PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846323

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846323

Sugar-Based Excipients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

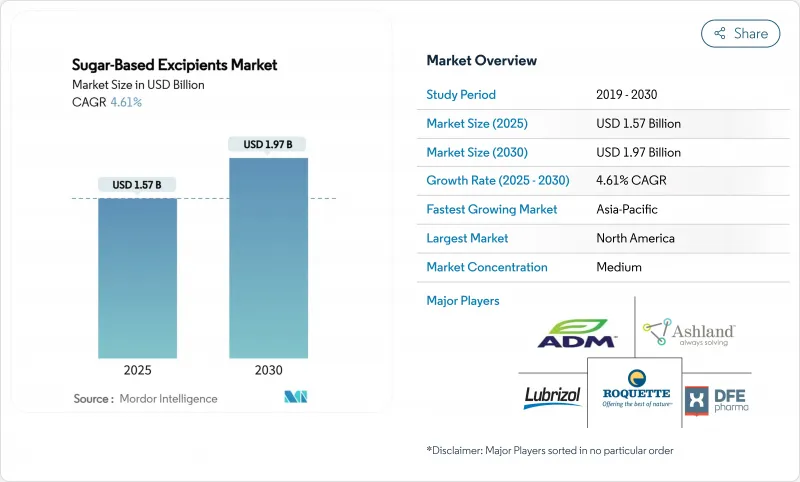

The sugar-based excipients market size is currently valued at USD 1.57 billion and is forecast to reach USD 1.97 billion by 2030, advancing at a 4.61% CAGR.

This expansion reflects rising demand for multifunctional carriers that simplify direct compression, accelerate orally disintegrating tablet (ODT) launches, and improve taste masking in pediatric and geriatric therapies. Co-processed platforms, spray-dried polyols, and 3-D-printable sugar matrices are reshaping formulation workflows while lowering manufacturing costs for generic producers. Contract development and manufacturing organizations (CDMOs) are scaling continuous direct-compression lines, further boosting adoption of sugar-derived binders and fillers. Regionally, North America retains leadership on the back of robust regulatory support, whereas Asia-Pacific registers the fastest uptake as China and India upgrade capacity for global exports. Competitive activity centers on acquisitions and joint ventures that combine excipient expertise with advanced process-analytical technologies.

Global Sugar-Based Excipients Market Trends and Insights

Increasing Use of Co-Processed Excipients

Co-processed sugars combine flowability, compressibility, and rapid dissolution in single particles that streamline direct compression and continuous manufacturing. The sugar-based excipients market is witnessing an 8.25% CAGR for these engineered blends as generic firms and CDMOs look to cut unit operations without sacrificing tablet robustness. Regulatory openness via the FDA Emerging Technology Program now shortens approval timelines for continuous direct-compression lines that rely on co-processed polyols, accelerating commercial uptake in North America and Europe.

Rapid Expansion of the Generics Industry

Generics manufacturers, which already absorb more than half of current sugar-based excipients market demand, require low-cost yet pharmacopoeia-compliant fillers to achieve bioequivalence quickly. Asian producers leverage domestic corn-based sorbitol and spray-dried mannitol to supply regional and export markets, pushing the sugar-based excipients market toward high-volume, flexible packaging formats that minimize freight and storage costs.

Stringent Multi-Jurisdictional Regulatory Requirements

Divergent pharmacopoeial standards force manufacturers to run separate stability studies and maintain duplicate documentation, inflating development timelines. Recent EU updates on allergen disclosure add further complexity, requiring sugar-based excipient suppliers to validate every lot for residual proteins and heavy metals.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Orally Disintegrating Tablet Launches

- Growing Demand for Palatable Formulations for Pediatric & Geriatric Cohorts

- Hygroscopicity-Driven Stability Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyols account for 45.51% of sugar-based excipients market share due to their favorable compressibility, low reactivity, and familiarity among regulators. Spray-dried mannitol grades enhance flow and enable higher active loading, supporting mini-tablet and ODT formats. Actual sugars exhibit stable, niche-oriented demand in syrups and medicated confectionery. Meanwhile, the sugar-based excipients market size attributed to co-processed sugars is projected to expand at an 8.25% CAGR as formulators seek single-step solutions that deliver robust hardness and rapid dissolution. Polyol-cellulose hybrids illustrate how particle engineering delivers high bulk density with minimal dusting, translating directly into faster line speeds and lower operator exposure.

Advances in continuous direct compression technology further amplify co-processed demand by allowing feeders to meter multifunctional blends without pre-mixing. Regulatory validation under the FDA Emerging Technology Program shortens paths to commercial launch, spurring investment across both originator and generic pipelines. Suppliers that secure backward integration into raw sugar streams and invest in spray-agglomeration towers are best positioned to capture this high-margin growth pocket within the sugar-based excipients market.

Direct-compression sugars hold 37.53% share of the sugar-based excipients market. Spray drying, fluid-bed agglomeration, and co-spheronization techniques continue to improve compressibility and reduce lubricant sensitivity, aligning well with continuous tablet presses that operate at speeds exceeding 250,000 tablets/hour. Powders and granules still anchor conventional wet-granulation lines, but roll-compaction adoption is rising thanks to low-hygroscopic mannitol grades that withstand high shear without capping.

Conversely, syrups and solutions log a 7.71% CAGR, reflecting the market's pivot toward patient-friendly liquid formats for pediatrics and geriatrics. Non-crystallizing sorbitol and glycerol-free maltitol solutions offer improved viscosity control and chemical stability, allowing formulators to reduce preservative loads. Single-phase aqueous concentrates simplify shipping and on-site dilution, cutting cold-chain requirements and widening access in emerging markets. This twin-track growth pattern underscores the sugar-based excipients market's versatility across both high-speed solids and value-added liquid delivery channels.

The Sugar-Based Excipients Market Report is Segmented by Product (Actual Sugar, Sugar Alcohols, and More), Form (Powders & Granules, Crystals, and More), Functional Role (Fillers and Diluents, Flavoring Agents, and More), Dosage Form (Oral Solid Dosage, and More), End User (Branded Pharmaceutical Manufacturers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 39.32% of global revenue thanks to the FDA's constructive stance on novel excipients, a deep bench of continuous manufacturing facilities, and active collaboration between academia and industry. Exclusive distribution deals, such as Univar Solutions' agreement to supply niche cellulose-based carriers, further enrich the regional portfolio. Sustainability initiatives, exemplified by carbon-neutral blister packs derived from sugar cane, show that environmental credentials are now intertwined with excipient selection.

Europe presents a mature but innovation-driven arena. Regulatory updates on allergen labeling and a possible ban on titanium dioxide spur R&D into alternative colorants and coatings, releasing fresh opportunities for calcium-enriched sugar shells. Roquette's USD 2.85 billion takeover of IFF Pharma Solutions marks the largest transaction in European excipients history, consolidating spray-dried polyol production under a single banner and signaling heightened competition in the sugar-based excipients market.

Asia-Pacific records the highest CAGR at 7.51%. China and India ramp up sorbitol and mannitol output, while South Korea and Singapore attract high-value biologics that require pharmaceutical-grade polyols as tonicity agents. Lotte Fine Chemical's USD 740 million distribution pact with Colorcon positions it as the world's largest pharmaceutical cellulose provider, underscoring the region's strategic importance. Trade agreements under the Pharmaceutical Inspection Co-operation Scheme streamline export adherence and reinforce Asia's role in the sugar-based excipients market.

- DFE Pharma

- Archer Daniels Midland

- Ashland

- Roquette

- Lubrizol

- Associated British Foods (ABITEC, SPI Pharma)

- Cargill

- Colorcon

- MEGGLE

- DuPont (IFF Pharma Solutions)

- Innophos

- BASF

- Kerry Group

- Sudzucker (BENEO)

- Tereos

- Grain Processing Corp.

- GMP Pharma

- Fuji Chemical Group

- SPI Pharma

- Huyang Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Use Of Co-Processed Excipients

- 4.2.2 Rapid Expansion Of The Generics Industry

- 4.2.3 Surge In Orally Disintegrating Tablet (ODT) Launches

- 4.2.4 Growing Demand For Palatable Formulations For Paediatric & Geriatric Cohorts

- 4.2.5 Adoption Of 3-D Printed Sugar Matrices For Personalised Dosing

- 4.2.6 FDA Novel Excipient Review Pilot Accelerating New Sugar-Based Carriers

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Jurisdictional Regulatory Requirements

- 4.3.2 Hygroscopicity-Driven Stability Challenges

- 4.3.3 Volatile Pharma-Grade Sorbitol Supply Chain

- 4.3.4 Sustainability Scrutiny Of High-Carbon Sucrose Production

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Actual Sugars

- 5.1.2 Sugar Alcohols (Polyols)

- 5.1.3 Artificial / High-Intensity Sweeteners

- 5.1.4 Co-processed Sugar Excipients

- 5.2 By Form

- 5.2.1 Powders & Granules

- 5.2.2 Direct-Compression Sugars

- 5.2.3 Crystals

- 5.2.4 Syrups & Solutions

- 5.3 By Functional Role

- 5.3.1 Fillers & Diluents

- 5.3.2 Binders

- 5.3.3 Flavoring / Sweetening Agents

- 5.3.4 Tonicity Modifiers

- 5.3.5 Coating Agents

- 5.4 By Dosage Form

- 5.4.1 Oral Solid Dosage

- 5.4.2 Oral Liquid Dosage

- 5.4.3 Topical & Others

- 5.5 By End User

- 5.5.1 Branded Pharmaceutical Manufacturers

- 5.5.2 Generic Pharmaceutical Manufacturers

- 5.5.3 Nutraceutical & Dietary-Supplement Producers

- 5.5.4 Contract Development & Manufacturing Organisations (CDMOs)

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 DFE Pharma

- 6.3.2 Archer Daniels Midland

- 6.3.3 Ashland

- 6.3.4 Roquette

- 6.3.5 Lubrizol

- 6.3.6 Associated British Foods (ABITEC, SPI Pharma)

- 6.3.7 Cargill

- 6.3.8 Colorcon

- 6.3.9 MEGGLE

- 6.3.10 DuPont (IFF Pharma Solutions)

- 6.3.11 Innophos

- 6.3.12 BASF

- 6.3.13 Kerry Group

- 6.3.14 Sudzucker (BENEO)

- 6.3.15 Tereos

- 6.3.16 Grain Processing Corp.

- 6.3.17 GMP Pharma

- 6.3.18 Fuji Chemical Group

- 6.3.19 SPI Pharma

- 6.3.20 Huyang Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment