PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848106

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848106

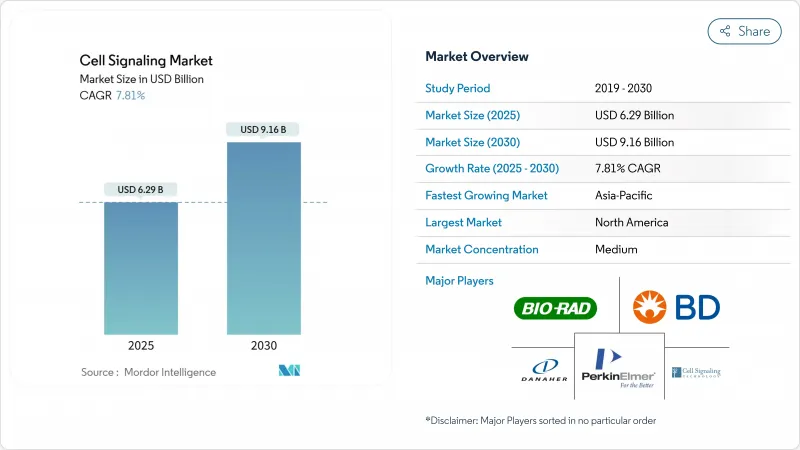

Cell Signaling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cell signaling market size is valued at USD 6.29 billion in 2025 and is forecast to reach USD 9.16 billion by 2030, advancing at a 7.81% CAGR.

Growth rests on sustained capital spending for automated flow cytometers, mass spectrometers and multiplex imaging systems that generate richer cellular data with fewer manual steps. North America retains leadership on the back of generous National Institutes of Health (NIH) grants and a receptive regulatory climate, while Asia-Pacific posts the fastest gains as Japan, South Korea and China expand single-use bioreactor capacity for clinical-grade cell and gene therapies. Momentum is reinforced by the U.S. Food and Drug Administration's (FDA) 2024 clearance of Ryoncil, the first allogeneic mesenchymal stromal cell product for steroid-refractory acute graft-versus-host disease, which signals wider acceptance of cell-based interventions. Leading suppliers are sharpening artificial-intelligence modules that cut assay-development cycles and improve reagent selection, thereby raising entry barriers for smaller competitors.

Global Cell Signaling Market Trends and Insights

Growing Prevalence of Chronic and Autoimmune Diseases

The rising incidence of chronic and autoimmune disorders is redirecting capital toward modular lipid-nanoparticle platforms that generate CAR-T cells in vivo, eliminating lengthy ex-vivo manufacturing. Mesenchymal stromal cell (MSC) transplantation continues to produce compelling remission rates across rheumatoid arthritis and systemic sclerosis, fueling wider payer acceptance. As aging populations swell in high-income economies, regenerative medicine trials targeting joint degeneration and metabolic syndrome further accelerate demand for advanced pathway analyses and functional-immune readouts.

Expanding Funding for Cell-Based Life-Science Research

Thermo Fisher Scientific is investing USD 2 billion over four years-USD 500 million earmarked for R&D-to anchor U.S. production of high-impact analytical systems, a move mirroring similar manufacturing onshoring initiatives by rivals. In parallel, Orionis Biosciences secured USD 105 million upfront from Genentech for molecular-glue programs, underscoring venture appetite for next-generation modality platforms. Across Asia-Pacific, sovereign wealth funds have started funneling capital into cell-therapy process-development hubs, compressing technology-transfer timelines for local biologics manufacturers.

High Capital Investment Required for Advanced Cell-Signaling Systems

Turn-key spectral cytometers exceed USD 750,000 per unit, stretching academic grant cycles and delaying upgrades in lower-income regions. Therapeutic-grade monoclonal antibody production still costs between USD 15,000 and USD 140,000 annually for a single indication, which inflates downstream consumable budgets. Contract manufacturing organizations report sub-50% utilization rates, revealing a supply-demand mismatch that exacerbates cost-recovery challenges for platform owners.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Technological Innovations in Cell-Analysis Platforms

- Increasing Adoption of Artificial Intelligence in Assay Design

- Ethical and Regulatory Concerns Surrounding Stem-Cell Research

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endocrine signaling held 34.76% of the cell signaling market in 2024, underpinning metabolic and reproductive studies that require hormone-receptor assays at organ scale. Autocrine signaling is on track for the fastest 8.9% CAGR because oncology programs increasingly dissect self-stimulating loops that govern tumor proliferation. Paracrine signaling retains relevance for tissue-repair models, while synaptic mechanisms benefit from higher neuroscience funding.

Growing mechanistic clarity around autocrine feedback has spurred design of pathway-selective inhibitors and companion diagnostics. Paracrine insights have inspired nanoparticle carriers programmed to home lymph-node chemokine gradients, an approach now in mid-phase breast-cancer trials. Together, these advances keep the cell signaling market firmly focused on translating pathway biology into precision therapeutics.

Instruments accounted for 55.67% of 2024 revenue, reflecting the hefty ticket price of analytical workstations that constitute the core lab infrastructure. Consumables, however, are poised to outpace with a 9.6% CAGR as recurring reagent orders scale with assay volume. Flow-cytometry skids, high-resolution imaging chips and microfluidic cartridges dominate replacement cycles, especially in decentralized CRO facilities.

Consumables demand also rises because recombinant antibodies outperform conventional polyclonal reagents on specificity, trimming reproducibility failures that previously cost U.S. labs up to USD 1.8 billion annually. Suppliers offering antibody-validation data sets gain customer stickiness and incremental margins.

The Cell Signaling Market Report is Segmented by Signaling Type (Endocrine Signaling, and More), Product (Instruments and Consumables), Technology (Flow Cytometry, Mass Spectrometry, and More), Pathway (AKT/PI3K Signaling, and More), Application (Drug Discovery & Development, and More), End User (Pharma & Biotech Companies, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.45% of global revenue in 2024, underpinned by NIH grant stability, venture capital depth and FDA guidance that shortens regulatory review for regenerative candidates. Thermo Fisher's multi-year USD 2 billion domestic build-out underscores supplier confidence in continued demand for high-throughput instrumentation. State-level legislation permitting certain unapproved stem-cell interventions introduces compliance fragmentation that large sponsors must now navigate.

Asia-Pacific leads growth at a 8.45% CAGR through 2030 as governments expand bioprocess tax incentives and roll out accelerated approval pathways for rare-disease therapies. China alone has compiled single-cell-omics atlases covering 120 million cells, offering unparalleled annotation depth for AI-training datasets. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) continues to refine its Sakigake fast-track to keep pace with U.S. breakthrough designation metrics.

Europe holds material share yet lags on speed: stringent cell-therapy directives extend trial-setup timelines, though they bolster supply-chain transparency. The region's active-pharmaceutical-ingredient (API) market is climbing 5.78% annually, with synthetic APIs largest today and biotech APIs growing fastest. Oncology remains Europe's most dynamic indication as hospitals integrate companion diagnostics into standard-of-care pathways.

- Beckton Dickinson

- Bio-Rad Laboratories

- Bio-Techne

- Cell Signaling Technology

- Danaher Corporation (Beckman Coulter, Molecular Devices, Cytiva)

- Merck KGaA (MilliporeSigma)

- Thermo Fisher Scientific

- PerkinElmer

- QIAGEN

- Promega

- Agilent Technologies

- Miltenyi Biotec

- Abcam

- Lonza Group

- Enzo Life Sciences

- Creative Diagnostics

- Tocris Bioscience

- GE Healthcare Life Sciences

- BioLegend Inc.

- Oxford Instruments (Andor)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Chronic And Autoimmune Diseases

- 4.2.2 Expanding Funding For Cell-Based Life Science Research

- 4.2.3 Continuous Technological Innovations In Cell Analysis Platforms

- 4.2.4 Increasing Adoption Oo Artificial Intelligence In Bioassay Design

- 4.2.5 Emergence of Three-Dimensional Microfluidic Cell Culture Models

- 4.2.6 Rapid Scale-Up of Cell Therapy Manufacturing Workflows

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Required For Advanced Cell Signaling Systems

- 4.3.2 Ethical And Regulatory Concerns Surrounding Stem Cell Research

- 4.3.3 Inconsistent Quality of Critical Reagents And Antibodies

- 4.3.4 Big-Data Management Challenges In Single-Cell Omics Workflows

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Signaling Type

- 5.1.1 Endocrine Signaling

- 5.1.2 Paracrine Signaling

- 5.1.3 Autocrine Signaling

- 5.1.4 Synaptic Signaling

- 5.1.5 Juxtacrine / Gap-Junction Signaling

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.1.1 Flow Cytometers

- 5.2.1.2 Mass Spectrometers

- 5.2.1.3 Western-Blot Imaging Systems

- 5.2.1.4 ELISA Readers

- 5.2.1.5 Other Instruments

- 5.2.2 Consumables

- 5.2.2.1 Reagents & Kits

- 5.2.2.2 Antibodies

- 5.2.2.3 Media & Sera

- 5.2.2.4 Other Consumables

- 5.2.1 Instruments

- 5.3 By Technology

- 5.3.1 Flow Cytometry

- 5.3.2 Mass Spectrometry

- 5.3.3 Western Blotting

- 5.3.4 ELISA

- 5.3.5 Other Technologies

- 5.4 By Pathway

- 5.4.1 AKT / PI3K Signaling

- 5.4.2 AMPK Signaling

- 5.4.3 ErbB / HER Signaling

- 5.4.4 Other Pathways

- 5.5 By Application

- 5.5.1 Drug Discovery & Development

- 5.5.2 Cancer & Stem-Cell Research

- 5.5.3 Immunology Research

- 5.5.4 Diagnostics

- 5.5.5 Other Applications

- 5.6 By End User

- 5.6.1 Pharma & Biotech Companies

- 5.6.2 Academic & Research Institutes

- 5.6.3 Contract Research Organizations

- 5.6.4 Other End Users

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.5.3.1 GCC

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Becton, Dickinson And Company

- 6.3.2 Bio-Rad Laboratories Inc.

- 6.3.3 Bio-Techne Corporation

- 6.3.4 Cell Signaling Technology Inc.

- 6.3.5 Danaher Corporation (Beckman Coulter, Molecular Devices, Cytiva)

- 6.3.6 Merck KGaA (MilliporeSigma)

- 6.3.7 Thermo Fisher Scientific Inc.

- 6.3.8 PerkinElmer Inc.

- 6.3.9 Qiagen NV

- 6.3.10 Promega Corporation

- 6.3.11 Agilent Technologies

- 6.3.12 Miltenyi Biotec

- 6.3.13 Abcam Plc

- 6.3.14 Lonza Group AG

- 6.3.15 Enzo Life Sciences

- 6.3.16 Creative Diagnostics

- 6.3.17 Tocris Bioscience

- 6.3.18 GE Healthcare Life Sciences

- 6.3.19 BioLegend Inc.

- 6.3.20 Oxford Instruments (Andor)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment