PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848011

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848011

Non-Meat Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

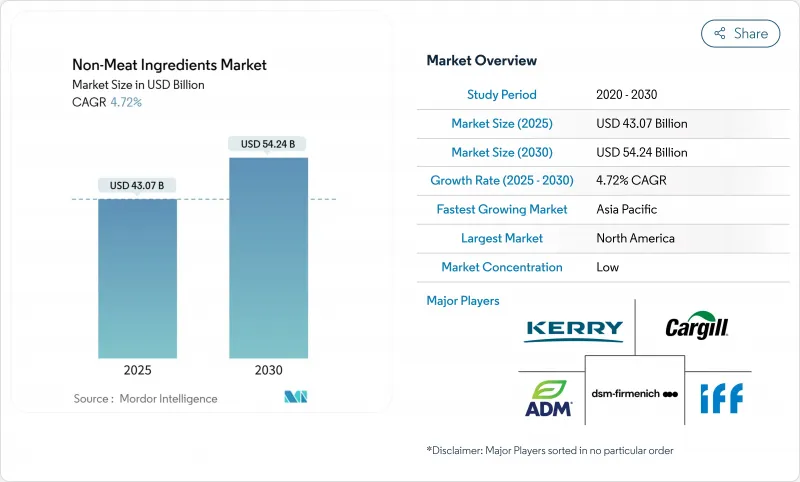

The non-meat ingredients market size is estimated to be valued at USD 43.07 billion in 2025 and is forecast to advance at a 4.72% CAGR to USD 54.24 billion by 2030.

This growth is primarily attributed to the increasing adoption of functional components designed to enhance texture, flavor, preservation, and nutritional density. Manufacturers are focusing on reformulating products to reduce input costs while maintaining sensory quality, supported by advancements in extraction and encapsulation technologies that improve ingredient performance. Furthermore, the demand is being driven by the rising preference for clean-label products, stricter safety regulations, and the expanding popularity of hybrid meat-plant offerings. Plant-derived proteins and natural preservatives, in particular, are gaining momentum as they address consumer concerns related to health and sustainability while enabling processors to comply with evolving regulatory requirements.

Global Non-Meat Ingredients Market Trends and Insights

Growing demand for processed meat products

The global processed meat market is experiencing significant growth, driven by evolving consumer preferences, urbanization, and innovations in production. Processed meat products, such as sausages, bacon, and deli meats, have become staples in developed countries, as highlighted by the USDA, while rising disposable incomes and urbanization in developing regions, as noted by UN-Habitat, are fueling demand for convenient, ready-to-eat options. Asia, which accounts for 54% of the global urban population, is projected to see its urban population grow by 1.2 billion by 2050, further amplifying this trend. Additionally, advancements in non-meat ingredients, including binders, fillers, and flavor enhancers, have enabled manufacturers to meet diverse consumer preferences while maintaining product quality and extending shelf life. Regulatory frameworks, such as the European Union's food additive standards, have also played a crucial role in promoting food safety and encouraging the adoption of advanced production techniques. These factors collectively underscore the dynamic nature of the processed meat market, where innovation and regulatory compliance are pivotal in addressing evolving consumer demands and sustaining market growth.

Requirement for extended meat product shelf life

The requirement for extended shelf life in meat products is a significant driver of the Global Non-Meat Ingredients Market. Consumers increasingly seek convenience and longer-lasting food products, prompting manufacturers to incorporate non-meat ingredients such as preservatives, stabilizers, and antioxidants to enhance shelf life. For instance, the United States Department of Agriculture (USDA) has established guidelines for the use of food additives to ensure safety and quality in processed meat products . Similarly, the European Food Safety Authority regulates the use of additives to maintain product integrity and extend shelf life. These regulatory frameworks encourage the adoption of non-meat ingredients, driving market growth. Additionally, associations like the North American Meat Institute emphasize the importance of shelf life extension to reduce food waste and meet consumer demands, further supporting the market's expansion.

High production costs of non-meat ingredients impacting product pricing and market adoption

Rising production costs for non-meat ingredients are influencing product pricing and slowing market adoption is hindering the market growth. For instance, according to the United States Department of Agriculture, the cost of plant-based proteins, a key non-meat ingredient, has been steadily increasing due to supply chain disruptions, higher raw material prices, and inflationary pressures. Moreover, the Food and Agriculture Organization (FAO) reports that the production of alternative proteins, such as pea and soy protein, is heavily impacted by fluctuating agricultural yields and climate change, leading to inconsistent supply and increased costs. These challenges are compounded by the high initial investment required for research and development (R&D) to improve the taste, texture, and nutritional profile of non-meat ingredients, which further escalates production expenses. As a result, manufacturers face difficulties in offering competitively priced products, limiting their ability to penetrate price-sensitive markets. These factors collectively hinder the widespread adoption of non-meat ingredients, particularly in emerging economies where affordability remains a critical factor for consumers.

Other drivers and restraints analyzed in the detailed report include:

- Increasing consumption of convenience foods

- Rising preference for protein-rich diets

- Short shelf life of natural non-meat ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, flavoring agents held a 33.65% share of the market, underscoring their pivotal role in meeting consumer demand for authentic taste profiles. These agents are essential for enhancing the sensory appeal of non-meat products, ensuring they deliver on taste and quality expectations. Moreover, they effectively mask vegetal undertones in hybrid products and maintain consistent flavor intensity during freeze-thaw cycles, which is critical for preserving product quality during storage and distribution. Their functionality highlights their importance as manufacturers continue to innovate to meet the evolving demands of the food industry, particularly in the context of plant-based and hybrid product development.

The preservatives sub-segment, forecasted to grow at a 6.16% CAGR, is experiencing robust demand driven by the shift toward synthetic-free and clean-label solutions. Consumers are increasingly favoring natural alternatives, prompting manufacturers to develop preservative solutions that extend shelf life while aligning with regulatory standards and consumer preferences for healthier, sustainable food options. This shift, coupled with advancements in ingredient technologies, is reshaping market dynamics. Manufacturers are prioritizing the development of high-quality, functional ingredients to cater to the diverse and growing needs of the food industry, particularly as plant-based and hybrid products gain traction.

The Non-Meat Ingredients Market is Segmented by Type (Flavoring Agents, Binders, Extenders, Fillers, Coloring Agents, Preservatives, Salt, and Others), Application (Processed and Cured Meat Products, Fresh Meat Products, and More), Source (Plant-Derived, Synthetic or Mineral-Derived, and Animal-Derived), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads the non-meat ingredients market with a 40.15% share in 2024, driven by advanced food processing infrastructure and strict regulations promoting functional ingredients. Rising health concerns about processed meats fuel demand for clean labels and natural ingredients. The U.S. leads with a focus on specialty ingredients, enhancing nutrition and sensory appeal. Canada and Mexico are expanding applications due to growing meat processing and health awareness. Innovation targets multifunctional ingredients addressing preservation, texture, and nutrition.

Europe, the second-largest market, is shaped by strict additive regulations and strong demand for clean-label products. The region leads in hybrid meat products, blending animal and plant proteins. Germany and the U.K. drive plant-based ingredient adoption, while France and Spain focus on natural preservatives and flavor enhancers. Mergers and acquisitions in the specialty ingredient sector are rising, with plant-based firms consolidating post-pandemic. This trend fosters integrated solutions for meat processing.

Asia-Pacific is projected to grow at a 7.07% CAGR from 2025-2030, driven by urbanization, rising meat consumption, and expanding food processing. China leads with investments in food technology and advanced ingredients for quality and safety, creating opportunities for suppliers of preservatives, flavor enhancers, and texture modifiers. India is emerging as a key market, with companies like Corbion expanding through acquisitions such as Novotech. South Korea drives innovation in fermentation-based functional ingredients. South America and the Middle East & Africa show steady growth, with Brazil and South Africa advancing due to expanding meat processing and rising food quality awareness.

- Archer Daniels Midland Company

- Kerry Group plc

- DSM-Firmenich

- International Flavors & Fragrances Inc.

- Ingredion Incorporated

- Associated British Foods PLC

- BASF SE

- Cargill, Incorporated

- Corbion N.V.

- Tate and Lyle PLC

- Sensient Technologies Corporation

- Kemin Industries

- Ajinomoto Inc.

- Novonesis

- Darling Ingredients

- Symrise AG

- Roquette Freres

- AGT Foods

- Florida Food products

- Givaudan S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for processed meat products

- 4.2.2 Requirement for extended meat product shelf life

- 4.2.3 Increasing consumption of convenience foods

- 4.2.4 Rising preference for protein-rich diets

- 4.2.5 Increasing demand for plant-based meat analogs

- 4.2.6 Expanding market for hybrid meat-plant products

- 4.3 Market Restraints

- 4.3.1 High production costs of non-meat ingredients impacting product pricing and market adoption

- 4.3.2 Short shelf life of natural non-meat ingredients

- 4.3.3 Technical difficulties in maintaining consistent product texture and taste

- 4.3.4 Consumer concerns about artificial additives and preservatives in processed foods

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Flavoring Agents

- 5.1.2 Binders

- 5.1.3 Extenders

- 5.1.4 Fillers

- 5.1.5 Coloring Agents

- 5.1.6 Preservatives

- 5.1.7 Salt

- 5.1.8 Others

- 5.2 Application

- 5.2.1 Processed and Cured Meat Products

- 5.2.2 Fresh Meat Products

- 5.2.3 Marinated and Seasoned Meat Products

- 5.2.4 Frozen Meat Products

- 5.2.5 Plant-Based Meat Analog Formulations

- 5.2.6 Others

- 5.3 By Source

- 5.3.1 Plant-Derived

- 5.3.2 Synthetic or Mineral-Derived

- 5.3.3 Animal-Derived

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Archer Daniels Midland Company

- 6.4.2 Kerry Group plc

- 6.4.3 DSM-Firmenich

- 6.4.4 International Flavors & Fragrances Inc.

- 6.4.5 Ingredion Incorporated

- 6.4.6 Associated British Foods PLC

- 6.4.7 BASF SE

- 6.4.8 Cargill, Incorporated

- 6.4.9 Corbion N.V.

- 6.4.10 Tate and Lyle PLC

- 6.4.11 Sensient Technologies Corporation

- 6.4.12 Kemin Industries

- 6.4.13 Ajinomoto Inc.

- 6.4.14 Novonesis

- 6.4.15 Darling Ingredients

- 6.4.16 Symrise AG

- 6.4.17 Roquette Freres

- 6.4.18 AGT Foods

- 6.4.19 Florida Food products

- 6.4.20 Givaudan S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK