PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849931

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849931

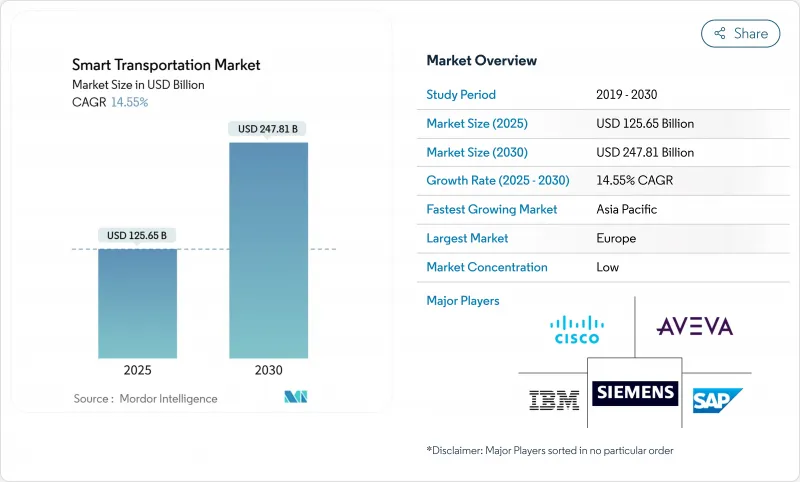

Smart Transportation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The smart transportation market size is valued at USD 125.65 billion in 2025 and is forecast to reach USD 247.81 billion by 2030, registering a 14.55% CAGR.

Strong policy backing and rising urban populations are steering governments toward data-centric traffic systems that deliver more capacity without paving additional lanes. Cloud-native analytics, 5G-enabled vehicle connectivity, and digital twin modeling are converging to cut congestion, shorten travel times, and improve safety. Public capital is flowing into deployment: in October 2024, the United States approved USD 4.2 billion for 44 next-generation mobility projects.Europe leads adoption through its Sustainable and Smart Mobility Strategy that promotes zero-emission travel under 500 km and mandates open data across modes of transport. Asia-Pacific is scaling fastest as megacities roll out intelligent highways and MaaS platforms to manage the largest wave of urbanisation in history.

Global Smart Transportation Market Trends and Insights

Rapid Urban-Population Growth Stressing Legacy Road Networks

The migration of people toward cities is creating unprecedented traffic density, with urban areas forecast to host 60% of the global population by 2030. Congestion already erodes 2-4% of GDP in many economies, spurring transport agencies to deploy AI-driven traffic optimisation instead of costly road widening. Beijing's smart signal network cut average delays by 23% in 2024, and similar deployments are underway in Mumbai and Jakarta. Digital twins allow planners to stress-test lane configurations virtually, while adaptive signal control paired with vehicle probe data has trimmed corridor travel times by 25% inside Asian megacities. The smart transportation market, therefore, benefits directly from urban density as cities prioritise technological fixes over concrete expansions.

Government Smart-City Funding & ITS Mandates

Legislative support is translating into multibillion-dollar pipelines for intelligent mobility. The U.S. Infrastructure Investment and Jobs Act allocates USD 91.2 billion for modernising public transit, and the ATTAIN program reserves USD 60 million annually for advanced technology pilots. Parallel initiatives in the European Union mandate interoperable data sharing and carbon-neutral corridors, anchoring demand certainty for vendors in the smart transportation market. Funding provisions often require rural inclusion, widening addressable demand beyond tier-one cities, and stimulating innovation in low-cost sensor packages and cloud orchestration.

High Upfront Capex for City-Wide ATMS Roll-Outs

Deploying an advanced traffic management backbone can cost USD 6,000-7,000 per intersection, and large cities easily exceed USD 70 million capital outlay. Budget cycles and procurement rules slow adoption, particularly where tax bases are small. Public-private partnerships and usage-based pricing models are emerging to defer capex, yet financial friction remains the most immediate headwind facing the smart transportation market.

Other drivers and restraints analyzed in the detailed report include:

- Drop-in Cost of AI-Enabled Edge Sensors

- Growth of MaaS Subscription Platforms

- Lack of Cross-Vendor Data Standards for V2X

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traffic Management contributed 32.30% market share to the smart transportation market in 2024 and is projected to outpace overall growth as cities target double-digit congestion cuts with AI coordination. Real-time adaptive signal control shows 35% travel-time savings in pilot corridors across Florida, underpinning procurement for intersection analytics, incident detection, and corridor optimisation. Municipal buyers value modular cloud dashboards that plug into legacy controllers without forklift upgrades, a design principle widening vendor addressability.

Parking Management technologies are advancing at a 13.2% CAGR, converting curbside inventory into digital assets and slashing cruising traffic that can reach 30% of downtown volumes. Public Transport is growing as passengers shift from ownership toward usage-based subscriptions. In freight, cooperative adaptive cruise control demonstrates 5-6% fuel savings and higher average speeds, generating business cases for logistics ITS deployments and further boosting the smart transportation market.

Advanced Transportation Management Systems represented 32% of smart transportation market share in 2024, acting as the digital operating system for multi-modal networks. Agencies are replacing siloed, on-premise servers with cloud-native orchestration that supports predictive analytics, work-zone automation, and greenhouse-gas dashboards. California's procurement to unify 20 legacy systems under a single COTS platform exemplifies the consolidation trend.

Cooperative Vehicle Systems, posting a 17.2% CAGR, marries 5G and edge AI to enable platooning, advanced hazard alerts, and prioritised emergency routing. The 5G Automotive Association's 2025 non-terrestrial network trial in Paris validated hybrid satellite-cellular V2X, widening coverage for rural highways 5gaa.org. Advanced Transportation Pricing Systems are gaining momentum as congestion pricing reshapes revenue streams and nudges modal shift, often using blockchain for real-time micro-tolling.

The Smart Transportation Market is Segmented by Application (Traffic Management, Road Safety and Security, and More), Product Type (Advanced Traveler Information Systems (ATIS), and More), Service (Deployment and Integration, and More), Transportation Mode (Roadways, Railways, and More), Connectivity Technology (DSRC/C-V2X, 5G and LTE-M, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe captured 39.5% of 2024 revenue in the smart transportation market, underpinned by stringent emissions targets and cohesive funding models. The Sustainable and Smart Mobility Strategy calls for 30 million zero-emission vehicles and a doubling of high-speed rail traffic by 2030. Investment in public data spaces and open-source simulation platforms accelerates vendor innovation while helping cities benchmark performance region-wide. Northern Europe's mature telecom infrastructure and early adoption of congestion pricing provide templates replicable across the continent.

North America ranks second. Federal programmes, including SMART Grants (USD 100 million annually) and mega-grant corridors, finance pilot scaling and rural outreach. Silicon Valley's cloud and semiconductor clusters feed a rich supplier ecosystem, allowing rapid commercialization of LIDAR modules, mapping APIs, and middleware critical to the smart transportation market. The FCC's approval for supplemental satellite coverage using commercial mobile spectrum extends V2X reach into sparsely populated regions, reinforcing the resilience of emergency services.

Asia-Pacific posts the highest growth at 13.6% CAGR. Chinese provinces are activating roadside C-V2X to meet national mandates, while India's dedicated highway and port programmes integrate IoT sensors for journey-time guarantees. ASEAN megacities deploy contactless ticketing tied to national identity schemes, shortening adoption cycles for Mobility-as-a-Service. In parallel, Middle Eastern states channel Vision 2030 funds into autonomous metro lines, targeting USD 7 billion regional ITS spend by 2030. Collectively, these initiatives cement APAC as a principal volume engine for the smart transportation market.

- Siemens Corporation

- Cisco Systems Inc.

- IBM Corporation

- SAP SE

- AVEVA Group PLC

- Thales Group

- Huawei Technologies Co. Ltd.

- Alstom SA

- Kapsch TrafficCom AG

- Hitachi Ltd.

- Oracle Corporation

- Advantech Co. Ltd.

- Orange SA

- TransCore LP

- Cubic Transportation Systems

- TomTom NV

- Panasonic Holdings Corp.

- Ericsson AB

- Qualcomm Inc.

- Continental AG

- Iteris Inc.

- PTV Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urban?population growth stressing legacy road networks

- 4.2.2 Government smart-city funding and ITS mandates

- 4.2.3 Drop-in cost of AI-enabled edge sensors

- 4.2.4 Growth of MaaS subscription platforms

- 4.2.5 Transition of toll roads to blockchain-based micro-payment rails

- 4.2.6 Aviation-grade GNSS redundancy adopted for dense urban canyons

- 4.3 Market Restraints

- 4.3.1 High upfront capex for city-wide ATMS roll-outs

- 4.3.2 Lack of cross-vendor data standards for V2X

- 4.3.3 Cyber-security-compliance liabilities for public agencies

- 4.3.4 Scarcity of dedicated 5.9 GHz spectrum in megacities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

- 4.8 Impact of Macroeconomic Trends

- 4.9 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Traffic Management

- 5.1.2 Road Safety and Security

- 5.1.3 Parking Management

- 5.1.4 Public Transport ITS

- 5.1.5 Automotive Telematics

- 5.1.6 Freight and Logistics ITS

- 5.2 By Product Type

- 5.2.1 Advanced Traveler Information Systems (ATIS)

- 5.2.2 Advanced Transportation Management Systems (ATMS)

- 5.2.3 Advanced Transportation Pricing Systems (ATPS)

- 5.2.4 Advanced Public Transportation Systems (APTS)

- 5.2.5 Cooperative Vehicle Systems (C-ITS)

- 5.3 By Service

- 5.3.1 Deployment and Integration

- 5.3.2 Cloud and Managed Services

- 5.3.3 Professional and Consulting

- 5.4 By Transportation Mode

- 5.4.1 Roadways

- 5.4.2 Railways

- 5.4.3 Airways

- 5.4.4 Maritime

- 5.5 By Connectivity Technology

- 5.5.1 DSRC / C-V2X

- 5.5.2 5G and LTE-M

- 5.5.3 Satellite (GNSS, L-band)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Initiatives and Mergers and Acquisitions

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global overview, market overview, core segments, financials, strategy, market rank/share, products and services, recent developments)

- 6.4.1 Siemens Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 IBM Corporation

- 6.4.4 SAP SE

- 6.4.5 AVEVA Group PLC

- 6.4.6 Thales Group

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 Alstom SA

- 6.4.9 Kapsch TrafficCom AG

- 6.4.10 Hitachi Ltd.

- 6.4.11 Oracle Corporation

- 6.4.12 Advantech Co. Ltd.

- 6.4.13 Orange SA

- 6.4.14 TransCore LP

- 6.4.15 Cubic Transportation Systems

- 6.4.16 TomTom NV

- 6.4.17 Panasonic Holdings Corp.

- 6.4.18 Ericsson AB

- 6.4.19 Qualcomm Inc.

- 6.4.20 Continental AG

- 6.4.21 Iteris Inc.

- 6.4.22 PTV Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment