PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849827

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849827

Automotive Anti Lock Braking System And Electronic Stability Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

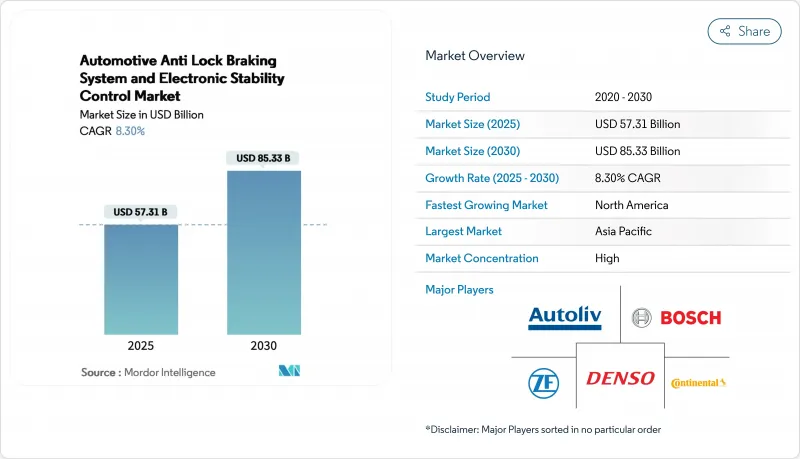

The Automotive Anti Lock Braking System And Electronic Stability Control Market size is estimated at USD 57.31 billion in 2025, and is expected to reach USD 85.33 billion by 2030, at a CAGR of 8.30% during the forecast period (2025-2030).

Growth is anchored in mandatory safety regulations, electrified platforms that favor brake-by-wire designs, and the steady rebound of global vehicle production. Regulators in the European Union, the United States, India, and China now regard ABS as foundational to wider active-safety suites, prompting OEMs to embed ABS into virtually every new vehicle segment. Suppliers are capitalizing on these mandates by bundling ABS with advanced driver assistance controllers, while insurers reward fleets and consumers that opt for active-safety packages. Alongside rising production volumes, electric two-wheelers and battery electric cars are creating the fastest incremental demand as single-channel and electric ABS architectures gain popularity.

Global Automotive Anti Lock Braking System And Electronic Stability Control Market Trends and Insights

Mandatory Safety Regulations Driving Global ABS Adoption

Stringent policies such as UN R78 for motorcycles, FMVSS-122 in the United States, and AIS-150 in India are pushing ABS fitment toward 100% in new vehicles. The U.S. National Highway Traffic Safety Administration's rule requiring automatic emergency braking by 2029 makes ABS core to achieving compliance. Europe already enforces motorcycle ABS on scooters above 125 cc, influencing ASEAN nations that rely heavily on two-wheelers. India mirrored this trend, compelling suppliers to release cost-optimized single-channel solutions. UN ESCAP estimates that motorcycle ABS can cut fatalities by 31% unescap.org, reinforcing regulators' confidence.

Rising Global Vehicle Production Expanding ABS Market Footprint

Post-pandemic manufacturing recovery is most pronounced in Asia Pacific, where China returned to full-scale capacity and India's two-wheeler output set new highs in 2024. Increased unit volumes translate directly into greater ABS demand, especially as ABS migrates from optional to standard equipment. Bosch notes that advanced ABS can prevent 40% of two-wheeler crashes, a statistic resonating with consumers and policymakers.

Cost Barriers Limiting Penetration in Price-Sensitive Markets

ABS price premiums remain challenging for low-cost motorcycles and entry-level cars in India, Indonesia, and Brazil, where a few USD can sway purchase decisions. OEM margins average 7.2%, while suppliers hover near 5.5%, limiting room to absorb ABS costs. Tier-1 vendors therefore re-engineer hydraulic units to remove valving complexity, adopt shared ECUs, and localize production to achieve viable price points.

Other drivers and restraints analyzed in the detailed report include:

- Growing Insurance Incentives for Active-Safety Equipped Vehicles

- Electrification Platforms Transforming ABS Architecture

- Semiconductor Supply Constraints Impacting Production Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars anchored the automotive anti-lock braking system market in 2024, delivering 47.15% revenue thanks to mandatory fitment in Europe, China, and North America. Stable car demand, paired with increasingly sophisticated driver assistance packages, ensures a consistent revenue base. The segment will grow in tandem with ADAS penetration, though at a slower pace than two-wheelers. The automotive anti-lock braking system market size for passenger cars is projected to expand at 8.10% CAGR, supported by OEM integration of brake control with lane-keeping and adaptive cruise functions.

Electric two-wheelers inject faster momentum at 15.40% CAGR. Mandates in India and Europe require ABS on motorcycles above 125 cc, propelling single-channel architectures that weigh and cost less than four-wheel solutions. Electric scooters popular in China and Southeast Asia favor regenerative braking, forcing suppliers to fuse ABS algorithms with energy-recovery logic. Bosch forecasts mass-market rider assistance deployment by 2026, underscoring regional appetite for active safety on two-wheelers.

Electronic control units remained the largest component segment in 2024 at 33.55% revenue, a share lifted by rising computational needs. AI firmware now interprets wheel-speed data, road friction coefficients, and vehicle load in real time, enabling predictive braking. This functionality drives a 12.10% CAGR outlook for ECUs, well ahead of other components. Wheel-speed sensors follow in value, benefiting from solid-state designs that withstand vibration on two-wheelers and heavy trucks.

Hydraulic control units face weight and efficiency redesigns for battery electric vehicles, where every kilogram impacts range. Valves and actuators exploit lightweight aluminum housings and advances in mechatronics to cut response times. As AI moves onto central domain controllers, ECU suppliers adapt by offering over-the-air update capabilities to maintain cyber compliance, mitigating one of the key restraints on software-defined braking.

The Automotive Anti-Lock Braking System Market is Segmented by Vehicle Type (Two-Wheelers, and More), Component (Electronic Control Unit (ECU), and More), ABS Type (4-Channel, and More), Technology (Hydraulic ABS, and More), End User (OEM-Fitment, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific leads the automotive anti-lock braking system market with 36.55% market share, propelled by China's production scale and India's regulatory surge. India's ABS mandate on motorcycles is growing significantly, with suppliers establishing local ECU plants to avoid import tariffs. China pairs ABS with compulsory electronic stability control on passenger cars, keeping domestic tier-1 suppliers in lockstep with multinational competitors. Japanese and South Korean OEMs integrate ABS with proprietary hybrid systems, sharpening regional technology leadership.

North America expands at highest CAGR at 13.60% by 2030, with U.S. demand buoyed by upcoming AEB rules and Canada aligning with FMVSS standards. Commercial fleet retrofits gain traction where insurers offer multiline discounts. Mexico's assembly plants, serving export markets, pre-install ABS to satisfy both U.S. and EU homologation. Smaller yet growing markets in the Middle East, Africa, and South America witness Brazil mandating ABS on all new motorcycles, and Saudi Arabia incentivizing fleets that adopt advanced safety packages.

Europe follows, underpinned by the EU General Safety Regulation that obliges ABS on all new vehicles and positions it within broader AEB validation. Germany remains the region's innovation hub, with suppliers piloting ABS-based harsh-brake data to improve road-friction mapping. Gapwaves notes that extra radar sensors required for AEB complement ABS signals for redundancy. Eastern European assembly plants extend adoption to entry-level cars, ensuring uniform safety standards.

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Mando Corporation

- Hyundai Mobis Co., Ltd.

- Hitachi Astemo, Ltd.

- Brembo S.p.A.

- Knorr-Bremse AG

- WABCO (ZF CVCS)

- Haldex AB

- Nissin Kogyo Co., Ltd.

- ADVICS Co., Ltd.

- Aptiv PLC

- Delphi Technologies (BorgWarner)

- Veoneer Holding LLC

- Autoliv Inc.

- BWI Group

- Maruichi Machine

- Federal-Mogul Motorparts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory safety regulations (UN R78, FMVSS-122, AIS-150)

- 4.2.2 Rising global passenger-car & 2-wheeler production rebounding post-COVID

- 4.2.3 Growing insurance incentives for active-safety equipped vehicles

- 4.2.4 Electrification platforms requiring brake-by-wire integration

- 4.2.5 Rapid retrofit demand in used-vehicle fleets for telematics-based UBI

- 4.2.6 Tier-1 suppliers bundling ABS with ADAS domain controllers

- 4.3 Market Restraints

- 4.3.1 High BOM cost for low-end 2-wheelers & emerging-market cars

- 4.3.2 Integration complexity with legacy hydraulic architectures

- 4.3.3 Semiconductor supply-chain constraints post-2023

- 4.3.4 Cyber-security certification delays for software-defined braking

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Two-Wheelers

- 5.1.2 Passenger Cars

- 5.1.3 Light Commercial Vehicles

- 5.1.4 Medium and Heavy Commercial Vehicles

- 5.2 By Component

- 5.2.1 Electronic Control Unit (ECU)

- 5.2.2 Hydraulic Control Unit

- 5.2.3 Wheel Speed Sensors

- 5.2.4 Valves & Actuators

- 5.3 By ABS Type

- 5.3.1 4-Channel

- 5.3.2 3-Channel

- 5.3.3 Single-Channel (Motorcycle)

- 5.4 By Technology

- 5.4.1 Hydraulic ABS

- 5.4.2 Electric ABS

- 5.4.3 Pneumatic ABS

- 5.5 By End User

- 5.5.1 OEM-Fitment

- 5.5.2 Aftermarket Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Turkey

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 DENSO Corporation

- 6.4.5 Mando Corporation

- 6.4.6 Hyundai Mobis Co., Ltd.

- 6.4.7 Hitachi Astemo, Ltd.

- 6.4.8 Brembo S.p.A.

- 6.4.9 Knorr-Bremse AG

- 6.4.10 WABCO (ZF CVCS)

- 6.4.11 Haldex AB

- 6.4.12 Nissin Kogyo Co., Ltd.

- 6.4.13 ADVICS Co., Ltd.

- 6.4.14 Aptiv PLC

- 6.4.15 Delphi Technologies (BorgWarner)

- 6.4.16 Veoneer Holding LLC

- 6.4.17 Autoliv Inc.

- 6.4.18 BWI Group

- 6.4.19 Maruichi Machine

- 6.4.20 Federal-Mogul Motorparts

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment