, and is expected to reach USD 3.04 billion by 2030, at a CAGR of 6.22% during the forecast period (2025-2030).

Continued growth in the pet diabetes care market stems from the convergence of rising disease prevalence, the first-in-class oral SGLT-2 inhibitors for cats, and steady uptake of continuous glucose monitoring (CGM) devices. Increasing pet obesity, estimated at 22-40% in dogs and 19-52% in cats, enlarges the addressable base for the pet diabetes care market. At the same time, humanization of companion animals is lifting veterinary expenditure; U.S. households alone spend more than USD 136 billion per year on overall pet care, placing diabetes management firmly within discretionary budgets. Competitive intensity is moderate: three multinational leaders-Boehringer Ingelheim, Merck Animal Health, and Zoetis-dominate product innovation while smaller device specialists enter through CGM and tele-health niches.

Global Pet Diabetes Care Market Trends and Insights

Rising Prevalence of Diabetes & Pet Obesity

Obesity-driven metabolic dysfunction now affects as many as 52% of domestic cats, creating fertile ground for the pet diabetes care market. Recorded canine diabetes incidence has climbed 79.7% since 2006, translating to roughly 165,000 dogs under active treatment in the United States. Excess adiposity induces insulin resistance in both species, and the pathophysiology mirrors type 2 human diabetes, further validating pharmacologic crossover strategies. In affluent economies, lower activity levels and calorie-dense "human-grade" diets exacerbate the condition. An ageing pet population adds momentum because metabolic flexibility diminishes with age, thereby prolonging treatment duration and lifting the lifetime value of each diabetic pet to the pet diabetes care market.

Increase in Pet Adoption & "Pet-Parent" Spending

Post-pandemic social dynamics have redefined companion care budgets, with Millennials and Gen Z now representing more than 60% of new pet owners in the United States. A similar shift is visible in Asia-Pacific, where ownership rates reach 70-80% in India, Thailand, Indonesia, and China. Younger owners favour technology-enabled services and direct-to-consumer delivery, accelerating CGM and tele-vet adoption. The pet diabetes care market benefits because these demographics are more willing to finance chronic care, including wearable monitors, subscription insulin shipments, and personalized nutrition plans.

High Cost of Insulin & Monitoring Supplies

Diabetes management runs USD 120 - 386 per month, escalating annual outlays beyond USD 6,600 for complex cases. Insurance rarely covers pre-existing conditions, so most owners self-fund medication, syringes, CGM sensors, and lab checks. In lower-income economies, these costs suppress diagnosis rates and lengthen untreated disease duration. Even in mature markets, price sensitivity motivates the shift toward online pharmacies and subscription discounts, reshaping channel dynamics within the pet diabetes care market.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Veterinary Diagnostics & CGM Technology

- FDA Approvals of Novel Oral SGLT-2 Inhibitors for Cats

- Supply-Chain Risks for Animal-Sourced Insulin

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insulin therapy held 58.86% of the pet diabetes care market share in 2024, reflecting its entrenched status as first-line therapy. Oral drugs-chiefly the SGLT-2 class-are forecast to outpace at a 6.92% CAGR as newly diagnosed felines migrate away from injections. This shift, coupled with real-time glucose metrics, raises owner satisfaction and broadens uptake.

The pet diabetes care market size for oral medications is projected to grow in the coming years, buoyed by 88.4% response rates recorded in pivotal trials. Insulin delivery innovation continues through devices such as VetPen, yet CGM systems like GluCurve now anchor data-driven dose optimization. Collectively, these innovations introduce pluralistic treatment pathways that reduce reliance on a single modality and stabilize growth in the broader pet diabetes care market.

Canines constituted 65.12% of total therapy revenue in 2024 as higher disease prevalence and larger body mass translate to greater insulin volume use. The pet diabetes care market size for feline therapy nonetheless is climbing more quickly, reflecting a forecast 7.68% CAGR through 2030 on the back of oral therapy convenience.

Commercial availability of Bexacat and Senvelgo positions cats for meaningful share gains, and remission prospects in diet-controlled cases further elevate owner motivation. Parallel increases in CGM acceptance-for example, FreeStyle Libre 3 correlations of r = 0.86 under stable glycaemia-make at-home monitoring feasible even for smaller animals. These dynamics collectively expand the treated feline cohort within the pet diabetes care market.

The Pet Diabetes Care Market Report is Segmented by Care Type (Drug Type, Device Type), Animal Type (Canine, Feline), End User (Veterinary Hospitals and Clinics, Home-Care Settings), Distribution Channel (Veterinary Pharmacies, Online Retailers, Pet Specialty Stores), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 39.16% of 2024 revenue, supported by high insurance penetration and early access to SGLT-2 therapies. Forward growth remains steady as tele-medicine regulation relaxes and CGM reimbursement expands. Canada's pending exit from animal-sourced insulin, however, introduces near-term sourcing risk that could elevate costs and drive therapeutic substitutions.

Europe combines stringent regulatory oversight with receptive consumers. GDPR compliance shapes cloud data flows for CGM, yet harmonized VICH rules ease product registration, fostering cross-border launches for devices such as AlphaTrak 3. Northern markets are adopting AI-powered analyzers rapidly, while Southern states see incremental gains through rising pet humanization. Collectively, these dynamics reinforce Europe as a profitable yet compliance-heavy portion of the pet diabetes care market.

Asia-Pacific is the fastest-growing region with an 8.19% CAGR to 2030. Rising disposable income, smartphone penetration, and cultural acceptance of e-commerce fortify momentum. Japan and China anchor premium demand, whereas India and Indonesia supply volume growth through expanding pet bases. Government initiatives to support tele-veterinary services, notably in Thailand and Singapore, further accelerate digital treatment adoption in the pet diabetes care market.

- Boehringer Ingelheim

- Merck Animal Health (MSD)

- Zoetis

- Covetrus

- Beckton Dickinson

- Allison Medical

- MED TRUST

- TaiDoc Technology

- UltiMed

- Abbott (FreeStyle Libre)

- Dexcom

- Insulet Corp.

- IDEXX

- Elanco

- Virbac

- Vetoquinol

- Trupanion

- Companion Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Diabetes and Pet Obesity

- 4.2.2 Increase In Pet Adoption & "Pet-Parent" Spending

- 4.2.3 Advances in Veterinary Diagnostics & CGM Technology

- 4.2.4 AI-Powered Tele-Vet Glucose Analytics Platforms

- 4.2.5 FDA Approvals of Novel Oral SGLT-2 Inhibitors for Cats

- 4.2.6 Growing Insurer & VC Focus on Chronic Pet Disease Management

- 4.3 Market Restraints

- 4.3.1 High Cost of Insulin & Monitoring Supplies

- 4.3.2 Adverse Reactions to Insulin/Oral Agents

- 4.3.3 Supply-Chain Risks for Animal-Sourced Insulin

- 4.3.4 Data-Privacy Barriers to CGM Cloud Integration

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Care Type

- 5.1.1 By Drug Type

- 5.1.1.1 Insulin Therapy

- 5.1.1.2 Oral Medication

- 5.1.2 By Device Type

- 5.1.2.1 Glucose Monitoring Devices

- 5.1.2.2 Insulin Delivery Devices

- 5.1.1 By Drug Type

- 5.2 By Animal Type

- 5.2.1 Canine

- 5.2.2 Feline

- 5.3 By End User

- 5.3.1 Veterinary Hospitals & Clinics

- 5.3.2 Home-care Settings

- 5.4 By Distribution Channel

- 5.4.1 Veterinary Pharmacies

- 5.4.2 Online Retailers

- 5.4.3 Pet Specialty Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Boehringer Ingelheim

- 6.3.2 Merck Animal Health (MSD)

- 6.3.3 Zoetis

- 6.3.4 Covetrus

- 6.3.5 Becton Dickinson

- 6.3.6 Allison Medical

- 6.3.7 MED TRUST

- 6.3.8 TaiDoc Technology

- 6.3.9 UltiMed

- 6.3.10 Abbott (FreeStyle Libre)

- 6.3.11 Dexcom

- 6.3.12 Insulet Corp.

- 6.3.13 IDEXX Laboratories

- 6.3.14 Elanco Animal Health

- 6.3.15 Virbac

- 6.3.16 Vetoquinol

- 6.3.17 Trupanion

- 6.3.18 Companion Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment