PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848093

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848093

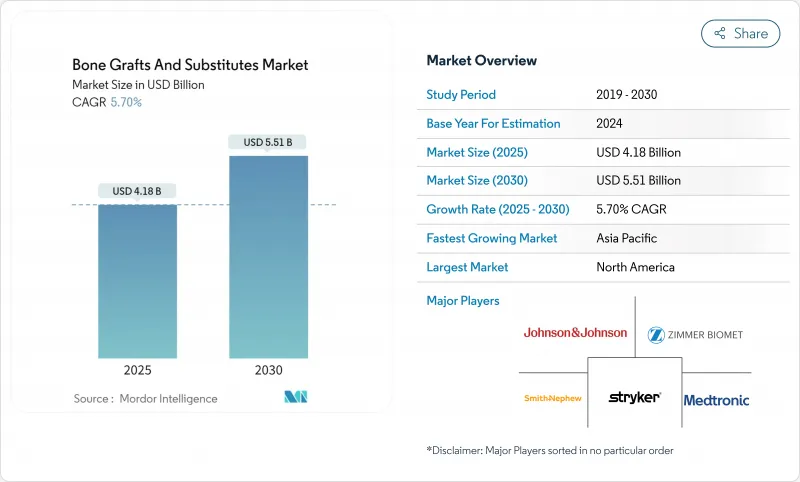

Bone Grafts And Substitutes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The bone graft substitutes market size reached USD 4.18 billion in 2025 and is forecast to climb to USD 5.51 billion by 2030, reflecting a 5.70% CAGR over the period.

Rapid progress in nanoscale 3-D printing, breakthroughs in bioactive glass and calcium-phosphate ceramics, and wider acceptance of cell-based matrices are shifting surgeon preference away from traditional autografts toward precision-engineered alternatives. Procedure volumes in spinal fusion and joint reconstruction continue expanding, with minimally invasive techniques enabling earlier interventions that drive steady product demand. Regulatory support is also accelerating innovation; FDA breakthrough designations awarded to new grafts shorten commercialization timelines while signaling clinical value. Industry participants layer competitive advantages around proprietary surface technologies, porous architectures, and patient-specific design-all aimed at faster fusion, lower complication rates, and more predictable healing.

Global Bone Grafts And Substitutes Market Trends and Insights

Increasing Spinal-Fusion & Joint-Reconstruction Volumes

Posterior cervical fusions for deformity grew at a 16.5% CAGR versus 9.7% for standard cases, confirming surgeon confidence to tackle complex anatomy with modern implants. ASCs expect orthopedic outpatient cases to climb 13% this decade, making rapid-setting grafts essential to same-day discharge targets. High throughput combined with heightened complexity shifts purchasing toward bone graft substitutes that reduce harvest-site morbidity, shorten operating time, and integrate seamlessly with interbody cages. Surgeons increasingly treat graft substitutes not as secondary fillers but as frontline enablers of workflow efficiency and enhanced patient recovery.

Rising Geriatric Population with Osteoporosis & Trauma Risk

Projected lower-limb arthroplasties in Colombia illustrate global momentum, rising to 39,270 procedures by 2050 at a 5.54% CAGR, driven primarily by aging female cohorts. Elderly patients present diminished osteogenic capacity and higher infection risk, raising the bar for graft bioactivity and antimicrobial performance. Medicare joint-arthroplasty reimbursements slid substantially from 2013 to 2021 despite higher beneficiary counts, forcing health systems to prioritize cost-effective grafts that outperform autografts without inflating episode costs, according to a September 2024 analysis of the Medicare Part B database published in the Journal of Orthopaedic Experience & Innovation Journal of Orthopaedic Experience & Innovation.

Calcium-doped titanium surfaces show promise in minimizing infection by modulating fibrinogen adsorption and bacterial adherence, which is vital in older populations with compromised immunity. Together these demographic and clinical pressures propel demand for bone graft substitutes that pair osteoinductivity with robust antimicrobial defenses.

High Cost & Patchy Reimbursement for Premium Grafts

Basic synthetic materials cost USD 46.2-140, while premium grafts exceed reimbursement caps, leading facilities to limit use to complex cases. Coverage for stem-cell-enhanced products remains conditional, intensifying uncertainty for innovators navigating evidence-based reimbursement hurdles. Regional variability compounds the issue; U.S. Northeast saw the steepest payment declines despite the highest baseline rates, underscoring geographic inconsistency in economic viability.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Synthetic & Cell-Based Matrices

- 3-D Printed, Patient-Specific Scaffolds Enable Complex Reconstructions

- Disease-Transmission / Immune-Response Risk with Allo- & Xenografts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Allografts captured the largest slice of bone graft substitutes market share at 42.67% in 2024, supported by clinician familiarity and strong osteoinductive profiles. Hospitals value their supply predictability, while tissue banks refine processing to safeguard biologic potency and viral safety. The bone graft substitutes market size for allografts is projected to rise steadily, propelled by fiber-based demineralized matrices that deliver improved handling and minimal donor-site morbidity. Synthetic grafts are closing the gap through nano-engineered surfaces and controlled degradation, and cell-based matrices post the fastest growth as regulatory clarity improves.

Competitive dynamics center on differentiation by specific procedure. Xenografts hold niche traction in dental indications that benefit from non-resorbable properties. Novel non-resorbable allografts extend longevity, easing revision anxiety in load-bearing zones. Cryopreserved viable bone matrices target premium clinical segments after Enovis and Ossium Health linked distribution reach with biologic innovation. Each product category therefore positions itself around a discrete clinical need set-safety, biological potency, or ease of use.

Calcium-phosphate ceramics represented 44.34% of bone graft substitutes market share in 2024 thanks to predictable biocompatibility and established regulatory paths. Advances in porosity tuning and silicon doping improve mechanical strength while accelerating osseointegration. The bone graft substitutes market size attached to bioactive glass grows fastest as newer formulations manage degradation kinetics and heighten osteostimulation. Polymer-based options remain in early adoption, valued for elasticity and drug-release potential in trauma settings. Composite matrices combining hydroxyapatite and collagen now rival iliac crest graft fusion rates while eliminating harvest pain. Supply reliability also shapes material selection; calcium sulfate modifications attempt to slow resorption without sacrificing structural integrity.

The Bone Grafts and Substitutes Market Report is Segmented by Product (Allografts, Bone Graft Substitutes, and Other Products), Application (Craniomaxillofacial, Dental, Joint Reconstruction, Spinal Fusion, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers Market Sizes and Forecasts in Terms of Value (USD) for all the Abovementioned Segments.

Geography Analysis

North America held 42.23% share in 2024, anchored by high procedure volumes, broad insurance coverage, and high surgeon comfort with premium products. Posterior cervical fusions for deformity continue to outpace other segments, underscoring demand for grafts that perform in challenging biomechanics. FDA breakthrough programs, such as Renovos's gel, channel innovation swiftly into operating rooms.

Europe stands second, characterized by rigorous evidence requirements and a penchant for ceramic and composite solutions. Germany and the United Kingdom invest heavily in biomaterials research, seeding a pipeline of glass-ceramic hybrids with controlled degradation profiles. Southern Europe's aging demographics sustain demand even as cost containment exerts downward price pressure.

Asia-Pacific records the fastest CAGR at 7.24%, driven by China's hospital expansion, India's burgeoning medical tourism, and Japan's super-aged populace. Governments increase orthopedic funding, while local manufacturers scale additive-manufacturing capacity to lower import dependency. Wider insurance penetration and surgeon training programs further lift adoption of next-generation bone graft substitutes.

List of Companies Covered in this Report:

- Medtronic

- Stryker

- Johnson & Johnson

- Zimmer Biomet

- Baxter International Inc. (Advanced Surgery)

- Integra LifeSciences Holdings Corp.

- Orthofix

- NuVasive

- Smith+Nephew plc

- RTI Surgical

- Geistlich Pharma

- Dentsply Sirona

- Biocomposites Ltd.

- Straumann Group

- Collagen Matrix

- SeaSpine Holdings Corp.

- Kuros Biosciences AG

- OsteoMed LLC

- AlloSource Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing spinal-fusion & joint-reconstruction volumes

- 4.2.2 Rising geriatric population with osteoporosis & trauma risk

- 4.2.3 Technological advances in synthetic & cell-based matrices

- 4.2.4 Shift from autografts to off-the-shelf substitutes

- 4.2.5 3-D printed, patient-specific scaffolds enable complex reconstructions

- 4.2.6 Ambulatory-surgery-center demand for minimally-invasive delivery kits

- 4.3 Market Restraints

- 4.3.1 High cost & patchy reimbursement for premium grafts

- 4.3.2 Disease-transmission / immune-response risk with allo- & xenografts

- 4.3.3 Medical-grade calcium-phosphate supply bottlenecks

- 4.3.4 Nano-ceramic-particle inflammation triggering tougher regulation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Allografts

- 5.1.2 Synthetic Bone Grafts

- 5.1.3 Demineralized Bone Matrix (DBM)

- 5.1.4 Cell-based Matrices

- 5.1.5 Xenografts

- 5.2 By Material

- 5.2.1 Calcium-phosphate ceramics

- 5.2.2 Bioactive glass

- 5.2.3 Polymer-based grafts

- 5.2.4 Composite materials

- 5.3 By Application

- 5.3.1 Spinal Fusion

- 5.3.2 Trauma & Craniomaxillofacial

- 5.3.3 Joint Reconstruction

- 5.3.4 Dental Bone Grafting

- 5.3.5 Foot & Ankle

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Dental Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Stryker Corporation

- 6.3.3 Johnson & Johnson (DePuy Synthes)

- 6.3.4 Zimmer Biomet Holdings Inc.

- 6.3.5 Baxter International Inc. (Advanced Surgery)

- 6.3.6 Integra LifeSciences Holdings Corp.

- 6.3.7 Orthofix Medical Inc.

- 6.3.8 NuVasive Inc.

- 6.3.9 Smith+Nephew plc

- 6.3.10 RTI Surgical Inc.

- 6.3.11 Geistlich Pharma AG

- 6.3.12 Dentsply Sirona Inc.

- 6.3.13 Biocomposites Ltd.

- 6.3.14 Institut Straumann AG

- 6.3.15 Collagen Matrix Inc.

- 6.3.16 SeaSpine Holdings Corp.

- 6.3.17 Kuros Biosciences AG

- 6.3.18 OsteoMed LLC

- 6.3.19 AlloSource Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment