PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846211

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846211

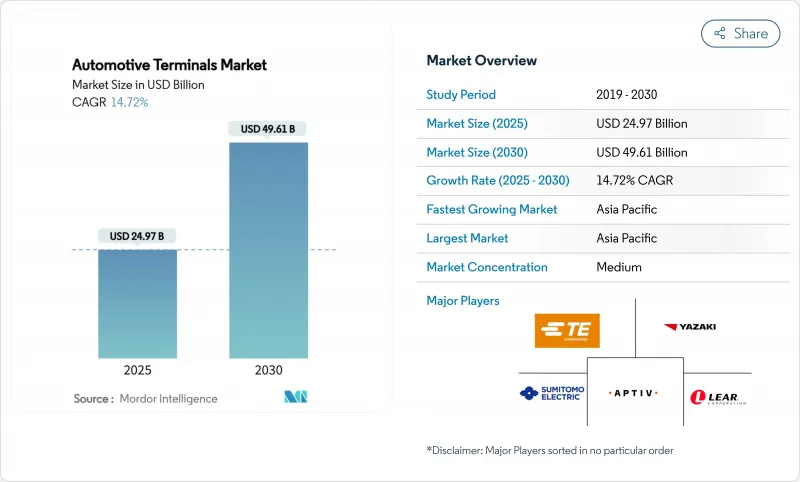

Automotive Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Automotive Terminals Market size is estimated at USD 24.97 billion in 2025, and is expected to reach USD 49.61 billion by 2030, at a CAGR of 14.72% during the forecast period (2025-2030).

A rapid shift toward 48 V low-voltage architectures, exemplified by Tesla's Low-Voltage Connector Standard that reduces connector SKUs to six while still covering more than 90% of signal and power needs, is compressing weight, cutting material usage, and accelerating harness automation. Terminal suppliers also benefit from ADAS proliferation, with retrofit programs in North America and Europe raising aftermarket demand for data-grade, shielded micro-connectors capable of multigigabit transmission. Meanwhile, copper-intensive battery systems require three times the conductor mass of internal-combustion platforms, pushing OEMs to lock multi-year supply contracts even as volatile spot prices pressure gross margins

Global Automotive Terminals Market Trends and Insights

Electrification-Led Explosion in Low-Voltage Connection Points

Vehicle electrification multiplies the number of low-voltage nodes: a contemporary battery electric platform integrates more than 200 distinct connection points against fewer than 100 in conventional 12 V cars. Battery management systems is growing at a robust CAGR, demanding ultra-compact terminals that monitor cell voltage and temperature at millisecond intervals. The higher current density of 48 V distribution increases the thermal load on contact surfaces, prompting the adoption of new tin-silver plating recipes that sustain 100 A continuous loads without fretting corrosion. Commercial fleets extend this demand signal, retrofitting 48 V electric turbochargers and regenerative accessories that add four to six new harness branches per vehicle.

Shift to 48 V Electrical Architectures in Premium Vehicles

BMW, Mercedes-Benz, and Volvo now fit 48 V subsystems across all premium models launched since mid-2024, delivering power for active chassis, e-turbochargers, and zone controllers without oversizing wire gauges. Harness weight falls by up to 19 kg per vehicle, translating to 0.3 L/100 km fuel savings or extended EV range when paired with auxiliary electrics. Tesla's LVCS proves that a 48 V backbone can coexist with legacy 12 V loads through DCDC nodes, allowing phased migration that protects aftermarket compatibility. Terminals must now guarantee 60 V DC dielectric strength while remaining backward-compatible with existing crimp tooling.

Copper Price Volatility is Squeezing Terminal BOM Margins

Copper averaged USD 10,800 per tonne in early 2024. Early 2025 saw rising copper prices due to U.S. tariffs and a weaker dollar, but fears of a global slowdown and China's retaliatory tariffs have weighed heavily on prices and demand outlooks. Chinese smelters face tightening concentrate availability after the closure of Chilean open-pit pits with declining ore grades, forcing fabricators to negotiate quarterly price escalators. Recycling helps offset volatility: US brass-rod mills certified average recycled content more than four fifth of the amount in 2025, reducing primary copper exposure by 38 kt.

Other drivers and restraints analyzed in the detailed report include:

- ADAS Retrofit Kits Creating Aftermarket Demand Spikes

- Stringent ISO 19642 Harness Standards Accelerate Terminal Redesign Cycles

- OEM Migration to Consolidated Connector Blocks Reduces Terminal Counts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery systems contributed 33.25% of the automotive terminals market share in 2024, underscoring their status as the most terminal-intensive sub-system across the automotive terminal market. Unit growth stems from cell-level sensing and rising pack voltages that push contact density beyond 1,400 pins in next-generation skateboard chassis. Safety & ADAS is growing at 14.81% CAGR through 2030 because each camera and radar module adds four to six shielded connections.

Emerging solid-state packs drive micro-terminal adoption, whose pitch falls below 0.35 mm, generating premium pricing. HVAC and comfort segments, despite their modest share, gain relevance as 48 V blowers, seat heaters, and heat pumps switch to brushless motors, lifting current draw and prompting copper busbar integration.

Passenger cars contributed to 64.85% of the automotive terminals market share in 2024, growing at 15.73% CAGR as stricter CO2 targets favor zero-tailpipe solutions. Light commercial vehicles (LCV) also grow steadily as parcel operators electrify last-mile fleets to comply with urban low-emission zones. Motorcycles and scooters leverage swappable battery platforms that spur standardization of IP67 sealed DC terminals.

Fleet operators measure lifecycle economics rigorously: every unscheduled roadside repair on high-utilization LCVs costs fairly in delivery penalties, incentivizing premium high-cycle terminals. Aptiv's CTCS heavy-duty connectors survive 30.6 G vibration and temperatures from -40 °C to +140 °C, offering uptime advantages that justify 14-18% price premiums in total-cost-of-ownership models.

The Automotive Terminals Market Report is Segmented by Application (Battery System, Lighting System, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Terminal Type (Ring Terminals, Spade Terminals, and More), Material (Copper, Brass, and More), Current Rating (Less Than 25 Amp and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with a 37.76% automotive terminals market share in 2024 and is showcasing the fastest 15.21% CAGR through 2030, underpinned by China's control of global new-energy vehicle production. Japan's tier-one suppliers leverage decades of lean manufacturing to ship precision-stamped contacts with single-digit PPM defect rates to global OEMs. Southeast Asian nations such as Indonesia and Thailand recorded triple-digit EV registration growth in 2024, prompting OEMs to localize connector and wire-harness production.

Europe, even after regional automotive revenue fell short amid inflation and energy-cost headwinds. Strict fleet CO2 rules lift EV sales to an expected figure in 2025, feeding demand for high-power charging terminals and data-grade board-to-board connectors, etc. Germany targets 873,000 new EV registrations, cementing local-content requirements for terminal suppliers. The region's regulatory leadership through ISO 19642 and DIN 72036 gives compliant vendors a first-mover edge even as economic stagnation tempers near-term margins.

An aging vehicle parc keeps the aftermarket vibrant and accelerates ADAS retrofit kit sales that rely on premium shielded connectors. General Motors' USD 4 billion plant overhaul, Hyundai's USD 21 billion multiyear expansion, and Clarios' investment strategy guarantee a steady pull for advanced 48V and 800V terminals. Middle East & Africa and South America collectively contributed a affairly decent share in 2024, with South America portraying steady growth on the back of Brazil's CO2 mandates and Argentina's lithium-mining incentives. Saudi Arabia and the United Arab Emirates use local-content policies within nascent EV assembly programs to stimulate regional cable and terminal manufacturing clusters.

- TE Connectivity

- Lear Corporation

- Aptiv PLC

- Viney Corporation

- Furukawa Electric Co., Ltd.

- Grote Industries

- Keats Manufacturing Co.

- Sumitomo Electric Industries, Ltd.

- Yazaki Corporation

- Amphenol Corporation

- K.S. Terminals Inc.

- Hirose Electric Co., Ltd.

- Littelfuse, Inc.

- Samtec Inc.

- Wurth Elektronik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-led explosion in low-voltage connection points

- 4.2.2 Shift to 48-V electrical architectures in premium vehicles

- 4.2.3 ADAS retrofit kits creating aftermarket demand spikes

- 4.2.4 Stringent ISO 19642 harness standards accelerating terminal redesign cycles

- 4.2.5 Solid-state battery BMS requiring high-precision micro-terminals

- 4.2.6 Automaker push for crimp-less laser-weld terminals to cut assembly takt-time

- 4.3 Market Restraints

- 4.3.1 Copper price volatility squeezing terminal BOM margins

- 4.3.2 OEM migration to consolidated connector blocks reducing terminal counts

- 4.3.3 Reliability issues in aluminum-alloy ring terminals for EV high-current paths

- 4.3.4 Skills gap in automated crimp-force monitoring on new Asian lines

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Battery System

- 5.1.2 Lighting System

- 5.1.3 Infotainment System

- 5.1.4 Powertrain & Engine Management

- 5.1.5 Safety and ADAS

- 5.1.6 HVAC and Comfort

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.3 By Terminal Type

- 5.3.1 Ring Terminals

- 5.3.2 Spade Terminals

- 5.3.3 Quick-Connect Terminals

- 5.3.4 Butt Connectors

- 5.3.5 Multi-Pin Connectors

- 5.4 By Material

- 5.4.1 Copper

- 5.4.2 Brass

- 5.4.3 Steel

- 5.4.4 Other Alloys

- 5.5 By Current Rating

- 5.5.1 Less than 25 Amp

- 5.5.2 25 - 50 Amp

- 5.5.3 More than 50 Amp

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Russia

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 South Africa

- 5.7.5.5 Nigeria

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 TE Connectivity

- 6.4.2 Lear Corporation

- 6.4.3 Aptiv PLC

- 6.4.4 Viney Corporation

- 6.4.5 Furukawa Electric Co., Ltd.

- 6.4.6 Grote Industries

- 6.4.7 Keats Manufacturing Co.

- 6.4.8 Sumitomo Electric Industries, Ltd.

- 6.4.9 Yazaki Corporation

- 6.4.10 Amphenol Corporation

- 6.4.11 K.S. Terminals Inc.

- 6.4.12 Hirose Electric Co., Ltd.

- 6.4.13 Littelfuse, Inc.

- 6.4.14 Samtec Inc.

- 6.4.15 Wurth Elektronik

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment