PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848152

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848152

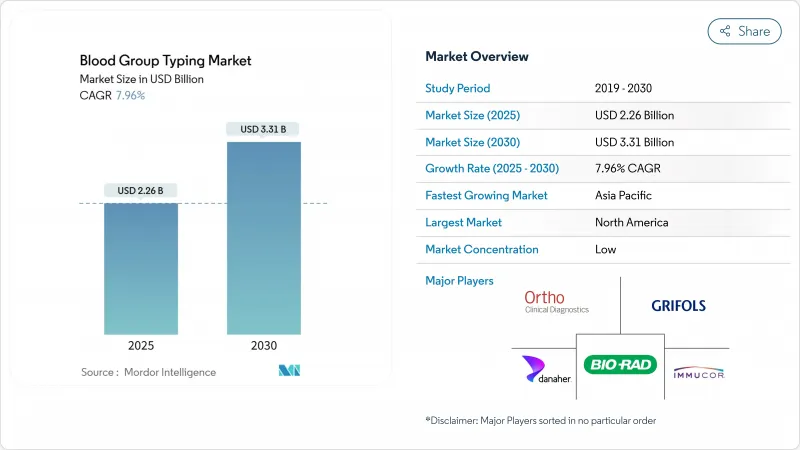

Blood Group Typing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The blood typing market size was valued at USD 2.26 billion in 2025 and is forecast to reach USD 3.31 billion by 2030, advancing at a 7.96% CAGR.

Rising surgical volumes, higher life expectancy, and the clinical shift toward precision transfusion protocols underpin this steady expansion. Rapid technology adoption-from high-throughput serology analyzers to next-generation sequencing (NGS) platforms-strengthens test accuracy and throughput, while enabling laboratories to resolve complex antibody work-ups within hours instead of days. Demand also gains from government-funded blood donation drives, especially in Asia-Pacific, that channel large numbers of collected units into standardized testing workflows. Automation is closing the gap created by laboratory staffing shortages, with instrument vendors embedding robotics, advanced optics, and artificial intelligence to deliver faster results and lower per-test costs. Hospital consolidation in North America and Europe further favors integrated platforms that combine instruments, reagents, middleware, and outsourced reference services under one purchasing contract.

Global Blood Group Typing Market Trends and Insights

Growth in Global Blood Transfusion Procedures

Worldwide transfusion volumes continue to climb as complex cardiovascular, trauma, and oncological interventions become commonplace. Each transfusion episode triggers multiple compatibility checks, so even marginal increases in procedure counts magnify reagent and instrument demand. Emergency medicine now requires point-of-care analyzers that can process ABO-Rh typing in under five minutes, a capability that high-volume hospitals in the United States and Japan already view as essential. Automated workflows are therefore replacing manual tube testing in both tertiary centers and regional trauma networks.

Rising Prevalence of Chronic and Hematological Disorders

Long-term transfusion support for thalassemia, sickle cell disease, and hematologic cancers is reshaping routine practice from basic ABO-Rh matching to extended antigen phenotyping. Molecular assays that read multiple blood group loci in a single run limit alloimmunization, a risk especially acute in multi-transfused pediatric patients. Oncology protocols are also adopting prophylactic typing to offset transfusion reactions during chemotherapy cycles.

Limited Healthcare Infrastructure in Low-Income Regions

Inconsistent electricity, inadequate cold chain capacity, and scarce maintenance expertise hamper reliable blood typing in a sizable share of African and rural South Asian facilities. Cap-ex hurdles slow adoption of NGS and even mid-tier automated serology systems, compelling many centers to rely on manual slide or rapid card tests with lower sensitivity.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of National Blood Donation Programs

- Technological Advancements in Automated Blood Typing Systems

- Shortage of Skilled Laboratory Personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables accounted for 48.32% of blood typing market share in 2024, reflecting the high frequency of reagents used for routine gel card and microplate testing. The services category, however, is projected to post a 10.45% CAGR to 2030 as laboratories increasingly outsource NGS-based antigen panels and rare antibody identification. That outsourcing trend enlarges the blood typing market size for specialized reference providers, many of which package logistics, sequencing, and interpretive reports under subscription agreements. Instruments maintain mid-single-digit growth, driven by upgrades to AI-enabled analyzers that optimize reagent use and interface directly with hospital LIS platforms.

Laboratory managers cite the capital-intensive nature of NGS as the main reason for send-out adoption. Meanwhile, reagent suppliers face price pressure as automated analyzers become more frugal with micro-volume reaction pads. Despite that, rising total test volumes secure stable revenue streams for gel cards, buffers, and control sera. Instrument manufacturers differentiate through modular designs that expand from 96 to 384 well formats, aligning capacity with fluctuating seasonal demand.

PCR and microarray platforms delivered 37.23% of segment revenue in 2024, yet NGS is forecast to climb at a 12.45% CAGR, reflecting unrivaled depth of antigen coverage. The blood typing market size for NGS reagents is still below traditional serology reagents, but rapid uptake in reference centers is narrowing the gap. Multi-locus sequencing resolves Rh, Kell, Kidd, and Duffy variants in a single assay, which supports precision-matching policies for chronically transfused patients.

While serology remains the frontline workhorse for same-day ABO-Rh testing, clinicians now consider NGS confirmation indispensable for complex phenotyping. Microfluidics and lateral-flow cassettes keep a foothold in resource-constrained or emergency settings due to minimal training requirements. Hybrid workflows are therefore common: a slide or column agglutination test confirms immediate compatibility, with NGS data arriving a day later to refine extended match decisions.

The Blood Group Typing Market Report is Segmented by Product (Instruments, Consumables, and Services), Technique (Serology Assay-Based, PCR-Based & Microarray, and More), Test Type (ABO Blood Tests, Antibody Screening, and More), End User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 33.45% of revenue in 2024 thanks to stringent regulatory oversight, high healthcare spending, and a mature hospital network that prioritizes fully automated immunohematology. FDA clearances in 2025 for integrated serology-molecular workstations illustrate the region's appetite for technology that merges gel card processing with reflex NGS and AI-based interpretation. A tight labor market further accelerates instrument replacement cycles, as labs gravitate to walk-away analyzers that need fewer hands-on minutes.

Asia-Pacific is forecast to post the highest 8.92% CAGR through 2030. National blood donation expansion across India, Indonesia, and Vietnam is pouring large sample volumes into both public and private testing channels, while China is fast-tracking automated reagent rental programs in provincial centers. Japan holds the highest per-capita test penetration, driven by rapid uptake of molecular typing for oncology and transplantation. Local manufacturers in South Korea and China are entering the mid-range instrument tier, challenging Western incumbents on price and after-sales service.

Europe maintains steady mid-single-digit growth. Harmonized EU medical device regulations impose rigorous performance verification, yet reimbursement frameworks in Germany, France, and the Nordics support adoption of high-spec analyzers that reduce sample volume and waste. Meanwhile, the Middle East and Africa display uneven progress. Gulf Cooperation Council countries import top-end instruments for tertiary hospitals, whereas many sub-Saharan facilities rely on manual slide testing due to power instability. South America gains momentum as Brazil's hemovigilance reforms channel capital into centralized testing hubs that serve multiple states.

- Bio-Rad Laboratories

- Grifols

- Ortho Clinical Diagnostics

- Danaher Corp. (Beckman Coulter)

- Immucor Inc. (Werfen)

- Thermo Fisher Scientific

- Mesa Laboratories (Agena Bioscience)

- Merck

- Quotient Ltd.

- DIAGAST

- AXO Science

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Beckton Dickinson

- Terumo Blood & Cell Technologies

- Fujirebio

- Tulip Diagnostics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Global Blood Transfusion Procedures

- 4.2.2 Rising Prevalence of Chronic and Hematological Disorders

- 4.2.3 Expansion of National Blood Donation Programs

- 4.2.4 Technological Advancements in Automated Blood Typing Systems

- 4.2.5 Increasing Adoption of Molecular Diagnostics in Transfusion Medicine

- 4.2.6 Government Initiatives for Maternal and Neonatal Health

- 4.3 Market Restraints

- 4.3.1 Limited Healthcare Infrastructure in Low-Income Regions

- 4.3.2 Shortage of Skilled Laboratory Personnel

- 4.3.3 High Cost of Advanced Typing Technologies

- 4.3.4 Stringent Regulatory and Compliance Requirements

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Suppliers

- 4.5.3 Bargaining Power Of Buyers/Consumers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.1.1 Automated Systems

- 5.1.1.2 Semi-Automated Systems

- 5.1.1.3 Manual Readers & Centrifuges

- 5.1.2 Consumables

- 5.1.2.1 Reagent Red Cells & Antisera

- 5.1.2.2 Gel Cards & Microplates

- 5.1.2.3 Molecular Assay Kits & Panels

- 5.1.3 Services

- 5.1.1 Instruments

- 5.2 By Technique

- 5.2.1 Serology Assay-Based

- 5.2.2 PCR-Based & Microarray

- 5.2.3 Massively Parallel / NGS

- 5.2.4 Lateral-Flow & Microfluidic

- 5.3 By Test Type

- 5.3.1 ABO Blood Tests

- 5.3.2 Antibody Screening

- 5.3.3 Cross-Matching Tests

- 5.3.4 HLA Typing

- 5.3.5 Antigen Typing (Kidd, Duffy, Etc.)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Blood Banks

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Bio-Rad Laboratories Inc.

- 6.3.2 Grifols S.A.

- 6.3.3 Ortho Clinical Diagnostics

- 6.3.4 Danaher Corp. (Beckman Coulter)

- 6.3.5 Immucor Inc. (Werfen)

- 6.3.6 Thermo Fisher Scientific

- 6.3.7 Mesa Laboratories (Agena Bioscience)

- 6.3.8 Merck KGaA (Sigma-Aldrich)

- 6.3.9 Quotient Ltd.

- 6.3.10 DIAGAST

- 6.3.11 AXO Science

- 6.3.12 Abbott Laboratories

- 6.3.13 Roche Diagnostics

- 6.3.14 Siemens Healthineers

- 6.3.15 Becton, Dickinson & Co.

- 6.3.16 Terumo Blood & Cell Technologies

- 6.3.17 Fujirebio

- 6.3.18 Tulip Diagnostics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment