PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848113

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848113

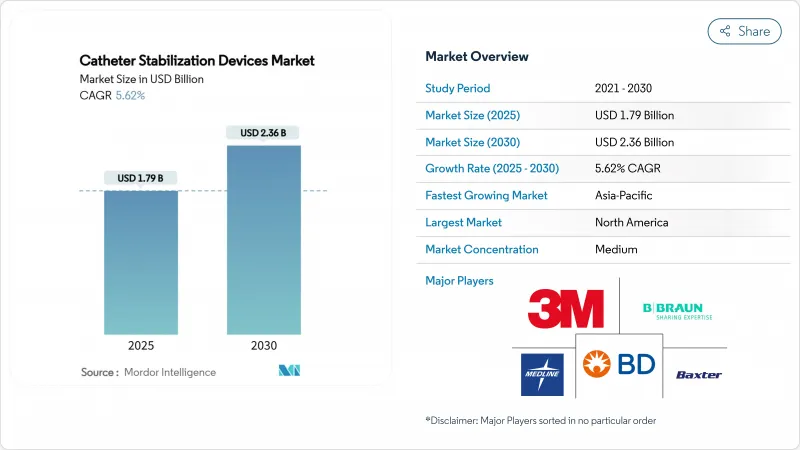

Catheter Stabilization Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The catheter securement devices market size is valued at USD 1.79 billion in 2025 and is forecast to reach USD 2.36 billion by 2030, advancing at a 5.62% CAGR.

Increasing clinical vigilance around catheter-associated infections, the steady expansion of minimally invasive procedures, and stronger demand for hospital-at-home care collectively reinforce the growth outlook. Hospitals intensify spending on infection-control consumables, while ambulatory settings and home-based infusion programs create new use cases that favor portable, easy-to-apply securement formats. Rising oncology caseloads, an aging population that requires frequent vascular access, and innovation in skin-friendly antimicrobial adhesives further sustain the catheter securement devices market trajectory. Manufacturers respond by investing in differentiated designs that reduce dislodgement, lower CLABSI risk, and meet emerging sustainability mandates without compromising performance.

Global Catheter Stabilization Devices Market Trends and Insights

Rising Prevalence of Chronic Lifestyle Diseases

The global rise in diabetes, cardiovascular disease, and cancer drives long-term demand for securement solutions that maintain catheter integrity over extended treatment cycles. Oncology protocols increasingly rely on peripherally inserted central catheters, resulting in a 6.81% CAGR for the segment as clinicians favor devices that cut dislodgement without compromising skin integrity. Seniors now constitute a larger share of hospitalized patients, and their fragile vasculature heightens the need for gentle yet robust securement. Hospitals invest in antimicrobial dressings that lower infection risk, thereby reducing cost of care and readmission penalties. This demographic shift positions the catheter securement devices market as a central component of chronic disease management strategies.

Expansion of Minimally Invasive & Catheter-Based Procedures

Interventional platforms such as transcatheter aortic valve replacement and robotic-assisted vascular therapies rely on precise catheter stability during lengthy procedures. Same-day discharge protocols mean patients leave the hospital sooner, placing a premium on securement devices that continue to perform without continuous monitoring. Device makers respond by engineering low-profile anchors that allow imaging access while resisting accidental pull forces. Premium pricing is achievable when a securement device is purpose-built for a specialized interventional workflow, enhancing revenue diversity within the catheter securement devices market.

Migration to Subcutaneous Ports / Needle-Free Connectors

Needle-free connectors such as BD's MaxPlus line show CLABSI reductions across more than 3,000 U.S. hospitals, shifting clinician preference toward hub-level infection control . Subcutaneous anchors like SecurAcath cut CLABSI risk by 288%, challenging adhesive devices. UV-C disinfection devices further decrease reliance on traditional securement by managing pathogens at the connector site. As integrated alternatives proliferate, sales of standalone surface adhesives may plateau.

Other drivers and restraints analyzed in the detailed report include:

- Stricter CLABSI & CAUTI Prevention Guidelines

- Greater Hospital Spend on Infection-Control Consumables

- Shift to Hospital-at-Home & Outpatient Infusion Programs

- Advanced Skin-Friendly Antimicrobial Adhesive Platforms

- Frequent Product Recalls & Adverse-Event Litigation

- Sustainability Mandates Curbing Single-Use Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peripheral IV securement devices accounted for 37.82% of the catheter securement devices market in 2024. Central venous solutions, though smaller, are projected to expand at a 6.30% CAGR due to critical-care complexity and CLABSI prevention mandates. These two categories collectively define the bulk of catheter securement devices market size, with arterial, urinary, and other niche formats serving specialized needs such as dialysis and pediatric care.

Developers enhance peripheral IV products with integrated antimicrobial overlays and transparent, breathable films that allow daily site inspection. In the CVC space, tunneled PICC placements exhibit better infection and dislodgement profiles than non-tunneled lines, prompting vendors to innovate around anchoring mechanisms that accommodate tunneling techniques. Anticipated regulatory clarity for force-activated separation devices should foster additional product differentiation further reinforcing growth prospects for the catheter securement devices market.

The Catheter Securement Devices Market Report is Segmented by Product (Peripheral IV Catheter Securement Devices, and More), Application (Cardiovascular Procedures, and More), End-User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, APAC, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 45.35% of catheter securement devices market share in 2024, underpinned by stringent infection-control policies and robust reimbursement pathways. Medicare's 2025 provisions for home infusion therapy further extend device use into residential settings, reinforcing the regional growth runaway.

Europe shows consistent expansion as hospitals adapt to sustainability regulations that favor recyclable or biodegradable securement components, propelling product redesign and procurement cycles. Clinical research concentration in Germany, France, and the United Kingdom accelerates local adoption of innovative adhesives that satisfy both infection-control and environmental objectives.

Asia-Pacific is set to outpace global averages at a 7.14% CAGR through 2030. Healthcare infrastructure modernization in China and India, combined with aging demographics in Japan and South Korea, steers demand toward advanced vascular access solutions. Regulatory harmonization initiatives streamline approvals, allowing multinational manufacturers to deploy uniform product lines while accommodating local care protocols.

- 3M

- Beckton Dickinson

- Baxter

- B. Braun

- ConvaTec Group plc

- Medline Industries

- Medtronic

- Merit Medical Systems

- TIDI Products

- Argon Medical Devices

- CATHETRIX

- Smiths Group

- Teleflex

- Avanos Medical (Halyard)

- Vygon

- Cardinal Health

- Centurion Medical Products

- SecurePort Medical

- Marpac Inc.

- Tractus Vascular

- Levity Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Chronic Lifestyle Diseases

- 4.2.2 Expansion Of Minimally Invasive & Catheter-Based Procedures

- 4.2.3 Stricter CLABSI & CAUTI Prevention Guidelines

- 4.2.4 Greater Hospital Spend On Infection-Control Consumables

- 4.2.5 Shift To Hospital-At-Home & Outpatient Infusion Programs

- 4.2.6 Advanced Skin-Friendly Antimicrobial Adhesive Platforms

- 4.3 Market Restraints

- 4.3.1 Migration To Subcutaneous Ports/Needle-Free Connectors

- 4.3.2 Frequent Product Recalls & Adverse-Event Litigation

- 4.3.3 Sustainability Mandates Curbing Single-Use Plastics

- 4.3.4 Hospital Reimbursement Squeeze On "Non-Revenue" Disposables

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD Million)

- 5.1 By Product

- 5.1.1 Peripheral IV catheter securement devices

- 5.1.2 Central venous catheter (CVC) securement devices

- 5.1.3 Arterial catheter securement devices

- 5.1.4 Urinary catheter securement devices

- 5.1.5 Other niche securement devices

- 5.2 By Application

- 5.2.1 Cardiovascular procedures

- 5.2.2 Oncology & chemotherapy

- 5.2.3 Critical care & emergency medicine

- 5.2.4 Gastro-urology & nephrology

- 5.2.5 Pain management & anesthesia

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-Care & Hospital-at-Home Programs

- 5.3.4 Long-term Care / Skilled Nursing Facilities

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 APAC

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of APAC

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M

- 6.3.2 Becton, Dickinson & Co.

- 6.3.3 Baxter International

- 6.3.4 B. Braun SE

- 6.3.5 ConvaTec Group plc

- 6.3.6 Medline Industries

- 6.3.7 Medtronic plc

- 6.3.8 Merit Medical Systems

- 6.3.9 TIDI Products

- 6.3.10 Argon Medical Devices

- 6.3.11 CATHETRIX

- 6.3.12 Smiths Medical (ICU Medical)

- 6.3.13 Teleflex Inc.

- 6.3.14 Avanos Medical (Halyard)

- 6.3.15 Vygon SA

- 6.3.16 Cardinal Health

- 6.3.17 Centurion Medical Products

- 6.3.18 SecurePort Medical

- 6.3.19 Marpac Inc.

- 6.3.20 Tractus Vascular

- 6.3.21 Levity Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment