PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849812

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849812

Inductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

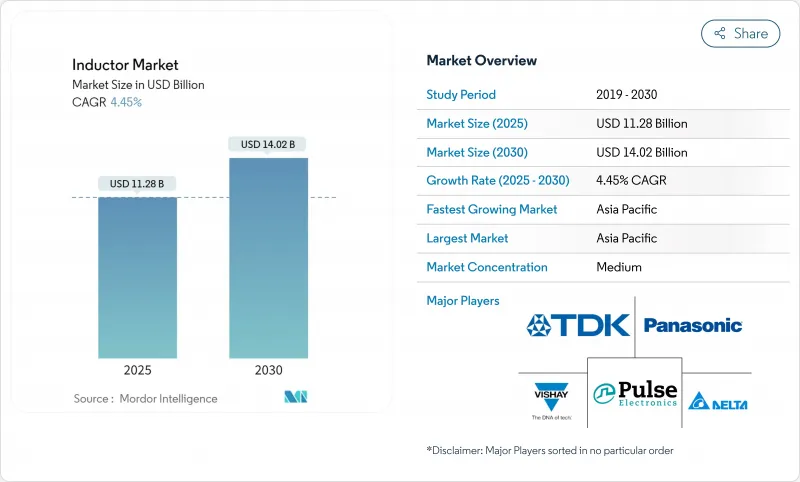

The inductors market size is estimated at USD 11.28 billion in 2025 and is forecast to reach USD 14.02 billion by 2030, expanding at a 4.45% CAGR over the period.

Electrification of vehicles, continued 5G base-station build-outs, and power-dense data-center hardware form the bedrock of growth even as discrete components face design-in pressure from integrated passive devices. Demand is shifting from high-volume commodity coils toward purpose-built parts optimized for high-frequency switching, thermally challenging automotive powertrains, and ultra-compact wearables. Automotive qualification (AEC-Q200) has moved from differentiator to entry requirement, surface-mount power inductors dominate new designs, and metal-alloy cores are steadily displacing ferrite in high-current rails. Supply-chain diversification and regionalization-especially out of mainland China-are rewriting the global production footprint as vendors seek resilience rather than the lowest landed cost.

Global Inductor Market Trends and Insights

Rising demand for miniaturized consumer electronics

Ultra-compact wearables, hearables, and next-generation smartphones rely on power-efficient passives that occupy ever-smaller PCB footprints. Breakthroughs such as TDK's 0.25 X 0.125 X 0.2 mm chip addressed this constraint by delivering space savings near 50% without sacrificing inductance values, typically 0.6-3.6 nH. Design wins migrate from smartphones to AR glasses and sensor-rich health monitors, sustaining the 42.4% 2024 consumer-electronics share even as handset replacement cycles lengthen. Vendors differentiate through lithographic patterning, fine-powder ferrites, and multilayer sintering that keep direct current resistance low while maintaining Q-factor.

Electrification of automotive sector (EVs)

Each battery-electric vehicle integrates more than 100 inductors for DC-DC converters, onboard chargers, and traction inverters, sharply higher than the sub-20 count typical in smartphones. AEC-Q200 compliance elevates testing for vibration, temperature shock, and humidity, raising barriers to entry and channeling share to qualified suppliers. Silicon-carbide inverters operate above 40 kHz, demanding metal-alloy or powder-molded cores that maintain inductance under elevated flux density. Global automakers' parallel pushes in China, Europe, and the United States sustain a 9.2% segment CAGR through 2030.

Volatility in copper and ferrite prices

Copper comprises the winding while ferrite or alloy powders form the magnetic path, so any spike ripples straight to cost of goods sold. Market observers warn that mine supply lags the electrification super-cycle, risking structural deficits after 2030. Manufacturers respond with recycled metal initiatives-TDK's new CLT32 series uses more than 50% reclaimed feedstock-and with long-term offtake agreements. Smaller fabs lacking scale for hedging remain exposed, squeezing margins and slowing capacity adds.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of 5G and high-speed communications

- Growth in renewable energy and power electronics

- Global supply-chain disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power inductors delivered 42.1% of inductors market share in 2024, an advantage anchored in voltage-regulation modules, DC-DC converters, and onboard chargers. Within the inductors market size for high-frequency designs, the sub-segment climbs at 6.3% CAGR to 2030 on the back of millimeter-wave 5G nodes. Wire-wound formats dominate automotive 48 V rails, whereas thin-film structures serve handset RF filters. Coupled coils improve transient response in multiphase VRMs that feed GPUs, and demand scales with AI-server shipments. Molded products gain ground where vibration resistance, thermal conductivity, and EMI shielding trump raw cost. Vendors layer in automatic optical inspection and X-ray process control to sustain tight inductance tolerances.

Second-generation metal-powder molding compounds from Resonac cut core losses above 2 MHz, enabling buck converters to shrink magnetics while preserving >=95% efficiency. As silicon-carbide MOSFET gate charges fall, switching frequencies climb, and inductor volumetric density becomes a primary design constraint. Emerging topologies such as dual-active-bridge converters for bidirectional battery packs further amplify the need for low-loss inductors with saturation currents above 60 A.

Ferrite continued to own 54.7% of 2024 revenue thanks to its balance of cost and permeability, yet the metal-alloy slice is forecast to grow 5.4% per year. In the inductors market, metal-alloy powder cores tolerate flux densities beyond 1 T, enabling coil counts to fall and inductance drift over temperature to shrink. Nanocrystalline strip products, such as Proterial's FINEMET, post insertion losses below 200 mW at 100 kHz, appealing to automotive bidirectional on-board chargers. Air-core coils persist in GHz RF paths where magnetic materials would introduce eddy-current loss. Ceramic substrates gain purchase in miniaturized Bluetooth modules that juggle thermal limits and strict form-factor caps. Manufacturers calibrate sintering curves and particle sizes to dial in B-H loops tailored to final applications.

Reliability screening tightens as core composition complexity grows; partial-discharge and frequency-swept impedance tests now complement legacy saturation-current checks. A move toward lifecycle carbon accounting drives interest in recycled iron powders and closed-loop ferrite reclaim systems, merging environmental goals with hedging against virgin-material price swings.

The Inductor Market Report is Segmented by Type (Power, RF/High Frequency, and More), Core Material (Air/Ceramic Core, Ferrite Core, and More), Mounting Technique (Surface-Mount Technology, and More), Shielding (Shielded and Unshielded), Inductance (Fixed, Variable/Tunable), End-User Vertical (Automotive, Aerospace and Defense, Communications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for inductors with significant growth potential. The region's market is characterized by increasing investments in industrial automation and the growing adoption of smart city initiatives. Latin America has shown particular promise with its expanding telecommunications infrastructure and increasing adoption of IoT technologies. The Middle Eastern market is driven by automation in the oil and gas sector, along with significant investments in renewable energy projects. The region's automotive sector, particularly in the UAE and Saudi Arabia, is showing increased interest in electric and hybrid vehicles, creating new opportunities for inductor manufacturers. The market is also benefiting from increasing investments in manufacturing capabilities and the growing adoption of advanced electronics in various industries. The development of smart infrastructure and the increasing focus on energy efficiency are creating additional demand for various types of inductors across the region.

- TDK Corporation

- Murata Manufacturing Co. Ltd

- Vishay Intertechnology Inc.

- Panasonic Holdings Corporation

- Taiyo Yuden Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Pulse Electronics (Yageo Corporation)

- Delta Electronics Inc.

- Coilcraft Inc.

- Bourns Inc.

- Wurth Elektronik GmbH & Co. KG

- Sumida Corporation

- TE Connectivity Ltd

- Chilisin Electronics Corporation

- AVX Corporation (Kyocera AVX)

- Bel Fuse Inc.

- Sunlord Electronics Co. Ltd

- Eaton Corporation (Coiltronics)

- KEMET Corporation (Yageo)

- API Delevan Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for miniaturized consumer electronics

- 4.2.2 Electrification of automotive sector (EVs)

- 4.2.3 Expansion of 5G and high-speed communications

- 4.2.4 Growth in renewable energy and power electronics

- 4.2.5 Embedded inductors in AI servers and IoT modules

- 4.2.6 High-frequency power converters in data centers

- 4.3 Market Restraints

- 4.3.1 Volatility in copper and ferrite prices

- 4.3.2 Global supply-chain disruptions

- 4.3.3 Thermal management issues in embedded inductors

- 4.3.4 Integrated passive devices eroding discrete demand

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Power Inductors

- 5.1.2 RF/High-Frequency Inductors

- 5.1.3 Coupled Inductors

- 5.1.4 Multilayer Inductors

- 5.1.5 Thin-Film Inductors

- 5.1.6 Molded/Wire-wound Inductors

- 5.2 By Core Material

- 5.2.1 Air/Ceramic Core

- 5.2.2 Ferrite Core

- 5.2.3 Iron and Metal-Alloy Core

- 5.2.4 Nanocrystalline and Amorphous Core

- 5.3 By Mounting Technique

- 5.3.1 Surface-Mount Technology (SMT)

- 5.3.2 Through-Hole Technology (THT)

- 5.3.3 Embedded/Integrated PCB Inductors

- 5.4 By Shielding

- 5.4.1 Shielded

- 5.4.2 Unshielded

- 5.5 By Inductance

- 5.5.1 Fixed Inductors

- 5.5.2 Variable/Tunable Inductors

- 5.6 By End-user Vertical

- 5.6.1 Automotive

- 5.6.2 Aerospace and Defense

- 5.6.3 Communications and 5G Infrastructure

- 5.6.4 Consumer Electronics and Computing

- 5.6.5 Industrial and Power

- 5.6.6 Healthcare and Medical Devices

- 5.6.7 Renewable Energy Systems

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 India

- 5.7.3.5 Taiwan

- 5.7.3.6 South East Asia

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Egypt

- 5.7.5.2.3 Nigeria

- 5.7.5.2.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TDK Corporation

- 6.4.2 Murata Manufacturing Co. Ltd

- 6.4.3 Vishay Intertechnology Inc.

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 Taiyo Yuden Co. Ltd

- 6.4.6 Samsung Electro-Mechanics Co. Ltd

- 6.4.7 Pulse Electronics (Yageo Corporation)

- 6.4.8 Delta Electronics Inc.

- 6.4.9 Coilcraft Inc.

- 6.4.10 Bourns Inc.

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Sumida Corporation

- 6.4.13 TE Connectivity Ltd

- 6.4.14 Chilisin Electronics Corporation

- 6.4.15 AVX Corporation (Kyocera AVX)

- 6.4.16 Bel Fuse Inc.

- 6.4.17 Sunlord Electronics Co. Ltd

- 6.4.18 Eaton Corporation (Coiltronics)

- 6.4.19 KEMET Corporation (Yageo)

- 6.4.20 API Delevan Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment