PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849843

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849843

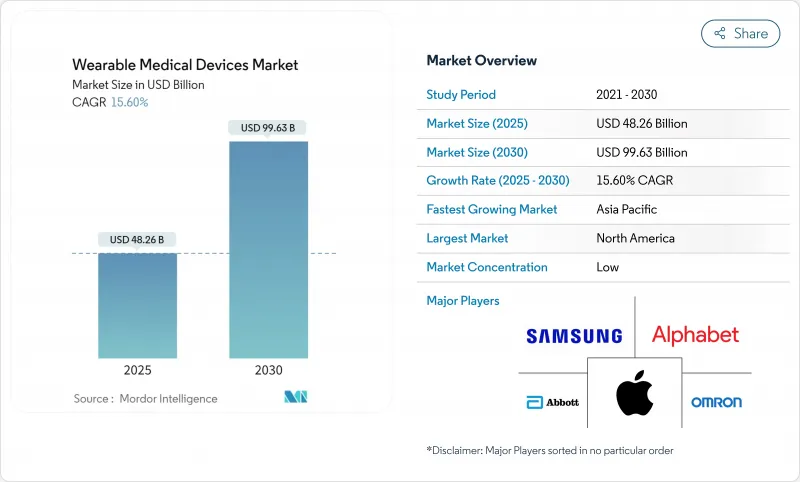

Wearable Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The wearable medical devices market size is estimated to be USD 48.26 billion in 2025 and is projected to reach USD 99.63 billion by 2030, registering a 15.60% CAGR over the forecast period.

Growth accelerates as regulatory bodies create fast-track pathways for connected diagnostics and expand Medicare reimbursement that recognizes wearable data within clinical decision support. Continuous innovation in biosensors, battery miniaturization, and cloud interoperability strengthens clinical adoption, while consumer-tech ecosystems such as Apple HealthKit amplify user engagement. Strategic partnerships between traditional med-tech firms and software leaders unlock new intervention-capable product lines, and Asia-Pacific manufacturing clusters support lower production costs that enable wider geographic reach. Cyber-security mandates and physician skepticism about consumer-grade accuracy temper momentum, yet clearer regulatory guidance and payer acceptance continue to translate pilot projects into broad hospital programs.

Global Wearable Medical Devices Market Trends and Insights

Rising Prevalence of Chronic Diseases & Home-Healthcare Demand

Population aging and value-based care reimbursement accelerate chronic-disease programs that rely on continuous monitoring to reduce unplanned admissions. Commercial continuous glucose monitors such as Abbott's Freestyle Libre allow diabetes patients to self-manage while providing clinicians with real-time trend data. Governments promote "hospital-at-home" models that require validated biosensors for round-the-clock vitals, making the wearable medical devices market essential to cost containment. Early anomaly alerts improve therapeutic outcomes and lower emergency department utilization. Asia-Pacific, where the elderly population rises fastest, demonstrates strong demand for fall-detection and cardiac-rhythm patches. These structural forces underpin a long-run uplift of roughly 3.5 percentage points in projected CAGR.

Increasing Adoption of AI-Enabled Biosensors for Disease-Specific Monitoring

AI embedded in flexible electronics shifts wearables from generic wellness trackers to diagnostic platforms capable of 98% arrhythmia-detection sensitivity in FDA-cleared algorithms. Nanowear's SimpleSense-BP captures dozens of biomarkers on a textile substrate to deliver clinical-grade blood-pressure readings. Edge-computing designs from the University of Hong Kong process data locally, preserving privacy and cutting cloud latency. Machine learning refines photoplethysmography to near-clinical accuracy for SpO2 and blood pressure. Predictive analytics flag exacerbations hours before symptomatic onset, transitioning care paradigms from reactive to proactive. These capabilities raise physician confidence and spur procurement across cardiology and neurology units.

Cyber-Security & Data-Privacy Compliance Costs

Healthcare ranks among the most targeted sectors for ransomware, prompting regulators to tighten requirements. The FDA now mandates software bill-of-materials disclosures and lifecycle patch plans in pre-market submissions, adding as much as USD 1 million in extra development outlays for complex wearables. EU GDPR rules require explicit consent and right-to-forget protocols, forcing vendors to invest in encryption, key management, and audit trails. Smaller innovators, though technically agile, often encounter capital constraints when meeting enterprise-grade security benchmarks. Delays in certification can defer commercialization and erode competitive positioning.

Other drivers and restraints analyzed in the detailed report include:

- Growing Reimbursement for Remote Patient-Monitoring Programs

- Integration with Consumer-Tech Ecosystems Boosting User Engagement

- Fragmented Device-Data Standards Hindering Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic and monitoring devices accounted for 63.78% of the wearable medical devices market size in 2024, buoyed by widespread heart-rate, blood-pressure, and continuous glucose monitors that satisfy reimbursable chronic-care pathways. The segment's leadership reflects mature sensor accuracy and broad regulatory clearances. Vital-sign patches remain preferred in cardiology wards, while overnight oximetry wearables support sleep-apnea screening. Closed-loop glucose systems received strong uptake after CMS broadened coverage, anchoring continued growth across endocrinology departments.

Therapeutic wearables, although smaller today, are advancing at a projected 15.93% CAGR as form factors evolve from passive patches to active drug-delivery or neuromodulation devices. Heat-therapy pads equipped with AI-guided exercise libraries illustrate convergence between physiotherapy and consumer convenience. Implantable EEG monitors such as Epiminder's Minder extend continuous seizure tracking outside clinical settings, signalling the market's shift toward intervention. These breakthroughs underscore how the wearable medical devices market size for therapeutics will expand markedly through 2030 as algorithms personalize dosage or stimulus intensity in real time.

Adults aged 18-60 represented 61.45% of the wearable medical devices market share in 2024, driven by chronic-disease incidence in working populations and employer wellness incentives. Devices balance lifestyle insights with FDA-cleared metrics, satisfying both preventive health and clinical monitoring. Seniors embrace simplified user interfaces and fall-detection smart clothing that embed motion sensors in natural fabrics, boosting compliance among less tech-savvy users.

Pediatric adoption, though smaller, carries a 16.46% forecast CAGR. FDA clearance for the Sonu Band, a drug-free nasal-congestion therapy for children over 12, exemplifies regulatory openness to child-specific designs. Parents value non-invasive vitals patch kits that transmit alerts to smartphones, reducing clinic visits. Gaming-style feedback and colorful form factors entice younger users, while school tele-health pilots showcase early success. Taken together, youth-focused innovation enlarges the wearable medical devices market size in segments traditionally underserved by medical technology.

The Wearable Medical Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices [Vital-Sign Monitoring Devices and More] and More), Age Group (Under 18 and More), Distribution Channel (Online and Offline), Application (Sports & Fitness and More), End-User (Consumers and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34.57% of global revenue in 2024 owing to robust reimbursement frameworks and streamlined FDA pathways that hasten commercialization. Uptake of CMS-approved remote patient-monitoring codes encourages hospitals to distribute certified sensors at discharge, driving further penetration across primary-care networks. U.S. tech giants foster vibrant developer ecosystems that enrich device functionality with third-party applications. Canada scales similar models through provincial tele-health mandates, while Mexico leverages cross-border supply chains to make certified devices accessible at lower cost.

Europe maintains momentum with a 15.32% CAGR, anchored by GDPR-aligned privacy assurance that elevates patient trust. Germany's DiGA program reimburses digital therapeutics, including cardiac-rhythm patches, through statutory insurance. France adopts nationwide electronic prescription services that automate device ordering, and Italy pilots public-private partnerships to integrate fall-detection wearables in elderly-care homes. The Medical Device Regulation's post-market surveillance obligations heighten vendor accountability, elevating the reputation of CE-marked products across the wearable medical devices market.

Asia-Pacific is forecast to be the fastest-growing territory at 16.42% CAGR. China's broader medical-device sector is trending toward USD 210 billion by 2025 as local champions secure National Medical Products Administration clearance for glucose monitors and AI-aided arrhythmia patches. Japan's health-ministry guidance endorses smartwatch-derived ECG data for preliminary triage, while South Korea subsidizes smart-clothing factories under its Bio-Healthcare 2030 plan. India's digital-health mission promotes Bluetooth-enabled vitals devices in rural clinics, enhancing accessibility. Regional contract manufacturers supply global brands, reinforcing Asia-Pacific's influence on production scale and cost leadership within the wearable medical devices market.

- Abbott Laboratories

- AIQ Smart Clothing Inc.

- Alphabet Inc.

- Apple

- Biobeat Technologies Ltd.

- Dexcom

- Garmin

- Huawei Technologies

- imec

- Intelesens

- Koninklijke Philips

- Lifesense Group

- Masimo

- Medtronic

- MINTTI Health

- OMRON

- Resmed

- Samsung Group

- Withings SA

- Xiaomi Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of chronic diseases & home-healthcare demand

- 4.2.2 Increasing adoption of AI-enabled biosensors for disease-specific monitoring

- 4.2.3 Growing reimbursement for remote patient-monitoring programs

- 4.2.4 Integration with consumer-tech ecosystems boosting user engagement

- 4.2.5 Miniaturization of battery technology lowering form-factor constraints

- 4.2.6 Regulatory fast-track pathways for digital therapeutics & connected devices

- 4.3 Market Restraints

- 4.3.1 Cyber-security & data-privacy compliance costs

- 4.3.2 Fragmented device-data standards hindering interoperability

- 4.3.3 Low physician trust in consumer-grade data accuracy

- 4.3.4 Battery-longevity and e-waste concerns

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 Vital-sign Monitoring Devices

- 5.1.1.2 Sleep-monitoring Devices

- 5.1.1.3 Continuous-Glucose Monitors

- 5.1.1.4 Blood-pressure Monitors

- 5.1.1.5 Other Diagnostic & Monitoring Devices

- 5.1.2 Therapeutic Devices

- 5.1.2.1 Pain-management Devices

- 5.1.2.2 Rehabilitation Devices

- 5.1.2.3 Respiratory-therapy Devices

- 5.1.2.4 Insulin-delivery Devices

- 5.1.2.5 Other Therapeutic Devices

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Age Group

- 5.2.1 Under 18

- 5.2.2 18 - 60

- 5.2.3 Above 60

- 5.3 By Distribution Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By Application

- 5.4.1 Sports & Fitness

- 5.4.2 Remote Patient Monitoring

- 5.4.3 Home Healthcare

- 5.5 By End-User

- 5.5.1 Consumers

- 5.5.2 Hospitals & Clinics

- 5.5.3 Long-term Care Centres

- 5.5.4 Ambulatory Surgical Centres

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 AIQ Smart Clothing Inc.

- 6.4.3 Alphabet Inc.

- 6.4.4 Apple Inc.

- 6.4.5 Biobeat Technologies Ltd.

- 6.4.6 Dexcom Inc.

- 6.4.7 Garmin Ltd.

- 6.4.8 Huawei Technologies Co., Ltd.

- 6.4.9 imec

- 6.4.10 Intelesens Ltd.

- 6.4.11 Koninklijke Philips N.V.

- 6.4.12 Lifesense Group

- 6.4.13 Masimo Corporation

- 6.4.14 Medtronic plc

- 6.4.15 MINTTI Health

- 6.4.16 Omron Corporation

- 6.4.17 ResMed Inc.

- 6.4.18 Samsung Electronics Co., Ltd.

- 6.4.19 Withings SA

- 6.4.20 Xiaomi Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment