PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848300

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848300

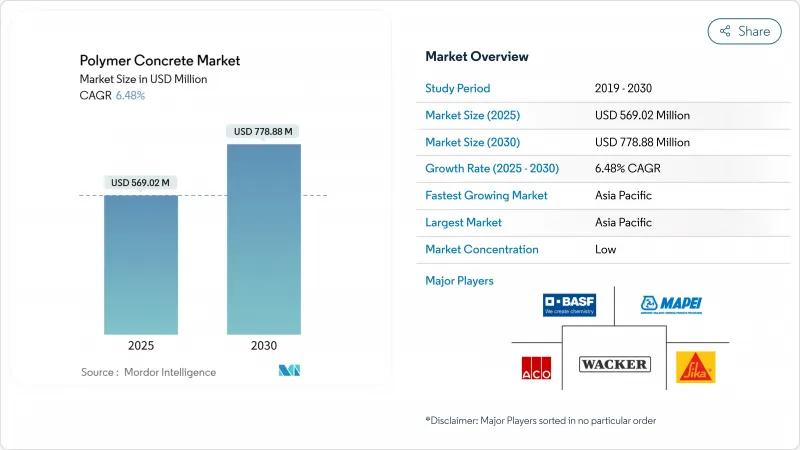

Polymer Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The polymer concrete market size stood at USD 569.02 million in 2025 and is on track to reach USD 778.88 million by 2030, advancing at a 6.48% CAGR.

Growth is anchored in infrastructure hardening programs that prioritize corrosion-proof materials, sustained capital spending on data-center drainage networks, and expanding use of non-conductive pads for utility equipment. Rapid urbanization in Asia Pacific, tighter European sustainability mandates, and progress in bio-based binder technology collectively widen application scope. Strategic acquisitions by leading producers, coupled with performance-driven formulation upgrades, are underpinning steady pricing power and stable margins in most regions.

Global Polymer Concrete Market Trends and Insights

Corrosion-proof Infrastructure Gains Momentum

Regional utilities are replacing steel-reinforced concrete with epoxy-bound alternatives in sewage mains and desalination plants because polymer concrete retains up to 90% of its initial strength after prolonged acid and salt exposure researchgate.net. GCC governments, contending with aggressive chloride environments, now specify polymer concrete for trunk lines and plant vessels. Local contractors such as DAW Construction and Qatar General Projects Company have launched region-specific mixes that resist extreme temperature swings, illustrating how the polymer concrete market leverages location-tailored chemistry for lifespan assurance

Chemical-resistant Materials in Industrial Hubs

Key Highlights

- Chemical processors in coastal China, South Korea, the U.S. Gulf Coast, and Germany are upgrading tank plinths, secondary containment, and loading bays with resin-rich formulations. Demand spiked after operators quantified lifecycle savings from fewer shutdowns and thinner wall sections compared with conventional mixes. Steady capacity expansions in battery chemicals, fertilizers, and specialty resins maintain a baseline flow of projects that feed the polymer concrete market.

Certification Hurdles in Structural Uses

Key Highlights

- Polymer concrete floor and wall panels still lack harmonized fire-rating protocols across major building codes. Developers stay cautious until independent labs publish full-scale test results that demonstrate reliable two-hour ratings, limiting uptake in mid-rise structures where code officials require redundant compliance proofs.

Other drivers and restraints analyzed in the detailed report include:

- European Micro-plastic Regulations Drive Road Overlay Upgrades

- U.S. Grid-hardening Favors Non-conductive Pads

- Extended Lead-times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy accounted for 52% of 2024 revenue, the largest share within the polymer concrete market, and is projected to rise at a 7.21% CAGR through 2030. Superior bond strength and resistance to acids underpin this dual leadership. Recent dynamic-loading research confirmed that epoxy mixes sustain higher peak stress under cyclic impact, a feature favored in rail sleepers and bridge paving. Methyl methacrylate grades address rapid-set repairs on airport runways where traffic disruption costs escalate quickly. Acrylate and latex systems occupy small niches for flexible overlays and bonding to aged substrates.

Epoxy's dominance also shapes additive demand patterns, encouraging suppliers of chopped glass fibers and silica flour to optimize particle gradation for resin-rich matrices. Polyester retains relevance in cost-sensitive applications but faces headwinds from compressive-strength limits. As value-chain participants broaden formulation options, the polymer concrete industry benefits from tailored chemistries that serve price-performance trade-offs.

Synthetic resin held an 80% share in 2024, reflecting decades of validated field performance. Pilot studies on natural binders recorded 59.6 MPa compressive strength for gelatin-modified composites, signaling technical feasibility. Government incentives for circular materials are pushing laboratories to evaluate chitosan, lignin and alginate as partial replacements. This research pipeline supports a 7.56% CAGR for natural resin through 2030, the fastest rate in the binding-agent hierarchy.

Producers are mapping their transition strategy by introducing hybrid systems that cap fossil-derived content at 60%. Early adopters in Scandinavia and Japan are purchasing pilot batches for green-certified civic works, creating demand pockets that will ripple through the polymer concrete market in the coming years. Technical documentation continues to focus on resin-aggregate compatibility, rheology control, and long-term weathering performance.

The Polymer Concrete Market Report Segments the Industry by Polymer Type (Epoxy, Polyester, and More), Binding Agent (Natural Resin, Synthetic Resin), Application (Asphalt Pavement, Building and Maintenance, and More), End-User Industry (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD Million)

Geography Analysis

Asia Pacific dominated sales with a 41.5% share in 2024, supported by China's Belt and Road corridor upgrades and India's smart-city sewer rehabilitation. Regional research institutes collaborate with domestic producers to tune formulations for tropical humidity and sulfate-rich soils, reinforcing local supply chains. The polymer concrete market size in Asia Pacific is projected to expand at a 7.45% CAGR through 2030, stimulated by expanding wastewater treatment capacity and rapid data-center construction.

North America maintains steady growth as the Infrastructure Investment and Jobs Act funds bridge deck overlays, shoreline protection, and resilient energy assets. Europe's stringent carbon and micro-plastic regulations accelerate the adoption of durable, low-maintenance materials.

The Middle East and Africa record rising demand in desalination plants, district cooling channels, and chemical terminals. South America's activity centers on Brazil's port expansions, biofuel facilities, and mining assets; polymer concrete offers lifecycle savings under acidic and abrasive operating conditions.

- ACO Ahlmann SE & Co. KG

- ACO FUNKI A/S

- Arizona Polymer Flooring Inc. (ICP Building Solutions Group)

- BASF SE

- Dudick Inc.

- Forte Composites Inc.

- Fosroc International Ltd.

- Hycrete Inc.

- Interplastic Corporation

- Mapei S.p.A.

- Metro Cast Corporation

- QGPC

- Sika AG

- TPP Manufacturing Sdn. Bhd.

- Ulma Architectural Solutions

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Polymer Concrete for Corrosion-Proof Sewage and Desalination Assets in GCC

- 4.2.2 Increasing Need for Chemical Resistant Construction Material

- 4.2.3 Europe Mandates on Micro-plastics Accelerating Shift to Low-Permeability Epoxy-Based Road Overlays

- 4.2.4 U.S. Utility Hardening Programs Specifying Non-Conductive Polymer Concrete Pads

- 4.2.5 Growth of Prefabricated Polymer Concrete Drainage Channels in Data-Center Construction

- 4.3 Market Restraints

- 4.3.1 Fire-Rating Certification Gaps Limiting Polymer Concrete Use in Mid-Rise Buildings

- 4.3.2 High Volatility in Bisphenol-A Epoxy Pricing Compressing Contractor Margins (NA)

- 4.3.3 Raw-Material Import Dependence Elevates Lead-Times for Emerging economies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts ( Value)

- 5.1 By Polymer Type

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Methyl Methacrylate

- 5.1.4 Latex

- 5.1.5 Acrylate

- 5.1.6 Others (Furan, Phenolic-Formaldehyde, Acetone-Formaldehyde, Carbamide)

- 5.2 By Binding Agent

- 5.2.1 Natural Resin

- 5.2.2 Synthetic Resin

- 5.3 By Application

- 5.3.1 Asphalt Pavement and Overlays

- 5.3.2 Building and Maintenance

- 5.3.3 Industrial Tanks

- 5.3.4 Prefabricated Drainage Systems

- 5.3.5 Others (Outdoor Furniture and Architectural Components, Solid-Surface Counters and Overlays)

- 5.4 By End-User Industry

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Infrastruture

- 5.4.4 Industrial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, Joint Ventures, Agreements)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ACO Ahlmann SE & Co. KG

- 6.4.2 ACO FUNKI A/S

- 6.4.3 Arizona Polymer Flooring Inc. (ICP Building Solutions Group)

- 6.4.4 BASF SE

- 6.4.5 Dudick Inc.

- 6.4.6 Forte Composites Inc.

- 6.4.7 Fosroc International Ltd.

- 6.4.8 Hycrete Inc.

- 6.4.9 Interplastic Corporation

- 6.4.10 Mapei S.p.A.

- 6.4.11 Metro Cast Corporation

- 6.4.12 QGPC

- 6.4.13 Sika AG

- 6.4.14 TPP Manufacturing Sdn. Bhd.

- 6.4.15 Ulma Architectural Solutions

- 6.4.16 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment