PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940578

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940578

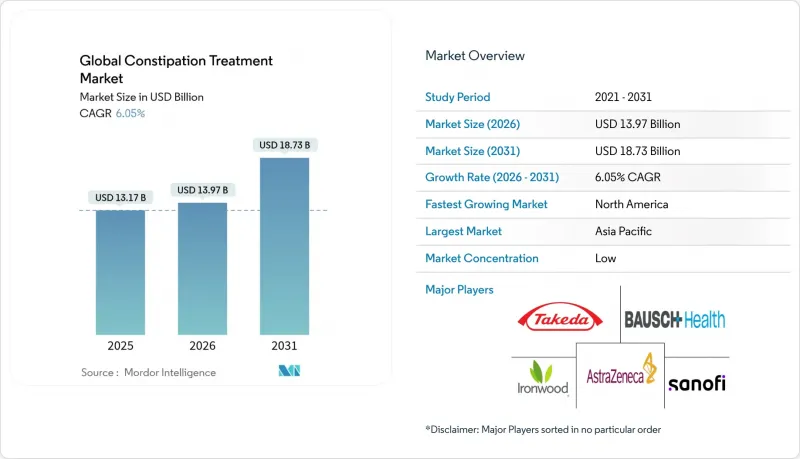

Global Constipation Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The constipation treatment market is expected to grow from USD 13.17 billion in 2025 to USD 13.97 billion in 2026 and is forecast to reach USD 18.73 billion by 2031 at 6.05% CAGR over 2026-2031.

Expanding elderly populations, higher opioid-related constipation rates, and approvals of receptor-targeted drugs underpin this growth trajectory. Precision therapeutics such as GC-C and 5-HT4 agonists continue to displace traditional osmotic laxatives, while gut-brain digital therapeutics and vibrating capsule devices widen the therapeutic playbook. North America maintains clear leadership through favorable reimbursement frameworks, yet Asia-Pacific shows the fastest up-curve thanks to broader healthcare access and rising disposable incomes. Competitive activity remains moderate as incumbents defend franchises against generics and newcomers focused on microbiome and digital health tools.

Global Constipation Treatment Market Trends and Insights

Increasing Prevalence of Chronic Idiopathic Constipation in Ageing Population

As the share of adults aged >= 65 climbs, chronic idiopathic constipation rates have reached 15%, almost doubling younger cohorts. Reduced colonic motility, lower rectal sensation, and polypharmacy interplay intensify treatment dependence. Constipation-related emergency department visits now exceed 1.3 million annually in the United States, with fecal impaction cases showing 40.6% serious complication rates and nearly 90% hospital admission rates, highlighting the inadequacy of current therapeutic approaches. The purchasing power of baby boomers magnifies demand for higher-efficacy therapies that support daily functioning. Drug developers are therefore steering R&D budgets toward gut-brain axis modulators, microbiome correction, and circadian rhythm agents tailored to geriatric physiology.

Rising Opioid Prescriptions Driving Demand for OIC Therapeutics

Opioid-induced constipation affects up to 81% of chronic pain patients and now represents a USD 2.1 billion opportunity within the broader constipation treatment market. Grunenthal's USD 250 million deal for naloxegol underscores the growing appeal of peripherally acting µ-opioid receptor antagonists that restore bowel function without blunting analgesia. Adherence tops 70%, far above conventional laxatives, securing sticky revenue streams. Shionogi's naldemedine clearance in China broadens geographic reach and illustrates expanding payer readiness in Asia-Pacific.

Safety Concerns Over Long-Term Use of Stimulant Laxatives

The EMA banned hydroxyanthracene compounds in 2025, tightening leverage on senna and cascara products. Physicians now lean toward osmotic or receptor-targeted agents, particularly for frail seniors susceptible to electrolyte imbalance. Consequently, legacy stimulant brands face shelf-space erosion in Europe and ripple effects in other stringent jurisdictions.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward OTC Self-Medication & E-Pharmacy Penetration

- Novel GC-C and 5-HT4 Agonists Gaining Approvals

- Patent Cliffs for Blockbuster Agents Intensifying Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pharmacological offerings captured an 83.02% slice of the constipation treatment market in 2025, led by GC-C and 5-HT4 agonists that outperformed bulk-forming and osmotic agents on sustained relief metrics. Within this pillar, GC-C drugs such as linaclotide posted USD 800 million in sales, while peripherally acting µ-opioid receptor antagonists benefited from high adherence among pain patients. Despite entrenched dominance, looming generics and safety vigilance for stimulants temper future share.

Non-pharmacological approaches expanded at a 7.03% CAGR and headline disruptive potential. FDA-cleared vibrating capsules produced 64% responder rates versus 36% placebo. Digital gut-brain programs recorded 73% improvement, positioning them as adjuncts that lift pharmacotherapy efficacy. As pipelines mature, cross-modal regimens could narrow pharmacological lead by decade's end.

Oral drugs delivered 86.15% of the constipation treatment market share in 2025, owing to convenience and chronic-use practicality. The constipation treatment market size for oral options is projected to climb at a 5.88% CAGR, even as innovation spreads.

Parenteral solutions-including subcutaneous methylnaltrexone for refractory opioid cases-post a faster 7.21% pace, albeit from a low base. Enhancements like vibration-enabled capsules reinforce oral loyalty by boosting efficacy without systemic drug load. Rectal forms remain niche for rapid in-clinic decompression or pediatric dosing constraints.

The Constipation Treatment Market Report is Segmented by Treatment Type (Pharmacological Laxatives, Non-Pharmacological), Route of Administration (Oral, Rectal, Parenteral), Patient Type (Adults, Pediatrics, Geriatrics), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.88% of 2025 sales, underpinned by high therapeutic adoption rates, resilient reimbursement, and heavy opioid use creating OIC incidence. The constipation treatment market size in the United States alone surpassed USD 5.28 billion in 2026 as prescribers favored GC-C agonists for chronic idiopathic constipation. Generic prucalopride's entry reflects the region's hotbed for first-wave competition.

Asia-Pacific is the fastest advancing territory with an 7.86% CAGR to 2031. China's insurance reforms and rising middle-class purchasing power widen access to advanced therapies, while culturally embedded herbal formulas such as Tongbian are studied alongside Western drugs. Japan leverages both Kampo remedies and receptor-targeted drugs for its aging population, and India's e-pharmacy boom couples price sensitivity with digital reach.

Europe delivers steady but slower momentum, constrained by stringent health technology assessments and the 2025 ban on hydroxyanthracene botanicals. The constipation treatment market share of stimulant laxatives has already fallen in Germany and France, opening room for osmotic and GC-C agents. Post-Brexit regulatory divergence could either speed or stall UK approvals relative to the EU, yet payer scrutiny remains universally tight.

- Takeda Pharmaceuticals

- Bayer

- Ironwood Pharmaceuticals

- Abbvie

- Sanofi

- AstraZeneca

- Shionogi & Co., Ltd.

- Bausch Health

- GlaxoSmithKline

- Johnson & Johnson

- Procter & Gamble

- Cipla

- Daewoong Pharmaceutical Co. Ltd.

- Nichirin Pharmaceutical

- HERMES PHARMA GmbH

- Nestle Health Science

- Herbalife Nutrition Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing prevalence of chronic idiopathic constipation in ageing population

- 4.2.2 Rising opioid prescriptions driving demand for OIC therapeutics

- 4.2.3 Shift toward OTC self-medication & e-pharmacy penetration

- 4.2.4 Novel GC-C and 5-HT4 agonists gaining approvals

- 4.2.5 Microbiome-derived therapeutics entering late-stage pipeline

- 4.2.6 Digital therapeutics & gut-brain neurostimulation apps improving adherence

- 4.3 Market Restraints

- 4.3.1 Safety concerns over long-term use of stimulant laxatives

- 4.3.2 Patent cliffs for blockbuster agents intensifying price competition

- 4.3.3 Supply-chain shortages of PEG & senna due to ESG controls

- 4.3.4 Consumer shift to herbal & home remedies reducing prescription uptake

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Treatment Type (Value)

- 5.1.1 Pharmacological

- 5.1.1.1 Laxatives

- 5.1.1.2 Chloride Channel Activators (Lubiprostone)

- 5.1.1.3 GC-C Agonists (Linaclotide, Plecanatide)

- 5.1.1.4 5-HT4 Agonists (Prucalopride, Naronapride)

- 5.1.1.5 Peripherally Acting µ-Opioid Receptor Antagonists

- 5.1.1.6 Others (Bile-acid modulators, etc.)

- 5.1.2 Non-Pharmacological

- 5.1.2.1 Dietary Fibre Supplements

- 5.1.2.2 Biofeedback & Physical Therapy

- 5.1.2.3 Fecal Microbiota Transplant

- 5.1.2.4 Digital Therapeutics

- 5.1.1 Pharmacological

- 5.2 By Route of Administration (Value)

- 5.2.1 Oral

- 5.2.2 Rectal (Suppositories, Enemas)

- 5.2.3 Parenteral / Sub-cutaneous

- 5.3 By Patient Type (Value)

- 5.3.1 Adults

- 5.3.2 Pediatrics

- 5.3.3 Geriatrics

- 5.4 By Distribution Channel (Value)

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies & Drug Stores

- 5.4.3 Online Pharmacies

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Takeda Pharmaceutical Company Limited

- 6.3.2 Bayer AG

- 6.3.3 Ironwood Pharmaceuticals, Inc.

- 6.3.4 AbbVie Inc.

- 6.3.5 Sanofi S.A.

- 6.3.6 AstraZeneca plc

- 6.3.7 Shionogi & Co., Ltd.

- 6.3.8 Bausch Health Companies Inc.

- 6.3.9 GlaxoSmithKline plc

- 6.3.10 Johnson & Johnson

- 6.3.11 Procter & Gamble Co.

- 6.3.12 Cipla Ltd.

- 6.3.13 Daewoong Pharmaceutical Co. Ltd.

- 6.3.14 Nichirin Pharmaceutical

- 6.3.15 HERMES PHARMA GmbH

- 6.3.16 Nestle Health Science

- 6.3.17 Herbalife Nutrition Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment