PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848025

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848025

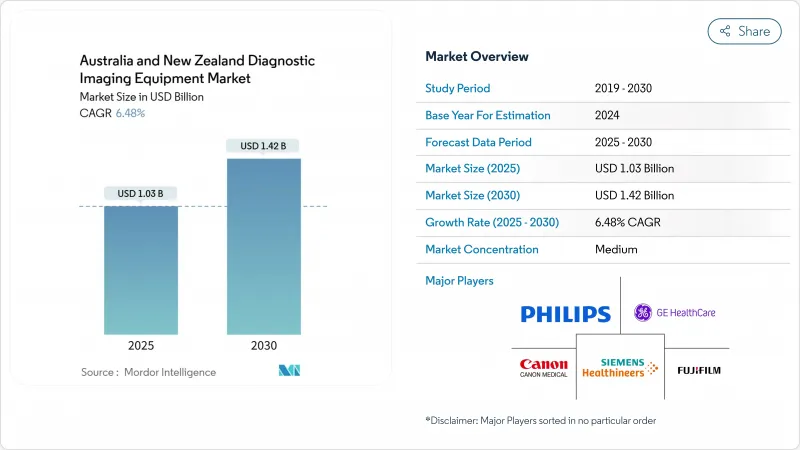

Australia And New Zealand Diagnostic Imaging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Australia and New Zealand Diagnostic Imaging Equipment Market size is estimated at USD 1.03 billion in 2025, and is expected to reach USD 1.42 billion by 2030, at a CAGR of 6.48% during the forecast period (2025-2030).

Demand scales with chronic-disease prevalence, rapid AI deployment across modalities, and record public spending on hospital infrastructure in both countries. Additional momentum comes from private-equity consolidation of imaging chains, helium-free MRI innovations that curb running costs, and teleradiology networks that extend specialist reach into sparsely populated regions. Capital-cost headwinds, sonographer shortages, and radio-isotope logistics temper growth yet are being offset by flexible finance models, national training grants, and modality-agnostic rebate reform. Overall, the Australia & New Zealand diagnostic imaging equipment market continues to benefit from synchronized policy, technology, and investment cycles that favor sustained equipment renewal and fleet expansion.

Australia And New Zealand Diagnostic Imaging Equipment Market Trends and Insights

Rise in Prevalence of Chronic Diseases

Cardiovascular disease and cancer remain leading death drivers, keeping demand for routine multimodal scans high. Indigenous Australians lose nearly 240,000 healthy life-years annually from illness, prompting targeted imaging subsidies in underserved regions. New Zealand expects cancer diagnoses to touch 25,000 a year, boosting need for oncology PET-CT capacity. Vendors now bundle AI triage engines such as GE HealthCare's CareIntellect to accelerate report delivery for complex oncology pathways. National health data agencies standardize coding to track chronic-disease imaging volumes, supporting predictable equipment upgrades.

Growing Geriatric Population

Australia's over-65 cohort expands by roughly 3.3% annually, raising incidences of osteoporotic fractures and neurodegenerative disorders that demand age-adapted imaging. Policy frameworks under the National Medical Workforce Strategy address geographic maldistribution that leaves rural elderly communities short of radiology services. New Zealand's Te Whatu Ora implements facility modernization so older adults access MRI and CT on-site rather than traveling long distances. Helium-free MRI such as Siemens MAGNETOM Flow reduces cryogen dependency while incorporating mood-lighting and noise dampening, addressing comfort concerns for elderly scans. Virtual-care megatrends project remote check-ins with integrated image sharing, shrinking repeat hospital visits for seniors.

Capital Cost of Advanced Modalities

High capital expenditure requirements for next-generation imaging systems create procurement barriers, particularly for smaller healthcare facilities. High-end 3 T MRI or spectral CT can exceed USD 3 million per unit, a threshold that strains district hospitals. Vendor finance packages and leasing are expanding yet smaller New Zealand sites still delay upgrades until depreciation schedules end. Australia's equipment-lifespan rules grant exemptions for early replacement if efficiency gains are proven, encouraging helium-free swaps. Regulatory compliance costs add complexity, with TGA application audit updates focusing on high-risk devices requiring comprehensive documentation for conformity assessments.

Other drivers and restraints analyzed in the detailed report include:

- Increased Adoption of Advanced Imaging Technologies

- Private-Sector Centre Consolidation

- Workforce Shortage of Sonographers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Computed tomography posted the quickest 7.97% CAGR, helping the Australia & New Zealand diagnostic imaging equipment market diversify beyond ultrasound leadership. The CT upswing aligns with bedside units such as Siemens SOMATOM On.site that bring neuro imaging directly to intensive-care beds. Ultrasound remains indispensable across obstetrics, emergency, and primary-care pathways because of portability and cost advantages. MRI growth benefits from helium-free magnet launches that trim life-cycle costs by up to 30%. X-ray systems have moved toward flat-panel detectors and smart workflow guidance, while fluoroscopy platforms integrate AI dose-optimization. Nuclear imaging's progress hinges on isotope supply, yet PET-CT retains niche strength in oncology staging backed by rebate increases. Mammography manufacturers add short scan times and AI lesion triage to meet breast-screen mandates. Together these upgrades sustain a healthy replacement cycle that underpins modality-level revenue expansion inside the Australia & New Zealand diagnostic imaging equipment market.

The segment's technology race fosters multi-vendor AI ecosystems where algorithms from local firms like Harrison.ai can be deployed across Canon, GE, or Philips hardware. Vendor neutrality helps private imaging chains standardize analytics fleetwide. As reimbursement now rewards quality metrics instead of raw throughput, software that cuts repeat scans or accelerates diagnosis holds commercial upside. This environment keeps CT and MRI demand resilient even when capital budgets tighten. The Australia & New Zealand diagnostic imaging equipment industry therefore witnesses continuous modality innovation that aligns clinical outcomes with cost-containment goals.

Fixed rooms still represent 81.84% revenue thanks to comprehensive capabilities, yet mobile and handheld devices are starting to reshape workflows within the Australia & New Zealand diagnostic imaging equipment market. Handheld ultrasound alone recorded more than 2,600 emergency-department scans across regional hospitals with 94% diagnostic utility. Mobile CT and MRI reduce patient transfers, lowering in-hospital complication risk. Rural outreach programs leverage truck-mounted magnet units, creating new capital-leasing opportunities for vendors.

Rising point-of-care adoption also reflects clinician demand for real-time triage in primary settings. Artificial intelligence embedded in devices like Philips Lumify automates measurement tasks, which broadens user segments beyond specialist radiologists. Regulatory authorities now provide accelerated routes for low-risk portable devices, shortening time to market. Collectively, these forces push portability CAGR to 7.12%, reinforcing the decentralization trend that drives incremental equipment sales across the Australia & New Zealand diagnostic imaging equipment market.

The Australia and New Zealand Diagnostic Imaging Equipment Market Report is Segmented by Modality (MRI, Computed Tomography (CT), Ultrasound, and More), Portability (Fixed Systems, Mobile and Hand-Held Systems), Application (Cardiology, Oncology, Neurology, and More), End User (Hospitals, Diagnostic Imaging Centres, Other End-Users), and Geography (Australia, New Zealand). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens Healthineers

- GE Healthcare

- Koninklijke Philips

- Canon Medical Systems Corp

- Fujifilm Holdings Corp

- Hologic

- Mindray Bio-Medical Electronics

- Carestream Health

- Agfa-Gevaert

- Hitachi Healthcare

- Shimadzu Corp

- Samsung Group

- Esaote

- United Imaging Healthcare

- Telix Pharmaceuticals

- Clarity Pharmaceuticals

- ANSTO

- Lumus Imaging (Healius)

- Integral Diagnostics

- Sonic Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Prevalence of Chronic Diseases

- 4.2.2 Growing Geriatric Population

- 4.2.3 Increased Adoption of Advanced Imaging Technologies

- 4.2.4 Private-Sector Centre Consolidation

- 4.2.5 Growth of Teleradiology in Remote Areas

- 4.2.6 Government Initiatives with Respect to Diagnostics

- 4.3 Market Restraints

- 4.3.1 Capital Cost of Advanced Modalities

- 4.3.2 Workforce Shortage of Sonographers

- 4.3.3 Helium Supply Volatility for MRI

- 4.3.4 Radio-Isotope Waste-disposal Rules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Modality

- 5.1.1 MRI

- 5.1.2 Computed Tomography (CT)

- 5.1.3 Ultrasound

- 5.1.4 X-ray

- 5.1.5 Nuclear Imaging (SPECT / PET)

- 5.1.6 Fluoroscopy

- 5.1.7 Mammography

- 5.2 By Portability

- 5.2.1 Fixed Systems

- 5.2.2 Mobile and Hand-held Systems

- 5.3 By Application

- 5.3.1 Cardiology

- 5.3.2 Oncology

- 5.3.3 Neurology

- 5.3.4 Orthopedics

- 5.3.5 Gastroenterology

- 5.3.6 Gynecology

- 5.3.7 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centres

- 5.4.3 Other End-users

- 5.5 By Geography

- 5.5.1 Australia

- 5.5.2 New Zealand

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Siemens Healthineers AG

- 6.3.2 GE HealthCare

- 6.3.3 Koninklijke Philips N.V.

- 6.3.4 Canon Medical Systems Corp

- 6.3.5 Fujifilm Holdings Corp

- 6.3.6 Hologic Inc

- 6.3.7 Mindray Bio-Medical Electronics

- 6.3.8 Carestream Health

- 6.3.9 Agfa-Gevaert Group

- 6.3.10 Hitachi Healthcare

- 6.3.11 Shimadzu Corp

- 6.3.12 Samsung Medison

- 6.3.13 Esaote SpA

- 6.3.14 United Imaging

- 6.3.15 Telix Pharmaceuticals

- 6.3.16 Clarity Pharmaceuticals

- 6.3.17 ANSTO

- 6.3.18 Lumus Imaging (Healius)

- 6.3.19 Integral Diagnostics

- 6.3.20 Sonic Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment