PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848143

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848143

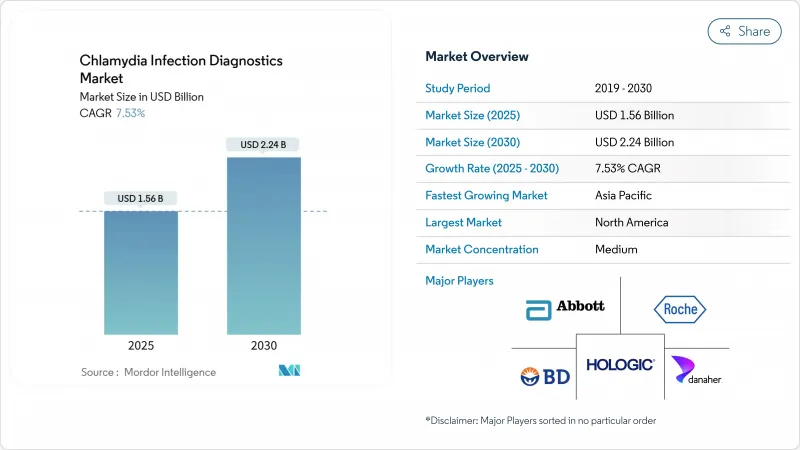

Chlamydia Infection Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The chlamydia infection diagnostics market size generated USD 1.56 billion in 2025 and is forecast to reach USD 2.24 billion by 2030, advancing at a 7.53% CAGR.

Demand growth is anchored in the global rise of sexually transmitted infections, the high rate of asymptomatic cases, and expanding access to molecular platforms that deliver rapid, accurate results. Regulatory catalysts, most notably the FDA's 2025 approval of the first over-the-counter chlamydia home test, are accelerating commercial timelines for similar products while shifting testing closer to consumers. Companies are prioritizing automation, multiplexing, and digital connectivity to shorten time-to-result, contain costs, and reduce loss-to-follow-up. In high-income countries, reimbursement frameworks and mandatory screening recommendations underpin steady test volumes, whereas emerging economies present volume upside once infrastructure bottlenecks are resolved.

Global Chlamydia Infection Diagnostics Market Trends and Insights

Increasing Global Burden of Sexually Transmitted Infections

Chlamydia case notifications have climbed steeply, with 216,508 confirmed cases reported across 27 EU/EEA countries in 2022, a 16% rise from 2021. Young adults aged 20-24 bear a disproportionate share, while infections among men who have sex with men have surged 72% over five years, demonstrating shifting transmission patterns. Because over 80% of infections present without symptoms, disease prevalence is substantially under-reported, pushing health systems toward routine, population-level screening. These epidemiological realities expand the Chlamydia infection diagnostics market by broadening the pool of individuals who require testing in both clinical and community settings.

Rising Government Funding for STI Screening Programs

Government budgets earmarked for STI control have risen across major markets. In the United States, the CDC's Prevention and Control program channels multi-year grants to state health departments, while its 2024 awards provided USD 9 million to scale integrated HIV/STI screening services. A parallel five-year laboratory-capacity initiative (NOFO CD-25-0019) kicks off in July 2025, ensuring reagent supply, staff training, and quality assurance for nucleic acid amplification testing. Similar policy alignment is taking shape internationally as the WHO positions NAAT as the gold-standard test, standardizing procurement criteria and reinforcing the demand curve for the Chlamydia infection diagnostics market.

Persistent Social Stigma Around STI Testing

Stigma continues to deter individuals from seeking diagnosis. Surveys show high hesitancy among adolescents and rural residents who fear judgment or breaches of confidentiality, suppressing clinical visitation rates even when symptoms are present. While home tests offer anonymity, social norms in many regions still discourage purchase and use, limiting uptake and tempering growth in the Chlamydia infection diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Molecular Diagnostic Platforms

- Growing Acceptance of Home-Based Self-Testing Solutions

- Inadequate Laboratory Infrastructure in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Chlamydia infection diagnostics market size for NAAT reached USD 0.95 billion in 2024 and is growing at a stable 7.1% CAGR. Culture tests, while still essential for antimicrobial-resistance surveillance, ceded routine detection to NAAT because of longer incubation times. Rapid lateral-flow assays, projected to post the segment's quickest 4.67% CAGR, leverage low-cost cartridges and minimal hardware to serve pharmacies, outreach vans, and sexual-health clinics. Regulatory momentum favors hybrid platforms that fuse NAAT accuracy with rapid assay turnaround, suggesting portfolio diversification will decide future competitive standings.

Demand for multiplex panels that detect chlamydia, gonorrhea, and trichomonas in one run is increasing. Abbott, Roche, and Hologic are upgrading firmware to integrate new targets without hardware changeovers, preserving capital investments for laboratories and sustaining brand lock-in. High throughput also meets bulk-testing needs driven by government-funded screening, reaffirming NAAT's dominance within the broader Chlamydia infection diagnostics market.

