PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846271

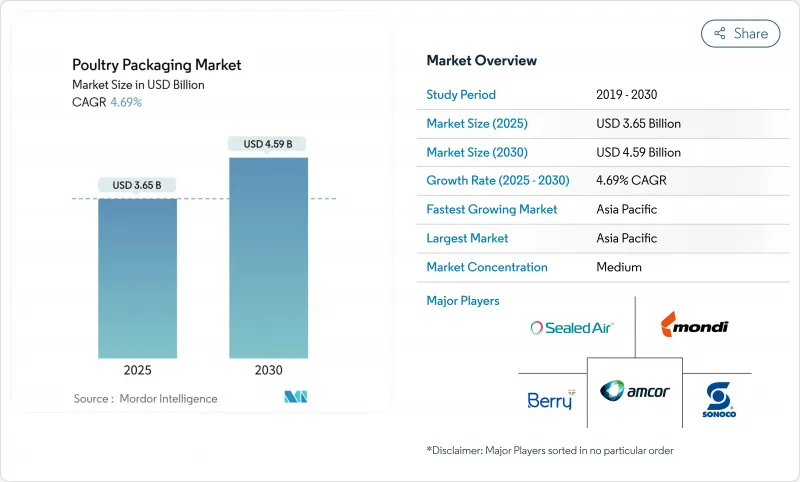

Poultry Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The poultry packaging market reached USD 3.65 billion in 2025 and is expected to achieve USD 4.59 billion by 2030, advancing at a 4.69% CAGR.

Rising demand for case-ready poultry, new modified-atmosphere solutions, and sustainability regulations underpin this steady growth. Retailers prefer shelf-stable chicken trays that reduce shrink and labor. E-commerce adds volume for insulated formats that survive multi-day transit. Material shifts toward paper-based laminates press producers to innovate barrier layers without losing throughput. Meanwhile, merger activity is altering bargaining power between converters and processors, and technology firms are embedding sensors that warn of temperature abuse at every link in the chain.

Global Poultry Packaging Market Trends and Insights

Rising Demand for Convenience and Case-Ready Poultry

Millennial and Generation Z shoppers favor quick, no-mess poultry meals that arrive in easy-peel trays or ovenable pouches. Large retailers therefore specify centralized case-ready programs that cut in-store labor and improve product consistency. Tray producers now integrate absorbent pads and gas-flush valves that extend freshness by several days. Equipment vendors such as G.Mondini supply modular lines that blend precise portioning with lower film gauge, trimming material use without sacrificing visual appeal. Foodservice chains mirror this shift by ordering pre-marinated, vacuum-skin packs that move from cooler to grill in one step. Premium meal-kit platforms exploit the same packaging to boost shelf life during shipping, capturing higher margins that offset advanced film costs.

Surge in MAP and Vacuum-Skin Technologies

Modified-atmosphere packaging improves shelf life by slowing microbial growth, yet early high-oxygen blends accelerated lipid oxidation and color shifts. Converters now trial carbon-monoxide adjuncts that stabilize bloom without raising safety concerns. Vacuum-skin films from firms like Duropac prevent purge and withstand puncture, making them attractive for bone-in cuts. Plasma-treated trays that create in-pack ozone cut Campylobacter by 90% and Salmonella by 60% without chemicals. Equipment makers such as MULTIVAC pair MAP valves with micro-perforated lids so processors can tune gas ratios to each SKU.

Avian-Influenza Supply Disruptions

The 2024-2025 HPAI wave removed millions of birds from supply chains, unsettling production schedules and altering tray demand by weight class. USDA spent USD 1.8 billion on indemnities, but barns need up to 24 weeks to repopulate, prolonging volume instability. Rapid biosensors from Washington University now detect H5N1 in five minutes, enabling earlier lockdowns and targeted culls. Shorter flock cycles force processors to order more flexible sizes and adjust brand mix, which in turn influences run-length planning for converters.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Bio-Based and Recyclable Materials

- E-Commerce Cold-Chain Expansion

- Stringent Food-Contact Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The chicken category owns 65.89% of the poultry packaging market, thanks to broad consumer acceptance and streamlined deboning lines. High throughput lets processors negotiate film cost and spur experimentation with peel-reseal lids that cut food waste. Duck, despite its modest base, grows at a 5.61% CAGR as upscale retailers introduce portion-controlled breasts in sleek vacuum-skin trays. Here, the poultry packaging market size for duck is forecast to climb steadily as exotic proteins move into mainstream freezers. Enhanced barrier bags from Amcor prevent grease migration and preserve dark-meat color, meeting premium presentation standards.

Duck's rise compels converters to integrate oil-resistant coatings while keeping clarity for retail appeal. Automation now portions duck to weight specs, enabling case-ready rollouts similar to chicken. Turkey holds share through seasonal whole-bird formats, yet value-added roasts and sliced deli packs sustain year-round demand. Each protein therefore demands tailored barrier, puncture strength, and silhouette, nudging film suppliers to broaden portfolios without inflating SKU count.

Flexible structures delivered 62.93% of the poultry packaging market in 2024, supported by lower material intensity and high graphics that elevate shelf presence. The format will remain the growth leader, advancing 5.39% each year as mono-PET and PE laminates become store-drop recyclable. Within the poultry packaging market size, rigid trays retain roles in premium oven-ready SKUs and whole-bird presentations that benefit from stacking stability.

Equipment such as GEA's PowerPak 1000 lets mid-scale plants swing between vacuum, MAP, and skin variants on a single frame, cutting change-over downtime . Flexible pouches now embed freshness sensors that change color when pH rises, turning the wrapper into a quality monitor. These upgrades defend price points in a cost-sensitive protein category and satisfy retailers that push for longer coded life to lower shrink.

The Poultry Packaging Market Report is Segmented by Meat Type (Chicken, Turkey, Duck), Packaging Format (Fixed/Rigid, Flexible), Packaging Material (Plastics, Paper and Paperboard, Metals), Packaging Technology (Modified Atmosphere Packaging, Vacuum Skin Packaging, and More), Distribution Channel (Retail, Foodservice/HORECA, Industrial and Institutional), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 38.71% of the poultry packaging market in 2024 and is projected to expand at a 5.24% CAGR to 2030. Rapid urban migration and rising disposable income in China and India lift chilled-poultry demand, while Thailand strengthens its export position. National circular-economy rules spur adoption of recyclable laminates, and local processors engage global machinery firms to meet export hygiene codes. Multinational retailers entering Indonesia and Vietnam specify case-ready programs, unlocking new business for regional converters.

North America ranks second in value. Federal regulation remains stable, but states such as California and Oregon add producer-responsibility fees that reward mono-material formats . Consumers display strong willingness to pay for antibiotic-free and sustainability-certified packs, encouraging brands to pilot compostable trays. Canada's updated Zero Plastic Waste agenda echoes EU targets, further accelerating the shift to paper-polymer hybrids. Intelligent labels see early uptake as big-box stores test on-pack QR codes for traceability.

Europe shows low headline growth yet high innovation density. Regulation 2025/40 enforces 100% recyclability by 2030 and bans PFAS, forcing converters into rapid material substitution. Retailers collaborate with suppliers to validate fully fiber trays that keep poultry fresh for 21 days, exemplified by Coveris' new BarrierFresh line. Smart-sensor pilots in Germany track time-temperature abuse, delivering data that informs dynamic discounting to curb waste.

- Amcor plc

- Berry Global Group Inc.

- Mondi plc

- Sealed Air Corporation

- Sonoco Products Company

- ProAmpac Holdings LLC

- UFlex Limited

- Huhtamaki Oyj

- Winpak Ltd.

- Glenroy Inc.

- LINPAC SEALPAC International BV

- Coveris Holding SA

- Smurfit Kappa Group plc

- Klockner Pentaplast GmbH

- Cascades Inc.

- DS Smith plc

- Printpack Inc.

- Graphic Packaging Holding Company

- Innovia Films Ltd.

- Flexopack SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for convenience and case-ready poultry

- 4.2.2 Surge in MAP and vacuum-skin technologies

- 4.2.3 Shift toward bio-based and recyclable materials

- 4.2.4 E-commerce cold-chain expansion

- 4.2.5 Adoption of intelligent freshness sensors

- 4.2.6 Recycled-content mandates in key markets

- 4.3 Market Restraints

- 4.3.1 Avian-influenza supply disruptions

- 4.3.2 Stringent food-contact compliance costs

- 4.3.3 Feedstock-price volatility for polyolefins

- 4.3.4 Consumer skepticism of high-O? MAP

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Meat Type

- 5.1.1 Chicken

- 5.1.2 Turkey

- 5.1.3 Duck

- 5.2 By Packaging Format

- 5.2.1 Fixed / Rigid

- 5.2.2 Flexible

- 5.3 By Packaging Material

- 5.3.1 Plastics

- 5.3.2 Paper and Paperboard

- 5.3.3 Metals

- 5.4 By Packaging Technology

- 5.4.1 Modified Atmosphere Packaging (MAP)

- 5.4.2 Vacuum Skin Packaging (VSP)

- 5.4.3 Active and Intelligent Packaging

- 5.4.4 High-Pressure and Others

- 5.5 By Distribution Channel

- 5.5.1 Retail

- 5.5.2 Foodservice / HORECA

- 5.5.3 Industrial and Institutional

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Berry Global Group Inc.

- 6.4.3 Mondi plc

- 6.4.4 Sealed Air Corporation

- 6.4.5 Sonoco Products Company

- 6.4.6 ProAmpac Holdings LLC

- 6.4.7 UFlex Limited

- 6.4.8 Huhtamaki Oyj

- 6.4.9 Winpak Ltd.

- 6.4.10 Glenroy Inc.

- 6.4.11 LINPAC SEALPAC International BV

- 6.4.12 Coveris Holding SA

- 6.4.13 Smurfit Kappa Group plc

- 6.4.14 Klockner Pentaplast GmbH

- 6.4.15 Cascades Inc.

- 6.4.16 DS Smith plc

- 6.4.17 Printpack Inc.

- 6.4.18 Graphic Packaging Holding Company

- 6.4.19 Innovia Films Ltd.

- 6.4.20 Flexopack SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment