PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849922

Global Neurology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

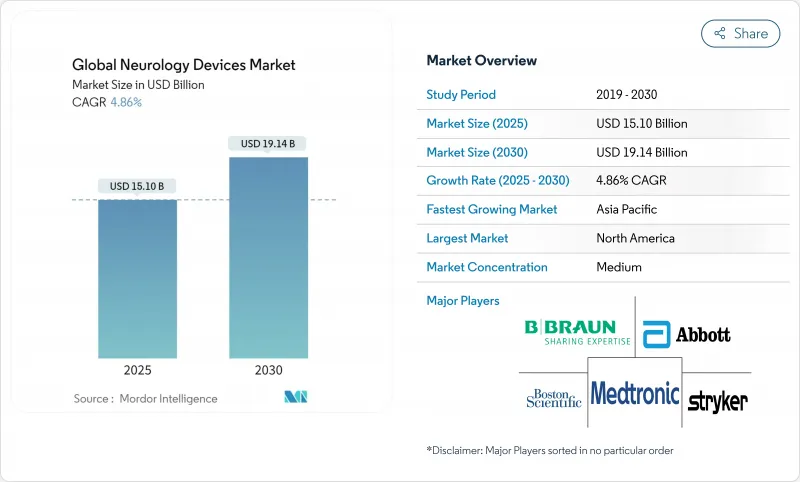

The Neurology Devices market generated USD 15.10 billion in 2025 and is on course to reach USD 19.14 billion by 2030, advancing at a 4.86% CAGR.

Growth reflects a shift from episodic, hospital-centric interventions to data-rich, predictive care models powered by artificial intelligence and closed-loop neuro-stimulation systems. Demand widens as stroke, Parkinson's disease, epilepsy and chronic pain remain high-priority public-health issues, and as aging populations intensify the neurological disease burden. Capital inflows, accelerated FDA clearances for adaptive stimulators and breakthroughs in mechanical thrombectomy catheters add momentum, while reimbursement code updates for closed-loop devices reduce payer friction in key markets. Conversely, supply-chain risks around rare-earth magnets and bismuth alloys, together with surgeon shortages in low- and middle-income countries, temper the Neurology Devices market's full potential.

Global Neurology Devices Market Trends and Insights

Rising Prevalence of Neuro-vascular & Neuro-degenerative Disorders

Neurological conditions now affect 43% of the global population, expanding the addressable pool for therapeutic devices. . Stroke remains paramount: large-vessel occlusions represent up to 40% of ischemic cases and demand rapid thrombectomy solutions. Post-viral neurological sequelae following COVID-19 and other pathogens further elevate device utilization. Given these epidemiologic realities, the Neurology Devices market continues to prioritise high-efficacy interventions and scalable chronic-disease monitoring strategies.

Technological Advances in Minimally Invasive & Image-Guided Devices

Fourth-generation aspiration catheters, steerable micro-catheters and 300 mT/m gradient MRI scanners shorten procedure time and elevate diagnostic precision. Real-time algorithms embedded in thrombectomy devices improve first-pass success and reduce downstream costs. Interplay of robotics, augmented reality and AI prompts faster learning curves for neurosurgeons, helping address workforce deficits. By raising clinical thresholds, technology upgrades consolidate share for R&D-intensive firms and reinforce entry barriers, affecting long-tail suppliers in the Neurology Devices industry.

High Device & Procedure Cost Burden

Spinal cord stimulation implants cost USD 35,000-70,000, while revisions add USD 15,000-25,000, limiting penetration among under-insured cohorts Journal of Pain Research. Explant rates hover near 10% owing mainly to efficacy loss, raising total-cost-of-ownership anxieties. In India, detachable coils for aneurysm repair attract import duties of 10%, compounding affordability hurdles MD+DI. Such cost vectors slow adoption despite clinical need.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Healthcare Spend & Neuro-rehab Reimbursement Schemes

- Wearable EEG & At-Home Neuro-monitoring Creating New Outpatient Revenue

- Lengthy & Complex Regulatory Approval Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Interventional systems captured 38.78% Neurology Devices market share in 2024 as mechanical thrombectomy and flow-diverter implants became standard of care for acute ischemic stroke. Data from the EXCELLENT registry showed final reperfusion rates of 94.5% with the EMBOTRAP retriever, reinforcing physician confidence. Neurodiagnostic monitors, cerebrospinal-fluid shunts and neuro-stimulation implants collectively anchor hospital procurement budgets, while platform upgrades, such as steerable micro-catheters, keep capital-replacement cycles brisk.

Rehabilitation & wearable devices, posting a 5.34% CAGR, increasingly enable post-operative and chronic-disease monitoring at home. In-ear EEG wearables capture seizure precursors, reducing emergency admissions and widening recurring-service revenue. Competitive barriers here hinge on data-analytics IP rather than hardware, inviting tech entrants. Consequently, incumbent catheter and shunt suppliers diversify portfolios to hedge against slower growth in mature theatre-based products.

The Neurology Devices Market Report Segments the Industry Into by Type of Device (Neurostimulation Devices, Interventional Neurology Devices and More), by Application (Stroke Management, Chronic Pain & Movement Disorders and More), by End User (Hospitals, Ambulatory Surgery Centers and More) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led revenue with 40.67% share in 2024 on the back of robust payer coverage, highly skilled neurologists and R&D ecosystems. Canada's single-payer model funds nationwide closed-loop SCS trials, while Mexico accelerates MRI procurement via public-private partnerships.

Asia-Pacific posts the quickest 7.13% CAGR, propelled by China's BCI roadmap and Japan's remote-care pilots. Government grants subsidise domestic flow-diverter manufacturing, reducing import reliance and bolstering local champions. India logs double-digit growth in detachable-coil sales as its ageing cohort expands, although affordability gaps persist.

Europe remains a steady contributor, emphasising clinical-value demonstration under Medical Device Regulation. Germany's rising hydrocephalus incidence fuels shunt demand, whereas the United Kingdom pilots AI-triaged stroke pathways that may scale continent-wide. Meanwhile, Switzerland's potential recognition of FDA approvals streamlines dual-market launches, benefiting US-centric manufacturers.

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Stryker

- Johnson & Johnson (CERENOVUS)

- LivaNova

- Penumbra

- MicroPort

- Terumo

- Integra LifeSciences

- Zimmer Biomet

- Nevro

- Cochlear

- Natus Medical

- B. Braun

- Koninklijke Philips

- GE Healthcare

- Siemens Healthineers

- Neuronetics

- Inari Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of neuro-vascular & neuro-degenerative disorders

- 4.2.2 Technological advances in minimally-invasive & image-guided devices

- 4.2.3 Expanding healthcare spend & neuro-rehab reimbursement schemes

- 4.2.4 AI-enabled closed-loop neuro-stimulation platforms

- 4.2.5 Wearable EEG & at-home neuro-monitoring creating new outpatient revenue

- 4.2.6 Remote-care pilots in China & Japan for neuromodulation therapy

- 4.3 Market Restraints

- 4.3.1 High device & procedure cost burden

- 4.3.2 Lengthy & complex regulatory approval cycles

- 4.3.3 Shortage of interventional neuro-surgeons in emerging regions

- 4.3.4 Supply-chain risk for implantable-grade rare-earth materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Device Type

- 5.1.1 Neurostimulation Devices

- 5.1.2 Interventional Neurology Devices

- 5.1.3 Neurosurgery Devices

- 5.1.4 Cerebrospinal Fluid Management Devices

- 5.1.5 Neurodiagnostic & Monitoring Devices

- 5.1.6 Neuro-rehabilitation & Wearables

- 5.2 By Application

- 5.2.1 Stroke Management

- 5.2.2 Chronic Pain & Movement Disorders

- 5.2.3 Epilepsy

- 5.2.4 Neuro-degenerative Diseases

- 5.2.5 Traumatic Brain & Spinal Injuries

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Neurology Clinics

- 5.3.4 Home-care Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corp.

- 6.3.4 Stryker Corporation

- 6.3.5 Johnson & Johnson (CERENOVUS)

- 6.3.6 LivaNova PLC

- 6.3.7 Penumbra Inc.

- 6.3.8 MicroPort Scientific

- 6.3.9 Terumo Corporation

- 6.3.10 Integra LifeSciences

- 6.3.11 Zimmer Biomet

- 6.3.12 Nevro Corporation

- 6.3.13 Cochlear Ltd.

- 6.3.14 Natus Medical

- 6.3.15 B. Braun Melsungen AG

- 6.3.16 Philips Healthcare

- 6.3.17 GE Healthcare

- 6.3.18 Siemens Healthineers

- 6.3.19 Neuronetics Inc.

- 6.3.20 Inari Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment