PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849880

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849880

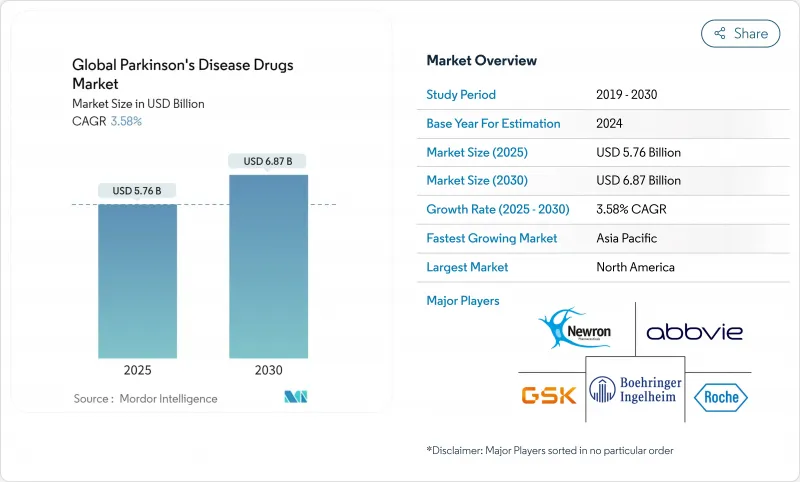

Global Parkinson's Disease Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Parkinson disease market is valued at USD 5.76 billion in 2025 and is projected to reach USD 6.87 billion by 2030, registering a 3.58% CAGR.

Growth reflects an expanding patient pool and steady uptake of both symptomatic and disease-modifying options. Carbidopa-levodopa combinations retain commercial primacy, yet adenosine A2A antagonists advance fastest as clinicians seek complementary non-dopaminergic relief. Continuous infusion devices win clinical favor for reducing motor fluctuations, while digital pharmacies widen access to therapy. North America preserves revenue leadership, whereas Asia Pacific posts the quickest expansion as aging trends accelerate and reimbursement frameworks broaden.

Global Parkinson's Disease Drugs Market Trends and Insights

Rising Geriatric Population & Rising Disease Burden

The global Parkinson patient base is projected to reach 25.2 million by 2050, more than doubling its 2021 level as longevity increases worldwide. East Asia shoulders the largest absolute case growth, while western Sub-Saharan Africa records the steepest percentage rise, steering investment toward region-tailored care models . Annual U.S. economic burden already tops USD 52 billion, prompting payer emphasis on early intervention to curb long-term disability costs.

Growing Awareness & Early Diagnosis Initiatives

AI-enabled blood assays can predict disease onset seven years before overt symptoms, allowing enrollment into neuroprotective trials earlier than ever. Complementary smartwatch analytics on 100,000 participants validated motion-pattern biomarkers that flag prodromal cases. Thailand's nationwide digital screening illustrates how low-cost tools enlarge detection in middle-income settings. Earlier diagnosis increases the addressable base for pipeline disease-modifying products.

Adverse Events Associated With Current Therapeutics

Chronic levodopa exposure produces motor complications; benserazide regimens show odds ratios of 170.74 for on-off phenomena, markedly higher than carbidopa's 67.5. Dopamine agonists carry impulse-control risks, and deep-brain stimulation involves surgical morbidity, limiting uptake outside high-resource centers.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Reimbursement & Insurance Coverage

- Increasing R&D Investment & Continuous Drug Approvals

- Adoption of Long-Acting Continuous Infusion Formulations

- AI-Driven Drug-Repurposing Pipelines Targeting a-Synuclein

- High Treatment & R&D Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Carbidopa-levodopa segment led the Parkinson disease market with a 35.43% share in 2024, supported by decades of clinical familiarity. Adenosine A2A antagonists, though niche, are the quickest-growing class at 4.25% CAGR. Selective D1/D5 partial agonist tavapadon achieved significant MDS-UPDRS gains in Phase 3, reinforcing appetite for mechanisms that preserve dopaminergic signaling while reducing dyskinesia risk.

Pipeline diversification tempers reliance on dopamine modulation. AI-derived a-synuclein inhibitors and GDNF gene-therapy vectors illustrate a pivot toward disease modification. As these reach commercial stages, the Parkinson disease market size for non-dopaminergic categories is expected to widen, enhancing therapeutic choice and competitive differentiation.

The Report Covers Parkinson's Disease Therapeutics Market and It is Segmented by Mechanism of Action (Dopamine Agonists, Anticholinergic, MAO-B Inhibitors, Carbidopa-Levodopa, and More), Route of Administration (Oral, Transmucosal, and More), by Distribution Channel (Hospital Pharmacies, Online Pharmacies, and More), and Geography. The Market Provides the Value (in USD Million) for the Above Segments.

Geography Analysis

North America contributed 44.35% of global value in 2024, leveraging well-funded health systems, comprehensive insurance, and dense movement-disorder specialist networks. Federal initiatives such as the National Plan to End Parkinson's Act earmark additional research financing, sustaining innovation momentum. Yet rural communities still face longer diagnostic delays due to limited neurologist access.

Asia Pacific ranks as the fastest-growing region at 5.28% CAGR to 2030. China's case load has soared since 1990, and clinician awareness of non-motor symptoms is improving, although rural treatment gaps persist. Japan's super-aged demographics spur demand for advanced devices, while India's expanding middle class boosts volume, albeit constrained by uneven specialist distribution. Regulatory harmonization across ASEAN members trims approval timelines, favoring multinational launches.

Europe enjoys consistent uptake backed by universal insurance, but individual-state reimbursement decisions create variability. Brexit-related customs changes caused occasional levodopa shortages in the United Kingdom, prompting calls for resilient supply strategies. Germany's 2025 guideline update emphasizes early interdisciplinary management, reinforcing stable demand across drug classes. Latin America and Middle East & Africa display emerging opportunities parallel to rising life expectancy and improving neurologic care infrastructure.

- Abbvie

- Amneal Pharmaceuticals

- Viatris

- Boehringer Ingelheim Intl. GmbH

- GlaxoSmithKline

- Teva Pharmaceutical Industries

- Pfizer

- Novartis

- Roche

- ABL bio

- KISSEI PHARMACEUTICAL

- AstraZeneca

- Prevail Therapeutics

- Newron Pharmaceuticals S.p.A.

- Kyowa Kirin

- ACADIA Pharmaceuticals Inc.

- UCB

- Sunovion Pharmaceuticals

- Neurocrine Biosciences

- Lundbeck A/S

- Voyager Therapeutics, Inc.

- Supernus Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Population & Rising Disease Burden

- 4.2.2 Growing Awareness & Early Diagnosis Initiatives

- 4.2.3 Expanding Reimbursement & Insurance Coverage

- 4.2.4 Increasing R&D Investment & Continuous Drug Approvals

- 4.2.5 Adoption Of Long-Acting Continuous Infusion Formulations

- 4.2.6 Ai-Driven Drug-Repurposing Pipelines Targeting A-Synuclein

- 4.3 Market Restraints

- 4.3.1 Adverse Events Associated With Current Therapeutics

- 4.3.2 High Treatment & R&D Costs

- 4.3.3 Supply-Chain Constraints For Levodopa Apis

- 4.3.4 Regulatory Uncertainty Around Disease-Modifying Claims

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Mechanism of Action

- 5.1.1 Dopamine Agonists

- 5.1.2 Anticholinergics

- 5.1.3 MAO-B Inhibitors

- 5.1.4 Amantadine

- 5.1.5 Carbidopa-levodopa

- 5.1.6 Adenosine A2A Antagonists

- 5.1.7 Other Mechanisms of Action

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Transdermal

- 5.2.3 Subcutaneous

- 5.2.4 Infusion

- 5.2.5 Intranasal

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amneal Pharmaceuticals LLC

- 6.3.3 Viatris

- 6.3.4 Boehringer Ingelheim Intl. GmbH

- 6.3.5 GSK plc

- 6.3.6 Teva Pharmaceutical Industries Ltd

- 6.3.7 Pfizer Inc.

- 6.3.8 Novartis AG

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 ABL bio

- 6.3.11 Kissei Pharmaceutical Co., Ltd.

- 6.3.12 AstraZeneca

- 6.3.13 Prevail Therapeutics

- 6.3.14 Newron Pharmaceuticals S.p.A.

- 6.3.15 Kyowa Kirin Co., Ltd.

- 6.3.16 ACADIA Pharmaceuticals Inc.

- 6.3.17 UCB S.A.

- 6.3.18 Sunovion Pharmaceuticals Inc.

- 6.3.19 Neurocrine Biosciences, Inc.

- 6.3.20 Lundbeck A/S

- 6.3.21 Voyager Therapeutics, Inc.

- 6.3.22 Supernus Pharmaceuticals, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment