PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848306

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848306

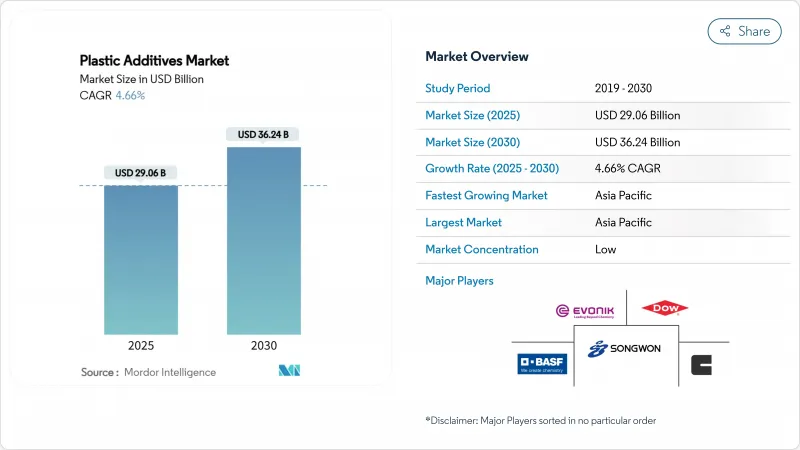

Plastic Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Plastic Additives Market size is estimated at USD 29.06 billion in 2025, and is expected to reach USD 36.24 billion by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).

Strong demand from lightweight electric-vehicle (EV) components, rapid urbanization in Asia-Pacific, and stringent global packaging rules sustain growth despite feedstock volatility and tightening chemical regulations. Asia-Pacific accounts for 54% of global revenue as China and India scale specialty-chemical output. Processing aids are the fastest-rising additive type, gaining from the move to PFAS-free chemistries, while consumer-goods applications outpace all other end-uses as brands prioritize safer ingredients. Producers are shifting portfolios toward bio-based and PFAS-free grades; BASF and Clariant finished their PFAS exits in 2024 to stay ahead of new EU and U.S. restrictions.

Global Plastic Additives Market Trends and Insights

Shift to Lightweight EV Components

Growing EV adoption is lifting demand for additives that can withstand heat, voltage, and vibration. BASF's non-halogen flame-retardant Ultramid T6000 PPA enables thinner, lighter terminal blocks and reduces corrosion risk in humid environments. Automakers currently use plastic for roughly 15% of average vehicle weight; design targets for next-generation EVs push that ratio toward 25%, magnifying additive volumes. Parallel innovations such as SABIC's NORYL GTX LMX310 resin cut charging-port carbon footprints by 30% while Avient's Hydrocerol foaming agents shave 20% from door-panel mass. As battery packs grow heavier, every kilogram saved in structural parts becomes more valuable, cementing EVs as a long-run catalyst for the plastic additives market.

Replacement of Conventional Materials

Plastics are displacing wood, steel, and concrete in construction owing to cost and longevity. BASF stabilizers extend the outdoor life of PVC roofing sheets and composite siding, reducing repaint cycles and maintenance costs. Similar shifts appear in electrical housings where flame-retardant additives allow thinner polymer casings that meet IEC standards. This material swap boosts the plastic additives market because each new polymer application needs antioxidants, UV stabilizers, and impact modifiers to match incumbent performance.

Volatility in Feedstock Prices

Tin and phosphorous prices swung sharply in 2024-2025 as mining disruptions hit Asia and Latin America, tightening the supply of organotin stabilizers and phosphite antioxidants. Smaller formulators lack hedging tools, forcing ad-hoc surcharges that erode buyer confidence and slow contract renewals. Some producers are redesigning stabilizers around calcium-zinc or hindered amine alternatives, though drop-in replacement is seldom seamless.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Compostable-Packaging Laws

- Growth of Antimicrobial Surfaces

- Phase-Out of Phthalate Plasticizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Processing aids represent the fastest-advancing category, forecast at 4.71% CAGR through 2030. Rising PFAS restrictions push converters toward new fluoro-free chemistries like Baerlocher's Baerolub AID, which improves extrusion stability without legacy environmental baggage. The "Others" group, including antioxidants, flame retardants, and impact modifiers, dominated 70% of the plastic additives market share in 2024, reflecting diverse end-use needs across packaging, construction, and mobility. Novel slip and antifog agents fitting demanding recycled-content films further widen the application scope.

Polyethylene sustained a 17% revenue share in 2024, underpinned by large packaging and pipe demand, anchoring the plastic additives market size for commodity resins. Recycled-content mandates amplify needs for compatibilizers and chain extenders that restore melt strength in rPE streams. In contrast, long constrained by recycling hurdles, polystyrene is rebounding on chemical-recycling breakthroughs that turn waste PS into ethylbenzene for sustainable aviation-fuel additives.

Polyvinyl chloride remains entrenched in window profiles and wire coatings yet faces scrutiny over residual phthalates. Innovations in bio-attributed PVC stabilizers allow producers to decouple from fossil-based feedstocks and comply with green-building labels.

The Plastic Additives Market Report Segments the Industry by Type (Lubricants, Processing Aids, Flow Improvers, Slip Additives, and More), Plastic Type (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), and More), Form (Masterbatch, Powder, and Liquid Concentrate), Application (Packaging, Consumer Goods, Construction, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific continues to anchor global volume, holding 54% of revenue in 2024 and expanding the region's plastic additives market size at 5.23% CAGR. China's stimulus for petrochemical self-reliance and India's relaxation of foreign-investment ceilings invite fresh capacity in performance stabilizers and color concentrates, securing domestic supply chains.

North America remains a mature but innovative market. U.S. automakers prioritizing EV platforms spur flame-retardant and high-flow additives for thermal-management parts, while Canada's single-use plastics ban boosts demand for compostable masterbatches that meet ASTM D6400 criteria. Mexico benefits from near-shoring, attracting extruders who source masterbatch locally to shorten lead times. The combined region posts modest growth yet commands premium margins.

Europe's policy landscape is the world's most stringent. The Packaging and Packaging Waste Regulation dictates recyclability by 2030, pushing converters to certify additive compliance through accredited labs. South America and the Middle-East and Africa are smaller in value but show healthy upside. Brazil's bio-polymer push aligns with additives that support starch and PLA blends,

- BASF

- ADEKA CORPORATION

- Albemarle Corporation

- Arkema

- Avient Corporation

- Baerlocher GmbH

- Clariant

- Croda International Plc

- Dow

- Emery Oleochemicals

- Evonik Industries AG

- Exxon Mobil Corporation

- KANEKA CORPORATION

- LANXESS

- Mitsui & Co.Plastics Ltd.

- Nouryon

- Peter Greven GmbH & Co. KG

- SABO S.p.A.

- Songwon Industrial Co. Ltd.

- Struktol Company of America, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Lightweight EV Components Stimulating High-Performance Additive Demand

- 4.2.2 Replacement of Conventional Materials by Plastic in Several Applications

- 4.2.3 Increasing Demand for Plastic Due to Rapid Urbanization and Rising Purchasing Power Among Consumers

- 4.2.4 Mandatory Compostable-Packaging Laws Accelerating Bio-Based Additive Masterbatches

- 4.2.5 Rapid Growth of Antimicrobial Surfaces in Healthcare and Food-Contact Plastics

- 4.3 Market Restraints

- 4.3.1 Volatility in Tin and Phosphorous Feedstock Prices Compressing Margins

- 4.3.2 Europe nad North America Phase-Out of Phthalate Plasticizers Reducing Addressable Volume

- 4.3.3 Regulatory Scrutiny on PFAS-Based Processing Aids Limiting Adoption

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Lubricants

- 5.1.2 Processing Aids (Fluro-polymer-based)

- 5.1.3 Flow Improvers

- 5.1.4 Slip Additives

- 5.1.5 Antistatic Additives

- 5.1.6 Pigment Wetting Agents

- 5.1.7 Filler Dispersants

- 5.1.8 Antifog Additives

- 5.1.9 Plasticizers

- 5.1.10 Other Types (Blowing Agent, Anti-blocking Agents, Coupling agents, etc.)

- 5.2 By Plastic Type

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyvinyl Chloride (PVC)

- 5.2.4 Polystyrene (PS)

- 5.2.5 Polyethylene Terephthalate (PET)

- 5.2.6 Polycarbonate (PC)

- 5.2.7 Polyamides (PA)

- 5.2.8 Other Plastic Types

- 5.3 By Form

- 5.3.1 Masterbatch

- 5.3.2 Powder

- 5.3.3 Liquid Concentrate

- 5.4 By Application

- 5.4.1 Packaging

- 5.4.2 Consumer Goods

- 5.4.3 Construction

- 5.4.4 Automotive

- 5.4.5 Others (Medical, 3D Printing)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Nordics

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments}

- 6.4.1 BASF

- 6.4.2 ADEKA CORPORATION

- 6.4.3 Albemarle Corporation

- 6.4.4 Arkema

- 6.4.5 Avient Corporation

- 6.4.6 Baerlocher GmbH

- 6.4.7 Clariant

- 6.4.8 Croda International Plc

- 6.4.9 Dow

- 6.4.10 Emery Oleochemicals

- 6.4.11 Evonik Industries AG

- 6.4.12 Exxon Mobil Corporation

- 6.4.13 KANEKA CORPORATION

- 6.4.14 LANXESS

- 6.4.15 Mitsui & Co.Plastics Ltd.

- 6.4.16 Nouryon

- 6.4.17 Peter Greven GmbH & Co. KG

- 6.4.18 SABO S.p.A.

- 6.4.19 Songwon Industrial Co. Ltd.

- 6.4.20 Struktol Company of America, LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Rising Research Activities Research to Develop Bio-based Plastics