PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846204

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846204

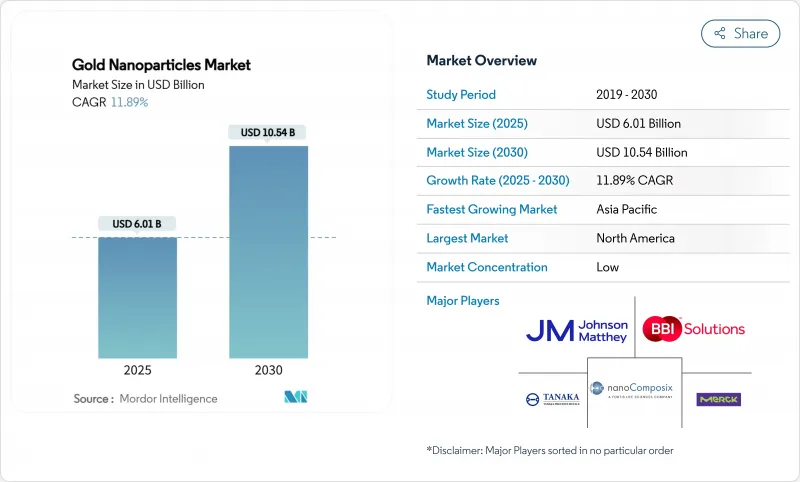

Gold Nanoparticles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Gold Nanoparticles Market size is estimated at USD 6.01 billion in 2025, and is expected to reach USD 10.54 billion by 2030, at a CAGR of 11.89% during the forecast period (2025-2030).

Escalating precision-medicine programs, persistent electronics miniaturization, and progress in continuous-flow green synthesis collectively lift demand for high-purity nanoparticles across healthcare, semiconductor, energy, and environmental use cases. Targeted drug-delivery platforms already account for 26.11% of current revenue and continue to attract investment as regulators approve more theranostic trials. Continuous-flow and microfluidic synthesis lines are scaling rapidly, lowering batch variability and hazardous-waste volumes while cutting operating expenses for producers. On the demand side, healthcare commands the largest uptake, yet the electronics segment registers the highest growth velocity as flexible and printed sensors migrate from lab to mass production. Gold-price volatility remains an operational risk, but coatings that reduce precious-metal loading per unit and recycling initiatives buffer near-term margin swings.

Global Gold Nanoparticles Market Trends and Insights

Rising Nanotechnology Applications in Medical Industry

Hospitals, contract research organizations, and device makers are moving beyond passive drug carriers to multifunction theranostic constructs that combine imaging and therapy on a single gold core, enabling clinicians to destroy tumors via photothermal heating while concurrently tracking treatment in real time. DNA-barcoded nanoparticle libraries now let oncologists screen several payload combinations inside one patient sample, cutting preclinical timelines and raising response rates for hard-to-treat malignancies. Regulatory agencies have accelerated review pathways for nanomedicines that demonstrate clear biocompatibility, helping three US clinical programs move into Phase II during 2025. Research teams are also probing neural-interface coatings that could translate the same plasmonic heating principle to minimally invasive brain stimulation. As datasets validate long-term safety profiles, hospital purchasing groups are earmarking budget for nanoparticle-guided ablation systems that integrate with standard imaging consoles. These transitions collectively add 3.2 percentage points to the gold nanoparticles market CAGR through mid-decade.

Growing Adoption in High-End Electronics & Photonics

Smart-watch, e-textile, and implantable sensor makers insert gold nanowires into ultrathin circuitry to raise conductivity while keeping bending radii below 1 mm, a key threshold for comfortable skin-mounted patches. Photonics research shows that embedding 10 nm spheres inside organic solar-cell photo-absorbers can lift power-conversion efficiency by more than 30% through localized surface-plasmon amplification RFID developers leverage gold seeds to boost antenna gain at gigahertz frequencies, widening read ranges without increasing tag size. Production readiness is high thanks to inkjet-printable nanoparticle inks that sinter at temperatures below 120 °C, compatible with PET and TPU films used in wearables. The electronics driver injects 2.8 points into forecast CAGR, with commercial shipments already ramping at factories in Japan, South Korea, and Taiwan that supply the global notebook, smartphone, and IoT modules sectors.

Volatility in Gold Prices

Benchmark bullion prices climbed almost 25% during the first half of 2025 as investors sought havens amid geopolitical shocks, pushing nanoparticle producers' raw-material spend to multi-year highs. Exchange-traded funds added more than 160 tonnes during the same window, siphoning supply from industrial channels. Many device OEMs lock quarterly contracts, yet spot spikes feed through to specialty ink and reagent catalogs within weeks, delaying project launches in diagnostics and printed-electronics niches. Hedging offers partial relief but raises working-capital needs, squeezing small firms that lack scale. Protective coatings that enable 30% metal-content reduction per chip are mitigating the blow, though adoption is uneven in medical segments that demand thicker biocompatible shells. The restraint subtracts 2.3 points from near-term CAGR until bullion prices stabilize or recycling yields improve.

Other drivers and restraints analyzed in the detailed report include:

- Sustainable Green Synthesis Methods Lowering Regulatory Risk

- Precision Oncology Demand for Theranostic Agents

- Safety & Long-Term Toxicity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical reduction accounted for 40.55% of the gold nanoparticles market size in 2024, a legacy position rooted in established batch infrastructure across North America and Europe. Yet downstream users now demand tighter particle-size distributions and lower solvent footprints, tipping procurement decisions toward continuous-flow lines that log a robust 12.45% CAGR to 2030. Plant operators retrofit vortex-fluidic modules that shear precursor streams into micron-thick films, promoting uniform nucleation while capturing hydrogen coproduct for on-site boiler fuel. AI-guided sensors adjust residence-time loops in real time, holding polydispersity indexes below 0.08 and elevating lot-to-lot reproducibility for pharmaceutical customers.

The shift also intersects with green-chemistry imperatives because flow reactors use aqueous media and ambient pressure, slashing energy intensity by nearly one-third versus citrate batch routes. Seed-mediated growth schemes layered onto the same skid allow production of rods, prisms, and core-shell configurations without opening the system, minimizing contamination risk. Developers of high-resolution biosensors increasingly embed bespoke shapes generated via flow-switch programming, capturing margin premiums well above commodity colloids. As validation batches scale, analysts expect continuous-flow capacity share to pass 30% by 2028, cementing its status as the new reference standard for regulated therapeutic and diagnostic end uses.

The Gold Nanoparticles Market Report is Segmented by Synthesis Method (Chemical Reduction, Green/Biological Synthesis, and More), Application (Imaging, Targeted Drug Delivery, and More), End-User Industry (Electronics & Semiconductors, Healthcare & Life Sciences, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 36.33% of global revenue in 2024, underpinned by deep R&D budgets, FDA oversight that standardizes quality, and integrated supply chains bridging academic labs with contract manufacturers. Academic-industry consortia in Boston and San Diego help spin off start-ups that license nanoparticle IP for oncology, cardiology, and neurology applications. Stimulus grants channeled through the National Institutes of Health in 2025 further enlarge domestic pilot capacities, ensuring short lead times for clinical-grade material.

Asia-Pacific posts the swiftest 12.98% CAGR, reflecting China's large-scale colloid reactors, India's expanding generics sector, and Japan's sensor innovation ecosystem. Policy incentives in Guangdong and Zhejiang provinces reimburse up to 20% of capital outlays for continuous-flow lines that meet ISO 14001 benchmarks, fast-tracking green production footprints. Semiconductor companies headquartered in Seoul and Hsinchu consume rising nanoparticle volumes for high-density interposers and thermal-interface pads, while ASEAN electronics exporters use printed antennas in logistics trackers and smart-package labels.

Europe balances regulatory rigour with sustainability leadership, supporting market development through Horizon Europe grants that prioritize green-chemistry upgrades and circular-economy pilot trials. German automotive suppliers validate gold-catalyzed NOx-reduction modules engineered for next-generation fuel-cell vehicles. Meanwhile, Nordic med-tech clusters incorporate nanoparticle tags into rapid-sepsis tests aimed at point-of-care settings, addressing public-health priorities under the EU's Beating Cancer Plan.

- Abcam

- Aurion

- BBI Solutions

- Creative Diagnostics

- Cytodiagnostics Inc.

- Johnson Matthey Plc

- Meliorum Technologies Inc.

- Merck KGaA

- nanoComposix

- NanoHybrids

- Nanopartz Inc.

- Sona Nanotech Inc.

- TANAKA Holdings Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Nanotechnology Applications in Medical Industry

- 4.2.2 Growing Adoption in High-end Electronics and Photonics

- 4.2.3 Sustainable Green Synthesis Methods Lowering Regulatory Risk

- 4.2.4 Precision Oncology Demand for Theranostic Agents

- 4.2.5 Next-Gen Flexible/Printed Sensors for IoT Devices

- 4.3 Market Restraints

- 4.3.1 Volatility in Gold Prices

- 4.3.2 Safety and Long-term Toxicity Concerns

- 4.3.3 Emerging Nano-material Substitutes (e.g., Quantum Dots)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Synthesis Method

- 5.1.1 Chemical Reduction

- 5.1.2 Green/Biological Synthesis

- 5.1.3 Seed-mediated Growth

- 5.1.4 Continuous Flow and Microfluidic

- 5.1.5 Other Methods

- 5.2 By Application

- 5.2.1 Imaging

- 5.2.2 Targeted Drug Delivery

- 5.2.3 Sensors

- 5.2.4 In Vitro Diagnostics

- 5.2.5 Probes

- 5.2.6 Catalysis

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Electronics and Semiconductors

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Chemicals and Catalysts

- 5.3.4 Energy and Environmental

- 5.3.5 Other End-User Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 NORDIAC

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Abcam

- 6.4.2 Aurion

- 6.4.3 BBI Solutions

- 6.4.4 Creative Diagnostics

- 6.4.5 Cytodiagnostics Inc.

- 6.4.6 Johnson Matthey Plc

- 6.4.7 Meliorum Technologies Inc.

- 6.4.8 Merck KGaA

- 6.4.9 nanoComposix

- 6.4.10 NanoHybrids

- 6.4.11 Nanopartz Inc.

- 6.4.12 Sona Nanotech Inc.

- 6.4.13 TANAKA Holdings Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Innovation in the Field of Electronics