The Chlamydia Infection Diagnostics Market Report is Segmented by Test Type (Culture Tests, Nucleic Acid Amplification Tests (NAAT), and More), Specimen Type (Vaginal Swabs, Urine Samples, and More), End User (Hospitals, Diagnostic Reference Laboratories, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.88% of global revenue in 2024, buoyed by mandatory annual screening guidelines for sexually active women under 25 and comprehensive third-party reimbursement that removes patient cost hurdles. Medicare's preventive-services provisions waive copays and deductibles for STI testing, preserving test volumes even when insurance deductibles trend upward. FDA fast-track pathways also shorten time-to-market for innovators, making the region the premier launchpad for new assays.

Asia-Pacific is the fastest-growing arena, advancing at 4.67% CAGR as public-private initiatives extend laboratory grids and telehealth apps penetrate smartphone-dense populations. Australia's pharmacy-based self-testing rollout, endorsed by the Therapeutic Goods Administration, illustrates policy openness to decentralized screening. Pilot programs in rural indigenous clinics cut the median time from sample collection to treatment from eight days to two, highlighting how rapid diagnostics can curb transmission.

Europe remains a mature but expanding market. The 2025 European guideline solidifies NAAT as first-line diagnosis and recommends doxycycline therapy for seven days, standardizing clinical practice across member states. Surveillance data reveal the region's steady infection climb, thus keeping screening budgets intact. Investments such as bioMerieux's EUR 25 million facility upgrade reinforce Europe's commitment to in-house R&D and advanced microbiology platforms, sustaining its strategic weight in the Chlamydia infection diagnostics market.

- Hologic

- Danaher Corp. (Cepheid)

- Abbott Laboratories

- Roche

- Beckton Dickinson

- DiaSorin

- Quidel-Ortho Corp.

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Luminex Corp. (Diasorin)

- QIAGEN

- Genedrive plc

- Binx Health Inc.

- Visby Medical Inc.

- Trinity Biotech plc

- Savyon Diagnostics Ltd.

- Accelerate Diagnostics Inc.

- Randox Laboratories

- Meridian Bioscience

- Seegene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Global Burden of Sexually Transmitted Infections

- 4.2.2 Rising Government Funding for STI Screening Programs

- 4.2.3 Technological Advancements in Molecular Diagnostic Platforms

- 4.2.4 Growing Acceptance of Home-Based Self-Testing Solutions

- 4.2.5 Expansion Of Public-Private Partnerships In Diagnostic Infrastructure

- 4.2.6 Integration of Point-of-Care Testing in Primary Healthcare Settings

- 4.3 Market Restraints

- 4.3.1 Persistent Social Stigma Around STI Testing

- 4.3.2 Inadequate Laboratory Infrastructure in Emerging Economies

- 4.3.3 High Cost of Advanced Molecular Diagnostic Tests

- 4.3.4 Regulatory and Reimbursement Uncertainties across Regions

- 4.4 Regulatory Landscape

- 4.5 Porte's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Test Type

- 5.1.1 Culture Tests

- 5.1.2 Nucleic Acid Amplification Tests (NAAT)

- 5.1.3 Serology / Rapid Lateral-Flow Assays

- 5.1.4 Direct Fluorescent Antibody Tests

- 5.1.5 Other Test Types

- 5.2 By Specimen Type

- 5.2.1 Vaginal Swabs

- 5.2.2 Urine Samples

- 5.2.3 Endocervical Swabs

- 5.2.4 Rectal & Pharyngeal Swabs

- 5.2.5 Blood / Serum

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Reference Laboratories

- 5.3.3 Sexual-Health / STI Clinics

- 5.3.4 Physician Offices

- 5.3.5 Home-care / Direct-to-Consumer

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Hologic Inc.

- 6.3.2 Danaher Corp. (Cepheid)

- 6.3.3 Abbott Laboratories

- 6.3.4 F. Hoffmann-La Roche Ltd.

- 6.3.5 Becton, Dickinson & Co.

- 6.3.6 DiaSorin SpA

- 6.3.7 Quidel-Ortho Corp.

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 Thermo Fisher Scientific Inc.

- 6.3.10 Luminex Corp. (Diasorin)

- 6.3.11 Qiagen NV

- 6.3.12 Genedrive plc

- 6.3.13 Binx Health Inc.

- 6.3.14 Visby Medical Inc.

- 6.3.15 Trinity Biotech plc

- 6.3.16 Savyon Diagnostics Ltd.

- 6.3.17 Accelerate Diagnostics Inc.

- 6.3.18 Randox Laboratories Ltd.

- 6.3.19 Meridian Bioscience Inc.

- 6.3.20 Seegene Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment