PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848142

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848142

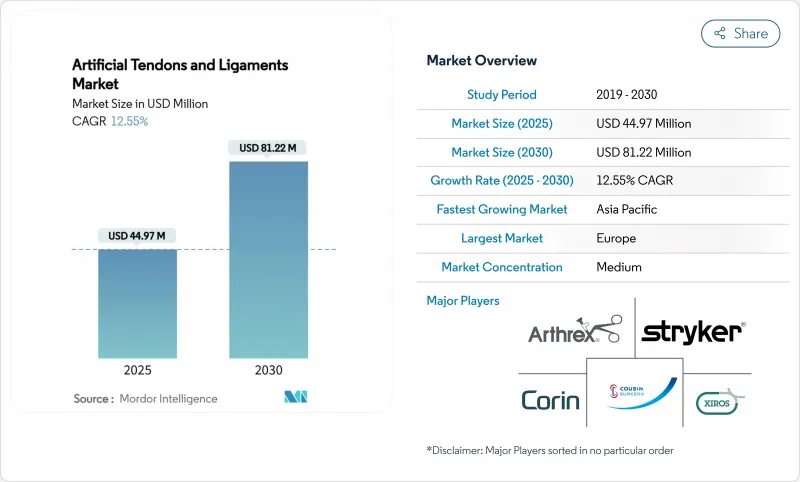

Artificial Tendons And Ligaments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The artificial tendons and ligaments market size is USD 44.97 million in 2025 and is forecast to reach USD 81.22 million in 2030, advancing at a 12.55% CAGR.

Rising sports-related ligament trauma, the shift to minimally invasive techniques, and rapid outpatient surgery growth are reinforcing demand. Europe maintains leadership with 38% revenue share, while Asia-Pacific posts the quickest 13.1% CAGR as regional sports participation climbs. Knee injuries dominate volume at 58% share, yet foot and ankle procedures accelerate at 13.8%. Competitive intensity centers on synthetic PET-LARS systems, but hybrid 3D-printed scaffolds-expanding 17.2%-signal a technological pivot. Hospitals deliver most cases today, though ambulatory surgical centers expand orthopedic capability and account for the market's fastest end-user growth. Strategic acquisitions such as Stryker's purchase of Artelon underscore industry consolidation and the quest for differentiated biomaterials.

Global Artificial Tendons And Ligaments Market Trends and Insights

Rising Global Incidence of Sports-Related Ligament Trauma

Annual ACL reconstructions now reach 400,000, translating to 18 injuries per 100,000 population and higher incidence among athletes. The economic burden extends to rehabilitation and productivity losses, propelling demand for solutions that shorten recovery periods. North America and Europe feel the strongest pull due to organized sports participation and insurance coverage that reimburses ligament reconstruction. Emerging sports leagues in Asia-Pacific add new procedure volumes and last-mile growth. Consequently, hospitals and ASCs invest in advanced graft options that offer immediate mechanical stability and quicker return-to-play timelines.

Growing Preference for Minimally Invasive Techniques

Arthroscopic methods now constitute more than 85% of ligament reconstructions. Clinical evidence from 2024 shows higher functional scores at 1- and 3-month check-ups when autologous tendons are augmented with LARS devices compared with traditional techniques. Surgeons favor all-inside approaches that lessen soft-tissue disruption, reduce narcotic use, and enable same-day discharge. Device makers respond with thinner, pre-loaded synthetic grafts compatible with single-portal instrumentation, supporting current procedural trends across high-volume ASC networks.

Persistent Surgeon Skepticism from Historical Failures

Early synthetic grafts were withdrawn due to mechanical failure and synovitis, as detailed in 2024 literature reviews. Surgeons trained in that period remain cautious and delay adoption until 10-year follow-up data becomes available. Educational symposiums and registry reporting aim to bridge the trust gap, yet skepticism still slows purchasing cycles, particularly in community hospitals.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Outpatient Orthopedic Surgery Infrastructure

- High Implant and Procedure Costs in Cost-Sensitive Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Knee reconstruction commanded 58% artificial tendons and ligaments market share in 2024 as roughly 400,000 ACL surgeries occurred worldwide. The artificial tendons and ligaments market size for knee treatments is forecast to climb steadily on the back of sports medicine volumes, rising older-adult activity, and evidence favoring PET-LARS augmentation in revision scenarios.

Foot and ankle injuries grow fastest at 13.8% CAGR, assisted by new implants tailored to lateral ligament complexes. Medline's 2025 ATFL augmentation device demonstrates the sector's commercial momentum. Surgeons seek synthetic options that improve mechanical stability where autograft harvest is limited. Hospitals in high-volume podiatry centers now bundle ankle ligament repairs with same-day rehabilitation protocols, expanding revenue per episode.

Shoulder repairs benefit from synthetic augmentation solutions that address rotator cuff re-tear rates, while spine and hip applications stay niche but gather momentum from specialized 3D-printed designs. Collectively, non-knee applications expand overall artificial tendons and ligaments market breadth and improve product mix profitability.

Synthetic PET-LARS implants held 64% share in 2024, supported by four decades of mechanical reliability data. The artificial tendons and ligaments market size for PET devices scales with broad regulatory clearance and surgeon familiarity. Evidence indicates a 0.17 odds ratio for re-rupture when PET-LARS augments ACL repair.

Hybrid 3D-printed constructs register a 17.2% CAGR to 2030, reflecting demand for devices combining immediate strength with biologic integration. OEMs employ multiscale biomimicry-porous tendon sheaths and nanohybrid collagen-mimetic fibers-to hasten tissue ingrowth. Early adopters situate hybrid grafts in revision and complex primary cases, where mechanical stability and biology both matter. This segment's rapid expansion realigns R&D budgets and acquisition targets toward materials science innovators.

The Artificial Tendons and Ligaments Market Report is Segmented by Application (Knee Injuries, Foot & Ankle Injuries, and More), Implant Type (Synthetic, and More), Material (Polypropylene, Carbon Fiber and More), Procedure (Primary Reconstruction and Revision Reconstruction), End User (Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe leads with 38% share, aided by historical openness to synthetic ligaments and reimbursement structures that fund premium devices. Countries such as France and Germany widely implant LARS grafts, while new MDR compliance adds regulatory workload that can slow novel product launches. Sports such as soccer and skiing, coupled with aging athlete populations, preserve high procedure demand.

North America places second, underpinned by roughly 200,000 ACL reconstructions annually and accelerating BEAR implant uptick. The outpatient shift dominates strategic planning, with ASCs performing 68% of orthopedic procedures. Early adoption channels foster demand for minimally invasive, hybrid grafts compatible with single-portal techniques.

Asia-Pacific marks the fastest 13.1% CAGR on broader insurance coverage, sports league growth, and robust medical tourism. China's domestic players increase pricing pressures, whereas Japan contributes silk-based biomaterial breakthroughs that feed global pipeline innovation. India's urban sports medicine clinics bolster shoulder and foot-ankle markets despite persistent price sensitivity.

South America and Middle East & Africa show moderate growth centered in major metros. Brazil leverages a passionate soccer culture that elevates ACL volumes, while GCC nations allocate sovereign funds to sports medicine centers serving both residents and inbound medical tourists. Currency fluctuations and unequal insurance access shape purchasing decisions for premium implants.

- Arthrex

- Stryker

- Corin Group

- Xiros Ltd. / Neoligaments

- Mathys

- Orthomed

- FH Orthopedics (Enovis)

- Cousin Biotech

- FX Solutions

- Shanghai PINE & POWER Biotech

- Artelon

- Smith+Nephew plc

- Zimmer Biomet

- Integra LifeSciences

- Miach Orthopaedics

- Bioretec Ltd.

- AlloSource

- MTF Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global incidence of sports-related ligament trauma prompting reconstructive surgeries

- 4.2.2 Growing preference for minimally invasive, accelerated-rehab ligament repair techniques

- 4.2.3 Expansion of outpatient/ambulatory orthopedic surgery infrastructure lowering total treatment cost

- 4.2.4 Accumulating clinical evidence and regulatory clearances for next-generation artificial ligament devices

- 4.2.5 Escalating OEM investments and partnerships in hybrid bio-synthetic graft R&D

- 4.3 Market Restraints

- 4.3.1 Persistent surgeon skepticism stemming from historical synthetic graft failures and limited long-term data

- 4.3.2 High implant and procedure costs versus autograft alternatives in cost-sensitive economies

- 4.3.3 Tightening global regulatory requirements extending product time-to-market

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Knee Injuries (ACL, PCL)

- 5.1.2 Shoulder Injuries (RC, SLAP)

- 5.1.3 Foot & Ankle Injuries (ATFL, Achilles)

- 5.1.4 Spine Injuries

- 5.1.5 Hip Injuries

- 5.2 By Implant Type

- 5.2.1 Synthetic (PET-LARS, Carbon-Fiber, UHMWPE)

- 5.2.2 Biological Augmented (Collagen-Coated PET, Porcine SIS)

- 5.2.3 Hybrid 3-D Printed Scaffolds

- 5.3 By Material

- 5.3.1 Polyethylene Terephthalate (PET)

- 5.3.2 Polypropylene

- 5.3.3 Carbon Fiber

- 5.3.4 Silk & Other Bio-polymers

- 5.4 By Procedure

- 5.4.1 Primary Reconstruction

- 5.4.2 Revision Reconstruction

- 5.5 By End User

- 5.5.1 Hospitals & Specialty Orthopedic Centers

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Sports Medicine Clinics

- 5.5.4 Defense & Military Hospitals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 Stryker Corp.

- 6.3.3 Corin Group

- 6.3.4 Xiros Ltd. / Neoligaments

- 6.3.5 Mathys AG Bettlach

- 6.3.6 Orthomed S.A.S.

- 6.3.7 FH Orthopedics (Enovis)

- 6.3.8 Cousin Biotech

- 6.3.9 FX Solutions

- 6.3.10 Shanghai PINE & POWER Biotech

- 6.3.11 Artelon

- 6.3.12 Smith+Nephew plc

- 6.3.13 Zimmer Biomet

- 6.3.14 Integra LifeSciences

- 6.3.15 Miach Orthopaedics

- 6.3.16 Bioretec Ltd.

- 6.3.17 AlloSource

- 6.3.18 MTF Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment