PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846256

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846256

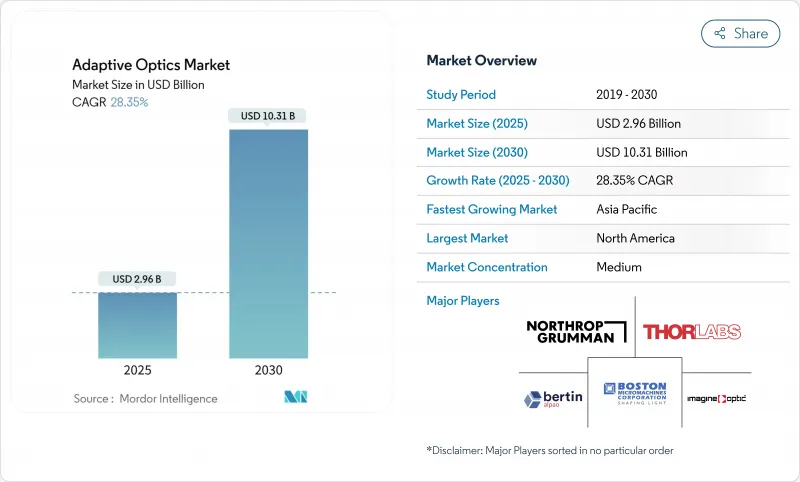

Adaptive Optics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The adaptive optics market size is valued at USD 2.96 billion in 2025 and is forecast to reach USD 10.31 billion by 2030, advancing at a 28.35% CAGR.

Demand is powered by government spending on directed-energy programs, semiconductor inspection needs at sub-nanometer precision, and rising consumer electronics applications such as AR/VR waveguide displays. Large-aperture telescope upgrades in Europe and Asia's expanding space-situational-awareness programs reinforce the technology's relevance. Machine-learning-based wavefront reconstruction, pivotal in next-generation control systems, is reducing calibration latency and broadening commercial appeal. The adaptive optics market is also benefitting from rapid adoption in retinal imaging devices as FDA classification changes shorten approval timelines for advanced ophthalmic platforms.

Global Adaptive Optics Market Trends and Insights

Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging

Ophthalmic device makers now integrate multi-conjugate adaptive optics to capture cellular-level retinal images, enabling earlier disease detection. FDA reclassification of ultrasound cyclodestructive devices from Class III to Class II in 2024 signals a more predictable pathway for advanced imaging platforms. Alcon's Unity VCS and Unity CS clearances illustrate growing commercial readiness, while AI-powered wavefront algorithms reduce chair-time calibration. Start-ups such as Profundus Imaging are developing prototypes that widen corrected fields of view through multiple deformable mirrors. These advances lower ownership hurdles for clinics beyond major academic centers and accelerate the adaptive optics market's healthcare reach.

Deployment in Directed-Energy & Free-Space Laser Communication Programs

The U.S. Department of Defense channels more than USD 1 billion annually into high-energy laser systems, with Lockheed Martin scaling to 300 kW devices that rely on adaptive optics for beam quality over long distances. The Space Development Agency's Proliferated Warfighter Space Architecture budgets USD 35 billion through 2029, embedding laser cross-links that need precise wavefront control. AI-enabled turbulence-forecasting tools such as TAROQQO from the University of Ottawa now refine free-space quantum channels in real time. Together these programs shorten development cycles, reinforce supply chains, and enlarge the adaptive optics market for military and secure-communication uses.

High CapEx of High-Actuator Deformable Mirrors

Deformable mirrors with 120 X 120 actuators raise unit costs that small manufacturers struggle to justify. Supply chain pressures, including export restrictions on germanium and gallium, inflate raw-material pricing for optical substrates. Alternative chalcogenide materials, such as BDNL4, lower dependence on restricted metals but require re-tooling that adds near-term expenses. The flat photonics-laser market, valued at USD 23 billion in 2024, narrows suppliers' ability to absorb capital outlays. These factors trim growth in price-sensitive verticals and impose caution on prospective entrants to the adaptive optics market.

Other drivers and restraints analyzed in the detailed report include:

- Large-Aperture Telescope Upgrades (ELT, TMT)

- Commercial Semiconductor Wafer & EUV Mask Inspection

- Complex Closed-Loop Design & Calibration Skills Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wavefront Sensors dominated 38% of the adaptive optics market share in 2024, anchored by Shack-Hartmann arrays that feed real-time aberration data to downstream controls. Shack-Hartmann's simplicity keeps cost low, while pyramid sensors gain traction for extreme adaptive optics astronomy. Control Systems & Software are projected to grow at 31.44% CAGR; spatiotemporal Gaussian process models cut wavefront phase variance by up to 3.5X versus non-predictive loops. Deformable Mirrors, the mechanical workhorses, are shifting toward MEMS architectures with 42% technology share that supports consumer price points. Other components, including tip-tilt mirrors, address specialized fine-pointing tasks in laser communications.

Control software now embeds reinforcement-learning agents that optimize gain schedules under turbulent conditions, reducing overshoot while preserving bandwidth. Frequency-based data-driven controllers, tested on SPHERE's SAXO+ upgrade, safeguard system stability through convex optimization. Suppliers bundle AI-ready firmware within modular hardware, shortening development cycles for integrators. As predictive control proliferates, the adaptive optics market size for control platforms is forecast to capture a larger revenue slice through 2030.

Defense & Security held 31.4% revenue share in 2024, underpinned by DoD programs that depend on adaptive optics to maintain laser-beam coherence. Government purchases remain sizable, but the fastest growth comes from Consumer Electronics, which will advance at 32.50% CAGR as AR/VR headsets and smartphone cameras require compact wavefront modulators. Apple's head-mounted displays have popularized high-pixel-density micro-OLED panels that rely on adaptive optics testing during fabrication.

Industrial Manufacturing leverages MEMS mirrors in semiconductor metrology lines, with inspection stations measuring sub-nanometer deviations. Medical & Life Sciences gain momentum from cellular-level retinal diagnosis platforms, further diversifying the adaptive optics market. Research & Academia continue to pioneer innovations such as metasurface-based wavefront sensors, ensuring a steady pipeline of intellectual property.

The Adaptive Optics Market Report is Segmented by Component (Wavefront Sensors, Deformable Mirrors, and More), End-User (Defense, Medical, Industrial, Consumer Electronics, and More), Application (Astronomy, Ophthalmology, Laser Communication, Semiconductor, AR/VR, and More), Technology (MEMS DMs, Piezoelectric DMs, LC SLMs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 37.9% of 2024 revenue, anchored by the DoD's billion-dollar directed-energy budget and NASA laser-communications initiatives. Suppliers such as Northrop Grumman's Xinetics deliver lead-magnesium-niobate deformable mirrors for multiple military branches. The Space Development Agency integrates adaptive mirrors into satellite cross-links within its USD 35 billion architecture program. Canadian research on atmospheric distortion complements United States programs, jointly reinforcing the North American adaptive optics market.

Asia-Pacific is the fastest-growing region at 30.80% CAGR as Japan's Space Strategy Fund stimulates launch-vehicle and constellation programs, and China expands optical payloads for space-situational-awareness satellites. China's remote-sensing sector is projected to escalate toward USD 55-68 billion by 2033, magnifying demand for precision optics. JAXA's XRISM mission validates soft-X-ray sensors that depend on adaptive mirrors, illustrating regional competence in space-borne instrumentation.

Europe's large-aperture telescopes and defense research consortia drive sustained orders. ESO's procurements for the ELT secure long-term contracts for continental suppliers. South America and the Middle East & Africa are nascent but promising as local space programs mature, yet limited technical talent and capital budgets slow adoption relative to leading regions. Collectively, these dynamics keep the adaptive optics market on a multi-regional growth path without over-reliance on a single geography.

- Northrop Grumman Corp. (AOA Xinetics)

- Thorlabs Inc.

- Boston Micromachines Corp.

- ALPAO SAS

- Imagine Optics SA

- Flexible Optical B.V.

- Iris AO Inc.

- Phasics SA

- CILAS (ArianeGroup)

- Active Optical Systems

- Optos Plc

- AKA Optics SAS

- Trex Enterprises Corp.

- MKS Instruments Inc. (Newport)

- HOLOEYE Photonics AG

- Jenoptik AG

- Teledyne e2v

- Wavefront Dynamics LLC

- Physik Instrumente (PI) GmbH

- Sacher Lasertechnik GmbH

- Ophir Optronics Solutions Ltd.

- First Light Imaging SAS

- OptoCraft GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging in North America

- 4.2.2 Deployment in Directed-Energy and Free-Space Laser Communication Programs by U.S. DoD

- 4.2.3 Large-Aperture Telescope Upgrades (ELT, TMT) Accelerating Demand in Europe

- 4.2.4 Commercial Semiconductor Wafer and EUV Mask Inspection Requiring Sub-Nanometer Precision

- 4.2.5 Emergence of AR/VR Waveguide Display Manufacturing Using AO-Enhanced Metrology

- 4.2.6 National Space Agencies Funding for Space Debris Tracking (Asia and Middle East)

- 4.3 Market Restraints

- 4.3.1 High CapEx of High-Actuator Deformable Mirrors Limiting Wider Industrial Adoption

- 4.3.2 Complex Closed-Loop Design and Calibration Skills Gap in Emerging Markets

- 4.3.3 Long Qualification Cycles for AO-Enabled Optical Payloads in Defense Sector

- 4.3.4 Miniaturization Challenges for Consumer-Grade Modules (less than 5 mm Aperture)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Wavefront Sensors

- 5.1.2 Deformable Mirrors

- 5.1.3 Control Systems and Software

- 5.1.4 Others (Beam Expanders, Tip-Tilt Mirrors)

- 5.2 By End-User Industry

- 5.2.1 Defense and Security

- 5.2.2 Medical and Life Sciences

- 5.2.3 Industrial Manufacturing

- 5.2.4 Consumer Electronics Brands and OEMs

- 5.2.5 Research and Academia

- 5.2.6 Other End-Users

- 5.3 By Application

- 5.3.1 Astronomy and Space Observation

- 5.3.2 Ophthalmology / Retinal Imaging

- 5.3.3 Laser Communication and Directed Energy

- 5.3.4 Semiconductor Inspection and Metrology

- 5.3.5 AR/VR Optical Testing

- 5.3.6 Others (Microscopy, Free-Space Optics RandD)

- 5.4 By Technology

- 5.4.1 MEMS-Based Deformable Mirrors

- 5.4.2 Piezoelectric (PZT) Deformable Mirrors

- 5.4.3 Liquid-Crystal Spatial Light Modulators

- 5.4.4 Magnetic / Voice-Coil Mirrors

- 5.4.5 Others (Hybrid and Novel Actuation)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Gulf Co-operation Council (GCC) Countries

- 5.5.5.2 Turkey

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Northrop Grumman Corp. (AOA Xinetics)

- 6.4.2 Thorlabs Inc.

- 6.4.3 Boston Micromachines Corp.

- 6.4.4 ALPAO SAS

- 6.4.5 Imagine Optics SA

- 6.4.6 Flexible Optical B.V.

- 6.4.7 Iris AO Inc.

- 6.4.8 Phasics SA

- 6.4.9 CILAS (ArianeGroup)

- 6.4.10 Active Optical Systems

- 6.4.11 Optos Plc

- 6.4.12 AKA Optics SAS

- 6.4.13 Trex Enterprises Corp.

- 6.4.14 MKS Instruments Inc. (Newport)

- 6.4.15 HOLOEYE Photonics AG

- 6.4.16 Jenoptik AG

- 6.4.17 Teledyne e2v

- 6.4.18 Wavefront Dynamics LLC

- 6.4.19 Physik Instrumente (PI) GmbH

- 6.4.20 Sacher Lasertechnik GmbH

- 6.4.21 Ophir Optronics Solutions Ltd.

- 6.4.22 First Light Imaging SAS

- 6.4.23 OptoCraft GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment