PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910651

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910651

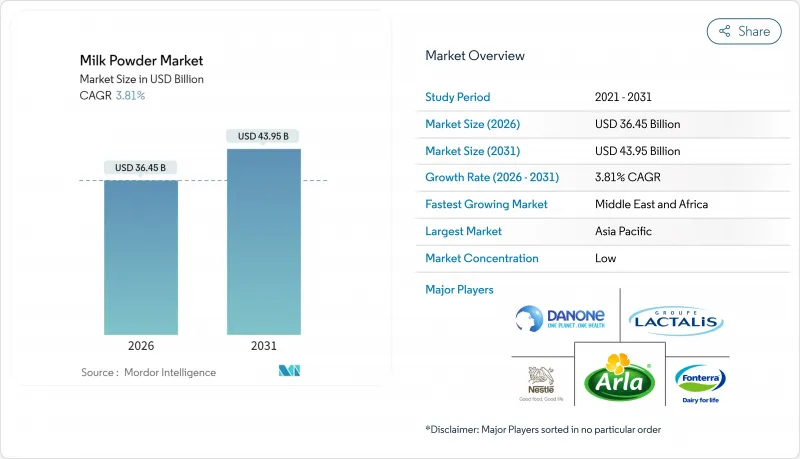

Milk Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The milk powder market is expected to grow from USD 35.11 billion in 2025 to USD 36.45 billion in 2026 and is forecast to reach USD 43.95 billion by 2031 at 3.81% CAGR over 2026-2031.

Milk powder, a dehydrated form of liquid milk, is extensively utilized across various industries, including infant formula, confectionery, bakery products, beverages, and nutritional supplements. Its long shelf life, ease of storage, and transportation advantages make it a preferred choice among manufacturers and consumers alike. The market's growth is primarily driven by the increasing demand for convenient and long-lasting dairy products, particularly in regions with limited access to fresh milk. Rising health consciousness among consumers has further fueled the demand for milk powder, especially for fortified and organic variants that cater to specific dietary needs. The growing adoption of milk powder in emerging economies, where it serves as a cost-effective alternative to liquid milk, is another significant factor contributing to market expansion. Additionally, the food and beverage industry is increasingly incorporating milk powder into its products to enhance nutritional value and improve product stability

Global Milk Powder Market Trends and Insights

Surging demand for infant fomrula

Global infant formula demand intensifies as regulatory frameworks evolve to support market resilience and nutritional adequacy. In 2025, the FDA unveiled its Long-Term National Strategy aimed at bolstering the resilience of the U.S. infant formula market. The strategy introduces fresh measures to prevent contamination and offers incentives to manufacturers, encouraging diversification in light of recent supply chain disruptions. These measures are designed to ensure a more robust and reliable supply chain, minimizing the risk of shortages and enhancing consumer confidence. Simultaneously, technological advancements in premium formulations are making waves. A case in point is Nestle's debut of NAN Sinergity, which boasts six human milk oligosaccharides. This move underscores how a super-premium positioning not only commands higher margins but also caters to specific nutritional needs, addressing the growing demand for specialized infant nutrition. The blend of regulatory backing and innovative strides is fueling a demand growth that's not just tethered to traditional demographic influences but also driven by evolving consumer preferences and health-conscious choices.

Population growth and urbanization

As urbanization rises in emerging markets, it fuels a structural demand growth, with increased access to packaged dairy products and a boost in disposable income steering choices towards premium nutrition. According to a UN-Habitat report, Asia is home to 54% of the world's urban population, amounting to over 2.2 billion individuals. Projections suggest that by 2050, Asia's urban populace will grow by an additional 1.2 billion, reflecting a 50% increase. This rapid urbanization in the Asia-Pacific is not just creating dense consumer hubs but also bolstering infrastructure, paving the way for cold-chain distribution networks vital for penetrating the milk powder market. Urban consumers, especially in regions where fresh milk faces availability challenges due to infrastructural constraints, are showing a pronounced willingness to pay more for convenience and nutritional advantages. This demographic evolution lays down robust growth foundations, transcending fleeting economic cycles and fostering predictable demand patterns. Such patterns, in turn, bolster long-term capacity planning and investment strategies.

Lactose intolerance and allergies

Milk powder faces significant challenges due to lactose intolerance and milk allergies, which act as major restraints in this market. According to the National Institutes of Health (NIH), approximately 68% of the global population is affected by lactose intolerance . This condition limits the consumption of dairy-based products, including milk powder, as individuals with lactose intolerance experience difficulty digesting lactose, a sugar found in milk and dairy products. Furthermore, milk allergies, particularly prevalent among children, further reduce the potential consumer base for milk powder. The Frontiers Report 2024 identifies Cow's Milk Allergy (CMA) as one of the most common food allergies in children, with a prevalence of 1.8% among children aged 1 to 5 in the United States . These health concerns have led to a growing consumer preference for non-dairy alternatives, such as plant-based milk powders, which are perceived as healthier and more suitable for individuals with lactose intolerance or milk allergies. Additionally, regulatory bodies worldwide are increasingly emphasizing the need for clear and accurate labeling of allergens in food products. This regulatory focus adds to the operational challenges for manufacturers, as they must ensure compliance with stringent labeling requirements while maintaining product quality and market competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in dairy processing technology boost milk powder quality and efficiency

- Use in processed foods such as ready meals, desserts, and beverages

- Volatile global dairy commodity prices caused by climate-linked supply shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, dairy milk powder dominated the milk powder market, accounting for a significant 62.68% share. This dominance can be attributed to its widespread use in various applications, including infant formula, bakery products, confectionery, and beverages. Dairy milk powder's long shelf life, ease of transportation, and nutritional benefits make it a preferred choice among consumers and manufacturers alike. Additionally, the segment benefits from the growing demand for protein-enriched diets and the increasing consumption of ready-to-eat and processed foods. Emerging markets, particularly in Asia-Pacific, are witnessing a surge in demand for dairy milk powder due to rising disposable incomes and changing dietary patterns. Furthermore, advancements in processing technologies and the availability of fortified dairy milk powders are expected to sustain the segment's growth during the forecast period.

On the other hand, non-dairy alternatives, such as plant-based milk powders, are experiencing rapid growth, with a projected CAGR of 3.92% through 2031. This growth is driven by rising consumer preferences for vegan and lactose-free products, along with increasing awareness of environmental sustainability. Plant-based milk powders, derived from sources like soy, almond, and oat, are gaining traction due to their health benefits and suitability for individuals with dietary restrictions. The segment's expansion is further supported by innovation in product offerings, such as flavored and fortified variants, which cater to diverse consumer preferences. Additionally, the growing adoption of plant-based diets, supported by marketing campaigns and endorsements from health and wellness influencers, is fueling demand. The increasing availability of plant-based milk powders in mainstream retail channels and their incorporation into various food and beverage applications are expected to drive further growth in this segment.

The Milk Powder Market Report is Segmented by Type (Dairy Milk Powder, Non-Dairy/Plant-Based Milk Powder), Packaging Format (Flexible Pouches, Cans and Tins, Bulk Bags, Single-Serve Sachets), Distribution Channel (Retail, Foodservice, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region secures a dominant 41.62% market share in the milk powder market, driven by several key factors. The region's demographic expansion, coupled with rising disposable incomes, has significantly increased consumer purchasing power, enabling greater access to packaged dairy products, including milk powder. Urbanization trends further amplify this demand, as urban consumers increasingly prefer convenient and shelf-stable dairy options. Additionally, China's regulatory landscape is undergoing significant changes, with the introduction of new national food safety standards and restrictions on the use of milk powder in shelf-stable milk. While these regulations create short-term disruptions, they also elevate quality standards, benefiting producers who comply with these stringent requirements and positioning them for long-term growth in the market.

The Middle East and Africa region is experiencing the fastest growth in the milk powder market, with a projected CAGR of 4.90% through 2031. This rapid growth is underpinned by ongoing economic development and substantial improvements in infrastructure, which are critical for the efficient distribution and consumption of dairy products. As disposable incomes rise and urbanization progresses, the demand for milk powder and other dairy products is expected to grow steadily. Furthermore, government initiatives aimed at enhancing food security and promoting local dairy production are likely to support the market's expansion in this region, creating opportunities for both domestic and international players.

North America and Europe exhibit stable growth patterns, reflecting the maturity of their respective milk powder markets. These regions benefit from well-established supply chains, high consumer awareness, and consistent demand for dairy products. However, growth opportunities remain limited compared to emerging markets. In contrast, South America presents a promising landscape for the milk powder market, driven by economic development and the expansion of the middle-class population. As consumers in this region increasingly seek nutritional enhancement products, the demand for milk powder is expected to rise. Additionally, the region's growing focus on improving dairy production capabilities and expanding export opportunities further supports market growth.

- Nestle S.A.

- Fonterra Co-operative Group Ltd

- Danone S.A.

- Groupe Lactalis

- Arla Foods amba

- Saputo Inc.

- Royal FrieslandCampina N.V.

- Dairy Farmers of America, Inc.

- Inner Mongolia Yili Industrial Group Co., Ltd.

- Gujarat Cooperative Milk Marketing Federation (Amul)

- Abbott Laboratories

- Morinaga Milk Industry Co.

- Hochdorf Holding AG

- Westland Milk Products

- Valio Oy

- Valley Milk LLC

- Royal A-ware Food Group

- Almarai Company

- Olam Food Ingredients

- Parag Milk Foods Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for infant fomrula

- 4.2.2 Population growth and urbanization

- 4.2.3 Advancements in dairy processing technology boost milk powder quality and efficiency

- 4.2.4 Use in processed foods such as ready meals, desserts, and beverages

- 4.2.5 Research and development investments in recombined UHT dairy beverages fueling industrial demand

- 4.2.6 High-protein lifestyle trend boosting skim milk powder in sports nutrition category

- 4.3 Market Restraints

- 4.3.1 Lactose intolerance and allergies

- 4.3.2 Volatile global dairy commodity prices caused by climate-linked supply shocks

- 4.3.3 Stringent EU antibiotic residue limits restricting imports of certain milk powders

- 4.3.4 Storage and transportation challenges hinder milk powder distribution

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Dairy Milk Powder

- 5.1.1.1 Whole Milk Powder (WMP)

- 5.1.1.2 Skim Milk Powder (SMP)

- 5.1.1.3 Others (Fat-Filled Milk Powder, A2 and Specialty Nutritional Powders, etc.)

- 5.1.2 Non-Dairy/Plant-Based Milk Powder

- 5.1.2.1 Soy Milk Powder

- 5.1.2.2 Almond Milk Powder

- 5.1.2.3 Coconut Milk Powder

- 5.1.2.4 Oat and Other Cereal-Based Powders

- 5.1.1 Dairy Milk Powder

- 5.2 By Distribution Channel

- 5.2.1 Retail

- 5.2.1.1 Supermarkets/Hypermarkets

- 5.2.1.2 Convenience and Grocery Stores

- 5.2.1.3 Online Retail

- 5.2.1.4 Other Distribution Channel

- 5.2.2 Foodservice

- 5.2.3 Industrial

- 5.2.3.1 Infant and Follow-on Formula

- 5.2.3.2 Bakery and Confectionery

- 5.2.3.3 Dairy-based Beverages and Recombination

- 5.2.3.4 Nutritional and Sports Supplements

- 5.2.3.5 Others (Ready-Made Meals, cosmetics, etc.)

- 5.2.1 Retail

- 5.3 By Packaging Format

- 5.3.1 Flexible Pouches

- 5.3.2 Cans and Tins

- 5.3.3 Bulk Bags

- 5.3.4 Single-Serve Sachets

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Columbia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Egypt

- 5.4.5.5 Nigeria

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 Fonterra Co-operative Group Ltd

- 6.4.3 Danone S.A.

- 6.4.4 Groupe Lactalis

- 6.4.5 Arla Foods amba

- 6.4.6 Saputo Inc.

- 6.4.7 Royal FrieslandCampina N.V.

- 6.4.8 Dairy Farmers of America, Inc.

- 6.4.9 Inner Mongolia Yili Industrial Group Co., Ltd.

- 6.4.10 Gujarat Cooperative Milk Marketing Federation (Amul)

- 6.4.11 Abbott Laboratories

- 6.4.12 Morinaga Milk Industry Co.

- 6.4.13 Hochdorf Holding AG

- 6.4.14 Westland Milk Products

- 6.4.15 Valio Oy

- 6.4.16 Valley Milk LLC

- 6.4.17 Royal A-ware Food Group

- 6.4.18 Almarai Company

- 6.4.19 Olam Food Ingredients

- 6.4.20 Parag Milk Foods Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK