PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849900

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849900

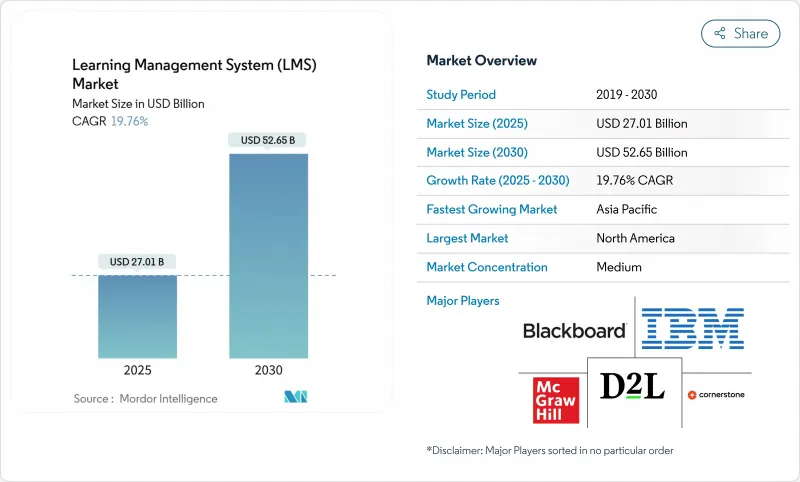

Learning Management System (LMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The learning management system market is valued at USD 27.01 billion in 2025 and is forecast to climb to USD 52.65 billion by 2030, advancing at a 19.76% CAGR.

Enterprises across sectors are investing in AI-powered personalization, micro-credentialing, and mobile learning to keep workforce skills current while meeting increasingly complex compliance mandates. North American healthcare and financial-services organizations remain early adopters, yet Asia-Pacific manufacturing hubs now drive incremental demand by linking digital learning to measurable productivity gains. Technology vendors are responding with predictive analytics, granular skills verification, and low-code integration to embed training into daily workflows. At the same time, rising SaaS licensing fees and last-mile connectivity gaps restrain budget-sensitive segments, forcing vendors to refine pricing tiers and content-delivery optimization.

Global Learning Management System (LMS) Market Trends and Insights

AI-Driven Adaptive Learning Algorithms Transform Course Completion Dynamics

AI-powered adaptive systems now tailor difficulty, pacing, and feedback in real time, delivering 40% higher course-completion rates for pilot programs in North American universities. Algorithms analyse time-on-task, assessment scores, and click-stream data to forecast disengagement and trigger targeted interventions that keep learners on track. Enterprises mirror this practice to reduce onboarding time and raise certification pass rates, tying learning objectives directly to key-performance indicators. Vendors that embed explainable AI build credibility with educators who must defend algorithmic decisions during accreditation audits. As feature sets mature, customers expect plug-and-play recommendation engines rather than bespoke data-science projects, simplifying adoption for mid-market buyers.

Micro-Credentials Drive Skills-Based Hiring Revolution

Asia-Pacific manufacturers face rapid automation cycles and therefore favour bite-sized certifications that prove competence in robotics, quality control, and supply-chain analytics. Surveys show 86% of employers rate micro-credentials as beneficial when evaluating applicants; workers progressively stack these badges to create dynamic skill portfolios. Blockchain verification ensures tamper-proof records that hiring managers can authenticate instantly, shortening recruitment cycles. As evidence of impact spreads, professional associations in North America begin mapping badges to continuing-education credits, extending the credentialing model into regulated professions.

SaaS Licensing Cost Inflation Pressures Educational Budgets

Recurring per-learner fees escalate as pandemic relief subsidies taper, forcing K-12 districts to reassess multi-year LMS contracts. Districts with 20,000 students report annual renewals rising 14% in 2025, outpacing stagnant operating budgets. Some pivot to open-source alternatives yet discover hidden costs in self-hosting and maintenance, highlighting a trade-off between cash outlay and administrative burden. Vendors respond with tiered pricing tied to active user metrics, but transparency remains inconsistent, prolonging procurement cycles.

Other drivers and restraints analyzed in the detailed report include:

- European Healthcare CPD Regulations Mandate Specialized Training Modules

- BYOD Workforce Mobility Accelerates Mobile-First LMS Architecture

- Infrastructure Limitations Constrain Immersive Learning Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated a dominant 67% revenue share in 2024, underscoring the centrality of platform licences in the learning management system market. The Services segment, however, is racing ahead at a 21.3% CAGR. Organisations that have already deployed a core platform now seek instructional-design support, system integration, and analytics optimisation. Case studies show that supply-chain firms achieved 30% faster course development after outsourcing content mapping to specialist agencies. As AI features proliferate, in-house teams require guidance to calibrate algorithms, opening new revenue pools for professional-services providers. The learning management system market size for Services is projected to rise from USD 8.11 billion in 2025 to USD 21.2 billion by 2030.

The Solutions segment is hardly static. Vendors are layering low-code workflow builders, API marketplaces, and native video-production suites to stave off commoditisation. Larger buyers negotiate enterprise-wide contracts that bundle multiple modules-authoring, credentialing, and advanced analytics-into predictable subscription envelopes. Smaller vendors differentiate through vertical templates that ship with compliance libraries for health and manufacturing domains. Consequently, procurement teams now evaluate total cost of ownership over five-year horizons rather than headline licence fees, a shift that benefits suppliers able to present robust ecosystem roadmaps.

Cloud architectures held 70% share of total learning management system market revenue in 2024 and continue to expand at 22.8% CAGR. Buyers cite automatic security patches, elastic scaling, and reduced IT overhead as decisive factors. Multinational firms further value region-specific data-residency options that simplify privacy compliance in Europe and Asia. The learning management system market size for cloud deployments is poised to climb from USD 18.9 billion in 2025 to USD 43.4 billion by 2030, underscoring an accelerating on-premise migration wave.

On-premise implementations persist in defence, energy, and public-sector accounts where air-gapped environments mitigate espionage risks. Even these organisations increasingly test private-cloud pilots to modernise user experience and analytics. Vendors thus support hybrid architectures that synchronise content repositories while retaining sensitive assessment data on local servers. Marketplace momentum nevertheless favours pure-cloud disruptors that release new features monthly, outpacing annual upgrade cycles typical of legacy suites.

The Learning Management System Market is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Delivery Mode (Distance Learning, Instructor-Led Training), End-User Vertical (BFSI, Healthcare and Pharmaceuticals, Manufacturing, Retail and Consumer Goods, Educational Institutions, Government Agencies, Other End-User Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 36% of global revenue in 2024, supported by advanced connectivity, high SaaS readiness, and stringent compliance frameworks across healthcare and finance. Large enterprises now focus on AI-driven optimisation rather than first-time deployment, spurring demand for predictive talent analytics add-ons. Federal and state grants targeting workforce reskilling further buoy platform adoption in community colleges and veteran-training programmes. Nevertheless, budget scrutiny in K-12 districts tempers short-term growth until funding models stabilise.

Asia-Pacific is projected to grow at 24.5% CAGR through 2030, propelled by India's Digital India programme and China's Made in China 2025 policy, both of which tie industrial modernisation to workforce upskilling. Multinational manufacturers mandate uniform training standards across regional plants, creating cross-border LMS rollouts that reward vendors with localisation expertise. Banking digitalisation across ASEAN markets further drives compliance-training licences. Still, linguistic diversity and varied data-privacy statutes necessitate modular deployment strategies.

Europe exhibits stable expansion as GDPR compliance and CPD rules fuel demand for platforms with granular audit trails. Governments fund digital apprenticeships that rely on LMS scaffolding, while corporations integrate learning suites with talent-management systems to address demographic skill shortages. The Middle East experiences above-average growth in GCC economies where national-transformation agendas prioritise digital skills. Africa shows uneven progress; urban centres adopt cloud LMS rapidly whereas rural districts lag due to connectivity challenges.

- McGraw-Hill Companies

- Blackboard Inc.

- D2L Corporation

- Cornerstone OnDemand Inc.

- IBM Corporation

- Oracle Corporation

- Instructure Inc.

- SAP SE

- Docebo SpA

- Saba Software

- Moodle Pty Ltd

- Adobe Inc.

- Absorb Software Inc.

- TalentLMS (Epignosis LLC)

- Infor (Infor LMS)

- Skillsoft Corporation

- Edmodo

- Schoology (PowerSchool)

- Tovuti LMS

- PowerSchool Holdings Inc.

- 360Learning SA

- Thought Industries Inc.

- Meridian Knowledge Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of AI-driven adaptive learning algorithms boosting course-completion rates in North American higher-education

- 4.2.2 Employer demand for skills-verification micro-credentials fueling LMS uptake across APAC manufacturing hubs

- 4.2.3 Mandatory CPD regulations in EU healthcare catalyzing specialised LMS modules

- 4.2.4 BYOD workforce mobility in distributed retail chains accelerating mobile-first cloud LMS adoption in Middle East

- 4.3 Market Restraints

- 4.3.1 Rising per-learner SaaS-licensing inflation squeezing budgets of K-12 districts

- 4.3.2 Patchy 5G / broadband coverage limiting immersive-content delivery in rural Africa and South Asia

- 4.3.3 Fragmented data standards hindering HRIS-LMS integrations in legacy-heavy European corporates

- 4.3.4 Escalating cyber-insurance premiums post-ransomware attacks deterring small healthcare providers from cloud LMS migration

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers / Learners

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Delivery Mode

- 5.3.1 Distance Learning

- 5.3.2 Instructor-led Training

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Pharmaceuticals

- 5.4.3 Manufacturing

- 5.4.4 Retail and Consumer Goods

- 5.4.5 Educational Institutions

- 5.4.6 Government Agencies

- 5.4.7 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 GCC

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 McGraw-Hill Companies

- 6.4.2 Blackboard Inc.

- 6.4.3 D2L Corporation

- 6.4.4 Cornerstone OnDemand Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Oracle Corporation

- 6.4.7 Instructure Inc.

- 6.4.8 SAP SE

- 6.4.9 Docebo SpA

- 6.4.10 Saba Software

- 6.4.11 Moodle Pty Ltd

- 6.4.12 Adobe Inc.

- 6.4.13 Absorb Software Inc.

- 6.4.14 TalentLMS (Epignosis LLC)

- 6.4.15 Infor (Infor LMS)

- 6.4.16 Skillsoft Corporation

- 6.4.17 Edmodo

- 6.4.18 Schoology (PowerSchool)

- 6.4.19 Tovuti LMS

- 6.4.20 PowerSchool Holdings Inc.

- 6.4.21 360Learning SA

- 6.4.22 Thought Industries Inc.

- 6.4.23 Meridian Knowledge Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment