PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846240

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846240

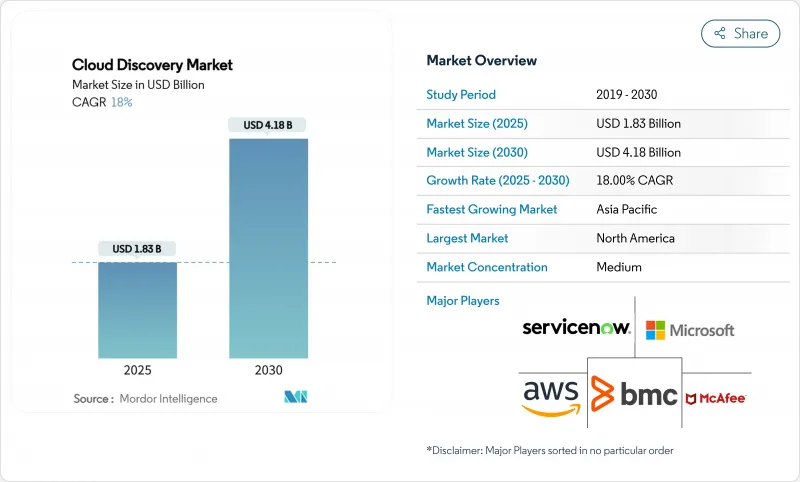

Cloud Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Cloud Discovery Market size is estimated at USD 1.83 billion in 2025, and is expected to reach USD 4.18 billion by 2030, at a CAGR of 18% during the forecast period (2025-2030).

Rapid multi-cloud adoption, stricter zero-trust mandates, and sustainability reporting rules are reshaping enterprise security architecture by making continuous asset visibility a board-level priority. Vendors that embed agentless discovery, automated classification, and FinOps-ready analytics into their platforms are gaining share as enterprises shift from one-time audits to real-time monitoring. North American demand remains anchored in federal compliance frameworks, while APAC's sovereign-cloud initiatives are accelerating regional uptake. Budget constraints at smaller organizations and persistent credential-access hurdles in segmented networks moderate overall growth, but sustained innovation in AI-driven automation continues to expand total addressable demand.

Global Cloud Discovery Market Trends and Insights

Growing Multi-Cloud Adoption Among Global 2000 Enterprises

Organizations now run production workloads across an average of 3.2 public clouds, a strategy that boosts resilience but fragments visibility. Discovery engines must therefore interface with multiple provider APIs, container orchestration layers, and service meshes in near real time. Early adopters in Asia are compelled to run parallel domestic and international cloud estates because of sovereign-cloud directives, reinforcing demand for platform-agnostic discovery. ServiceNow's integration with a leading hyperscaler illustrates how workflow automation and discovery are converging to shorten response times across hybrid estates.Without these capabilities, enterprises report discovery lags of up to 72 hours, exposing security and compliance blind spots that regulators increasingly penalize.

Rising Need for Real-Time Configuration Visibility to Harden Cyber-Resilience

Misconfigurations continue to account for the overwhelming majority of cloud breaches, prompting regulators to enforce continuous monitoring requirements. The U.S. Department of Defense's updated cloud clause obliges contractors to track data location and remediate drift instantly. Healthcare providers, subject to HIPAA and ransomware threats, are leading investments in real-time discovery tied to data-security-posture management. Vendors integrating discovery with AI-driven threat analytics claim mean-time-to-detect reductions of more than 30%. Manufacturing firms report double-digit improvements in overall equipment effectiveness after embedding continuous asset discovery within industrial IoT environments.

Persistent Credential-Access Hurdles in Highly Segmented Networks

Zero-trust designs intentionally restrict lateral movement, requiring discovery engines to authenticate separately in every micro-segment. Financial services institutions must also segregate business-unit data by jurisdiction, multiplying credential overhead.Healthcare providers face comparable challenges when isolating protected health information. Agentless approaches alleviate some friction yet still struggle with depth, forcing trade-offs between breadth and granularity. Enterprises estimate that 40-60% of discovery budgets are consumed by credential management tasks alone.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of FinOps and ITOM Driving Discovery Modules Into Cost-Governance Stacks

- GenAI-Powered Auto-Classification Reducing CMDB Maintenance Cost

- SMB Budget Squeeze for Discovery Licences and Staff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Professional services captured 68% of the cloud discovery market in 2024, underscoring enterprises' reliance on specialized architects to integrate discovery engines with complex identity, network, and workflow layers. Engagement scopes typically cover multi-cloud API mapping, policy tuning, and CMDB population-all tasks requiring deep vendor expertise. Managed services, however, are forecast to accelerate at a 24% CAGR through 2030 as enterprises recognize that discovery must run continuously rather than ad-hoc.

Growth in managed offerings signals a structural shift in spending from project-based deployments to subscription models anchored in ongoing visibility. ServiceNow's managed discovery subscriptions contributed materially to its USD 2,866 million Q4 2024 recurring revenue, illustrating the appeal of outcome-based contracts. Manufacturing clients adopting always-on discovery have reported 10-15% boosts in operational effectiveness through faster anomaly detection. The shift also benefits vendors, as automated classification reduces marginal delivery costs and widens adoption among organizations lacking full-time cloud-security staff.

The Cloud Discovery Market is Segmented by Service (Professional, Managed), End-User Industry (IT and Telecommunication, BFSI, Retail and Consumer Goods, Industrial Manufacturing, Healthcare and Other Industries), and Geography

Geography Analysis

North America held 38% of 2024 revenue thanks to early enterprise cloud adoption, a mature hyperscale ecosystem, and federal mandates that embed discovery clauses in government contracts. Financial institutions, defense contractors, and healthcare networks represent the largest buyer clusters, while Canadian firms increasingly adopt managed discovery to address cross-border data movement. Competition remains intense as established IT-service-management vendors integrate discovery into broader workflow suites, yet market saturation among Fortune 1000 firms tempers incremental growth.

APAC is projected to post a 22% CAGR from 2025-2030, the fastest worldwide, driven by sovereign-cloud policies and localization laws that force companies to inventory assets at the regional level. More than one-third of Asia-Pacific governments plan to deploy sovereign clouds by 2026, compelling enterprises to maintain granular records of workload residency. Data-center capacity in the region topped 12,000 MW in 2024, and a further 14,000 MW is under construction, magnifying the need for hybrid-cloud visibility. Industries such as financial services and sovereign defense lead adoption, while emerging digital-native enterprises accelerate managed-service uptake.

Europe represents a sizable, compliance-driven market where GDPR and the Corporate Sustainability Reporting Directive make discovery essential for both data protection and emissions accounting. Enterprises leverage discovery engines to map data flows and assign Scope 3 carbon factors, enabling transparent ESG disclosures. Uptake is most pronounced in Germany, France, and the Nordics, where energy-efficient cloud zones intersect stringent data-residency rules. While growth rates are lower than in APAC, vendors benefit from long contract tenures due to high switching costs tied to regulatory certification. South America and the Middle East & Africa remain nascent but promising; telco-led cloud rollouts and public-sector digitization programs are laying the groundwork for future demand, provided pricing aligns with constrained IT budgets.

- ServiceNow Inc.

- BMC Software Inc.

- Microsoft Corp.

- Amazon Web Services Inc.

- Cisco Systems Inc.

- IBM Corp.

- Broadcom Inc. (Symantec)

- McAfee LLC

- Palo Alto Networks Inc.

- Fortinet Inc.

- Splunk Inc.

- Dynatrace Inc.

- New Relic Inc.

- vArmour Networks Inc.

- Tenable Inc.

- Qualys Inc.

- Rapid7 Inc.

- Wiz Inc.

- Lacework Inc.

- Orca Security Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Market Drivers

- 4.1.1.1 Growing multi-cloud adoption among Global 2000 enterprises

- 4.1.1.2 Rising need for real-time configuration visibility to harden cyber-resilience

- 4.1.1.3 Convergence of FinOps and ITOM driving discovery modules into cost-governance stacks

- 4.1.1.4 GenAI-powered auto-classification reducing CMDB maintenance cost*

- 4.1.1.5 Mandatory asset-discovery clauses in new U.S. Federal Zero-Trust contracts*

- 4.1.1.6 Sustainability reporting rules (CSRD, SEC) demanding cloud-asset inventories*

- 4.1.2 Market Restraints

- 4.1.2.1 Persistent credential-access hurdles in highly segmented networks

- 4.1.2.2 SMB budget squeeze for discovery licences and staff

- 4.1.2.3 Sovereign-cloud restrictions limiting discovery scope outside region*

- 4.1.2.4 Shadow-IT growth outpacing discovery coverage despite tool upgrades*

- 4.1.3 Value/Supply-Chain Analysis

- 4.1.4 Regulatory Landscape

- 4.1.5 Technological Outlook

- 4.1.6 Porter's Five Forces

- 4.1.6.1 Threat of New Entrants

- 4.1.6.2 Bargaining Power of Buyers

- 4.1.6.3 Bargaining Power of Suppliers

- 4.1.6.4 Threat of Substitutes

- 4.1.6.5 Competitive Rivalry

- 4.1.1 Market Drivers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service

- 5.1.1 Professional

- 5.1.2 Managed

- 5.2 By End-user Industry

- 5.2.1 IT and Telecommunication

- 5.2.2 BFSI

- 5.2.3 Retail and Consumer Goods

- 5.2.4 Industrial Manufacturing

- 5.2.5 Healthcare

- 5.2.6 Other Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 South America

- 5.3.3 Europe

- 5.3.4 APAC

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ServiceNow Inc.

- 6.4.2 BMC Software Inc.

- 6.4.3 Microsoft Corp.

- 6.4.4 Amazon Web Services Inc.

- 6.4.5 Cisco Systems Inc.

- 6.4.6 IBM Corp.

- 6.4.7 Broadcom Inc. (Symantec)

- 6.4.8 McAfee LLC

- 6.4.9 Palo Alto Networks Inc.

- 6.4.10 Fortinet Inc.

- 6.4.11 Splunk Inc.

- 6.4.12 Dynatrace Inc.

- 6.4.13 New Relic Inc.

- 6.4.14 vArmour Networks Inc.

- 6.4.15 Tenable Inc.

- 6.4.16 Qualys Inc.

- 6.4.17 Rapid7 Inc.

- 6.4.18 Wiz Inc.

- 6.4.19 Lacework Inc.

- 6.4.20 Orca Security Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment