PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849869

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849869

Automotive Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

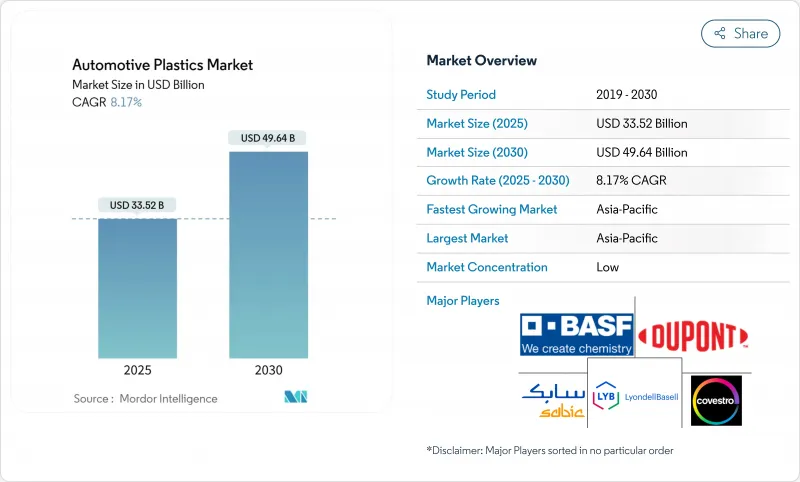

The Automotive Plastics Market size is estimated at USD 33.52 billion in 2025, and is expected to reach USD 49.64 billion by 2030, at a CAGR of 8.17% during the forecast period (2025-2030).

The steady uptick reflects automakers' pivot toward lighter materials to reconcile strict emission rules with performance targets. Accelerated adoption of advanced polymer solutions, especially in electric-vehicle (EV) platforms, is pushing the automotive plastics market well ahead of its historical pace. Asia-Pacific commands almost half of global demand and is compounding at the fastest regional rate, while polypropylene (PP) continues to set the benchmark for cost-to-performance across major vehicle systems.

Global Automotive Plastics Market Trends and Insights

Increasing demand for lightweight materials in electric vehicles

Range anxiety and battery-pack cost keep lightweighting at the center of EV engineering. PP compounds now appear in larger volumes per EV than in comparable internal-combustion cars, largely because lower mass converts directly into added driving range without resizing the battery. Beyond instrument panels and trims, high-dielectric PP and advanced polyamide grades are entering structural housings and high-voltage busbars. Dedicated EV platforms free designers from legacy metal hard-points, allowing more plastic integration into body structures and thermal-management channels.

Carbon-emission penalties accelerating polypropylene bumper adoption

Fleet-average emissions standards in Europe and North America impose significant financial penalties for excess CO2. Automakers therefore target "quick wins" such as switching from metal-reinforced to fully PP bumpers, achieving meaningful mass savings at lower system cost. Industry life-cycle assessments consistently show PP bumpers delivering a smaller carbon footprint than steel or aluminum alternatives once use-phase fuel savings are incorporated.

OEM qualification delays for Bio-PA due to odor & flammability

Bio-sourced polyamides promise lower cradle-to-gate emissions, yet residual odor and inconsistent ignition behavior complicate cabin and under-hood approvals. Academic work on cellulosic-fiber-reinforced Bio-PA confirms wide variability in mechanical properties stemming from fiber dispersion challenges. Industry groups have petitioned regulators to allow longer validation cycles so material suppliers can fine-tune formulations.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Modular Front-End Carriers (MECs) via injection-molded hybrids

- Growing demand for flexible and cost-efficient design materials

- High materials and processing cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene held a commanding 34.18% automotive plastics market share in 2024 on the back of balanced cost, processability and property retention. Interior fascia, door trims and center consoles dominate PP usage, but glass-fiber-reinforced grades now extend into semi-structural seat carriers and tailgates.

Polyamides are climbing an 8.87% CAGR trajectory through 2030 as high-temperature electrified powertrains demand better thermal and dielectric insulation. PA66 and partially aromatic PA6/6T blends displace metal brackets in battery-cold-plate assemblies, inverter housings and turbo-air ducts. Bio-based PA grades, while not yet mainstream, attract OEMs seeking Scope-3 carbon reductions once odor and flame-spread hurdles are cleared.

Interior accounted for 32.97% of the automotive plastics market size in 2024, buoyed by demand for soft-touch dashboards, ambient-lit door panels, and integrating display clusters into single multi-shot molded units. Haptic coatings and laser-etch graphics depend on specialty PP, ABS, and PC/PMMA blends, reinforcing plastics' role in experiential design.

Under-bonnet components, though smaller in absolute volume, are growing at 8.98% per year. Electrified architectures pack more electronics and require intricate cooling channels; thus, heat-stabilized PA, PPS, and PBT replace die-cast aluminum for e-motor cooling jackets and high-voltage busbar covers.

The Automotive Plastics Market Report Segments the Industry by Material (Polypropylene (PP), Polyurethane (PU), Polyvinyl Chloride (PVC), and More), Application (Exterior, Interior, and More), Vehicle Type (Conventional/Traditional Vehicles, and Electric Vehicles), Source (Virgin Plastic, Recycled Plastic, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the automotive plastics market with a 48.25% stake in 2024 and mirrors the highest regional CAGR at 9.82% to 2030. China's large-scale EV rollout, supported by battery-maker alliances and state incentives, is spurring polymer capacity expansions across PP, PA and PBT value chains. India records double-digit growth in passenger-car output, triggering investments in local compounding hubs to curb import reliance. South Korea and Japan refine ultra-high-molecular-weight grades for impact-resistant exterior panels, further embedding a virtuous innovation-capacity loop.

North America presents a mature yet inventive landscape. Compliance with tightening Corporate Average Fuel Economy standards pushes OEMs toward multi-material architectures that maximize plastics in liftgates, battery packs and advanced driver-assistance sensor housings. The United States also hosts pioneering work in closed-loop recycling partnerships between resin suppliers and tier-one molders, supporting local circular-economy targets.

Europe maintains sizeable demand anchored by premium vehicle segments and aggressive regulatory frameworks. The proposed 25% recycled-content threshold in passenger cars catalyzes R&D around compatibilizer additives and de-odorizing systems that elevate post-consumer resin performance. Germany leads technology deployments in fiber-reinforced PA cross-members, while France and the United Kingdom channel public funding toward biopolymer pilot lines. The region nevertheless faces margin pressures from energy-cost volatility, making material efficiency a strategic imperative.

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lighweight Materials in Electric Vehicles

- 4.2.2 Carbon Emission Penalties Accelerating Polypropylene Bumper Adoption

- 4.2.3 Shift to Modular Front-End Carriers (MECs) via Injection-Molded Hybrids

- 4.2.4 Growing Demand for Flexible and Cost Efficient Design Materials in Automotive

- 4.2.5 Consistent Expansion of the Global Automotive Sector

- 4.3 Market Restraints

- 4.3.1 OEM Qualification Delays for Bio-PA due to Odor and Flammability

- 4.3.2 High Materials and Processing Cost

- 4.3.3 Incraesing Competion from Alternative Materials in Automotive

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyurethane (PU)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Polyethylene (PE)

- 5.1.5 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.6 Polyamides (PA)

- 5.1.7 Polycarbonate (PC)

- 5.1.8 Other Materials

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.2 Interior

- 5.2.3 Under Bonnet

- 5.2.4 Other Applications

- 5.3 Vehicle Type

- 5.3.1 Conventional/Traditional Vehicles

- 5.3.2 Electic Vehicles

- 5.4 Source

- 5.4.1 Virgin Plastic

- 5.4.2 Recycled Plastic

- 5.4.3 Bio-based Plastic

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Advance Corporation

- 6.4.3 BASF SE

- 6.4.4 Borealis AG

- 6.4.5 Braskem

- 6.4.6 Celanese Corporation

- 6.4.7 Covestro AG

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 dsm-firmenich

- 6.4.11 DuPont

- 6.4.12 Evonik Industries AG

- 6.4.13 Exxon Mobil Corporation

- 6.4.14 INEOS

- 6.4.15 LANXESS

- 6.4.16 LG Chem

- 6.4.17 LyondellBasell Industries Holdings B.V.

- 6.4.18 Mitsui Chemicals Inc.

- 6.4.19 SABIC

- 6.4.20 TEIJIN LIMITED

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Technological Developments in Electric Vehicles