PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066406

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066406

Blood Glucose Test Strips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

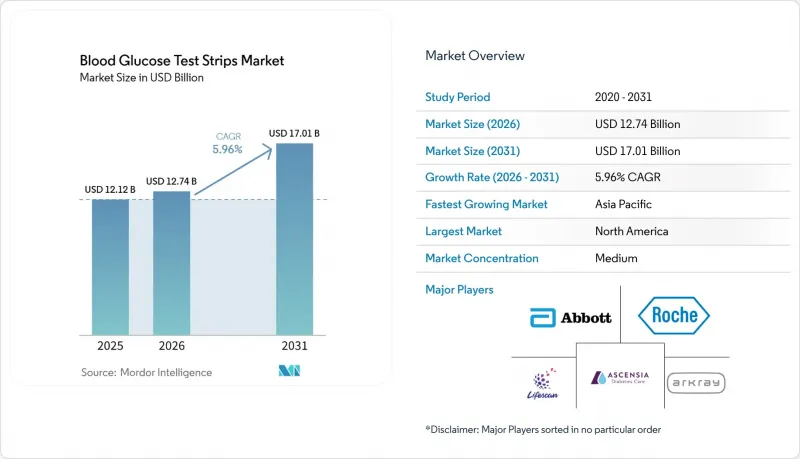

According to Mordor Intelligence, the blood glucose test strips market size was valued at USD 12.12 billion in 2025 and is estimated to grow from USD 12.74 billion in 2026 to reach USD 17.01 billion by 2031, at a CAGR of 5.96% during the forecast period (2026-2031).

This report is Segmented by Product Type (Thick Film, Thin Film, and Optical/Photometric), Diabetes Type (Type 1, Type 2, and Gestational and Others), End User (Hospitals and Clinics, and More), Distribution Channel (Hospital, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Blood Glucose Test Strips Market Trends and Insights

Escalating Global Diabetes Prevalence

Global diabetes cases reached 588.7 million adults in 2024, and 251.7 million remain undiagnosed, underscoring a vast latent user base for test strips. China recorded 140.9 million patients in 2021 and is adding roughly 10 million seniors annually, a demographic that tests glucose frequently as comorbidities mount. India distributed 1.2 million glucometers through public primary care centers in 2024, each requiring 100-200 strips per year, resulting in 120-240 million incremental units. The International Diabetes Federation foresees 852.5 million diabetics by 2050, with the sharpest acceleration in sub-Saharan Africa and Southeast Asia, regions where CGM remains cost-prohibitive. These rising numbers create structural demand that anchors the blood glucose test strips market even as technology evolves.

Emphasis on Self-Monitoring and Preventive Care

The American Diabetes Association's 2026 Standards of Care newly recommend self-monitoring for non-insulin Type 2 patients experiencing glycemic variability, broadening the addressable patient pool by an estimated 30% (diabetes.org). Medicare's 2024 pilot authorizes 100 strips every quarter for high-risk non-insulin users, potentially covering 2 million additional beneficiaries. Across Europe, primary-care physicians now conduct quarterly HbA1c testing, supplemented by at-home strip checks, which has increased per-patient strip use from 50 to 150 annually in the United Kingdom. Large U.S. employers, such as Johnson & Johnson, distribute free meters and 200 strips annually to employees with elevated fasting glucose, turning preventive screenings into recurring purchases. Collectively, these policies cultivate daily testing habits that sustain the blood glucose test strips market.

Rising Adoption of Continuous Glucose Monitoring Systems

Abbott's FreeStyle Libre Rio, cleared in July 2024 at USD 55 per 14-day sensor, brings CGM within price parity for heavy strip users who test 4 times or more daily. Dexcom's G7 extends wear time to 15 days and costs USD 1,460 annually, now reimbursed by many Medicare Advantage plans without prior authorization. The ADA's 2026 Standards recommend CGM for all intensive insulin regimens, accelerating the migration among the 1.6 million U.S. Type 1 patients who historically consumed up to 10 strips a day. Senseonics' 365-day implantable sensor eliminates finger-stick calibration, offering a zero-strip alternative for affluent users willing to pay USD 3,500 upfront. As CGM pricing falls and coverage widens, strip volumes in high-income segments will continue to shrink, curbing overall growth in the blood glucose test strips market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Enhancements in Enzymatic Strip Chemistry

- Integration of Bluetooth-Enabled Smart Meters with Telehealth Platforms

- Price Sensitivity in Low-Income Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thick film formats accounted for 46.43% of the blood glucose test strips market in 2025, due to production costs of less than USD 0.08 and an accuracy of +-10%. Optical strips, however, are on track for a 7.54% CAGR through 2031 as colorimetric methods appeal to clinics without reliable electricity, particularly in sub-Saharan Africa and rural Asia. The blood glucose test strips market size for optical products is projected to widen as the World Health Organization's 2024 Essential Diagnostics List prioritizes battery-free devices.

Electrochemical technology is evolving as well. Roche's porous-carbon electrode wicks blood in under two seconds, marrying the costs of thick films with the speed of thin films. Abbott's dual-enzyme system removes maltose interference for dialysis patients, and the FDA's stricter +-10% guidance from 2024 will phase out sub-standard generics, channeling demand toward compliant brands. This competitive interplay keeps the blood glucose test strips market dynamic even as optical entries rise.

Type 2 diabetics generated 67.54% of strip consumption in 2025, illustrating that CGM remains economically unjustified for patients on oral drugs or lifestyle therapy. Gestational and other types of diabetes are growing at a 7.65% CAGR, driven by universal pregnancy screening that introduces three-strip checks per test episode, resulting in millions of additional annual uses in the United States and India.

The blood glucose test strips market share for Type 1 users is shrinking as CGM penetration hit 68% in 2025. Yet, the overall blood glucose test strips market size continues to rise because Type 2 comprises the vast majority of the global diabetic population. Public-health programs targeting undiagnosed adults further enlarge demand, counterbalancing CGM-led attrition in intensive-insulin cohorts.

Geography Analysis

North America accounted for 43.56% of the 2025 global revenue, primarily driven by Medicare Part B coverage, which guarantees demand for approximately 2.96 billion strips annually among insulin users. Competitive bidding trimmed reimbursement by 28% between 2021 and 2024, yet expanded eligibility to high-HbA1c non-insulin patients, preserving volume despite lower unit prices. Canada's public formularies cap quantities - Ontario allows 3,000 strips yearly for Type 1 but only 400 for Type 2 - curbing upside despite high disease prevalence. U.S. FDA accuracy rules, effective in 2024, are expected to consolidate the market around Abbott, Roche, and Ascensia, pushing low-cost generics out of pharmacies.

Asia-Pacific is projected to post the fastest 6.64% CAGR through 2031 on the back of China's 140.9 million and India's 101 million patient bases. India's Production Linked Incentive program subsidizes 5-7% of incremental sales, coaxing Sinocare and Bionime to build two billion-strip plants, which will lower public-sector per-unit costs and increase usage in rural clinics. China's regulator cut approval times to nine months in 2024, enabling domestic firms to launch 12 new strip lines that undercut imports by up to 40%. Japan's 12% reimbursement reduction in 2024 pressured margins, driving ARKRAY and Terumo to shift manufacturing to lower-cost Southeast Asian hubs.

Europe, the Middle East, and Africa, along with South America, collectively account for the remainder of global demand; however, fragmented reimbursement and price sensitivity restrain growth. German public insurers are forcing pharmacists to dispense the cheapest strip brand, thereby compressing Roche and Abbott's combined market share from 68% to 54% by 2025. The United Kingdom now limits non-insulin users to two strips per day, but quarterly HbA1c tests, paired with at-home checks, help maintain baseline consumption. Brazil covers strips for insulin users but 42% of Type 2 patients test less than weekly due to USD 0.60 per-unit prices. Sub-Saharan African patients often forgo recommended testing frequencies as strips can cost up to 10% of daily wages, highlighting affordability as the primary ceiling on the blood glucose test strips market in low-income regions.

- 77 Elektronika Kft.

- Abbott Laboratories

- Acon Laboratories

- AgaMatrix

- Arkray

- Ascensia Diabetes Care Holdings AG.

- Bionime

- Roche

- i-SENS Inc.

- LifeScan IP Holdings, LLC.

- Nova Biomedical

- OK Biotech Co. Ltd.

- Omron Healthcare Co. Ltd.

- Prodigy Diabetes Care, LLC

- Rossmax

- SD Biosensor Inc.

- Sinocare

- TaiDoc Technology

- Trividia Health

- Ypsomed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Diabetes Prevalence

- 4.2.2 Emphasis on Self-Monitoring and Preventive Care

- 4.2.3 Technological Enhancements in Enzymatic Strip Chemistry

- 4.2.4 Expanding Insurance Reimbursement for SMBG Consumables

- 4.2.5 Localization of Strip Manufacturing Driven by Supply-Chain Incentives

- 4.2.6 Integration of Bluetooth-Enabled Smart Meters with Telehealth Platforms

- 4.3 Market Restraints

- 4.3.1 Rising Adoption of Continuous Glucose Monitoring Systems

- 4.3.2 Price Sensitivity in Low-Income Regions

- 4.3.3 Enzymatic Raw Material Supply Bottlenecks

- 4.3.4 Regulatory Push Toward Eco-Friendly Strip Disposal Standards

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Thick Film Strips

- 5.1.2 Thin Film Strips

- 5.1.3 Optical / Photometric Strips

- 5.2 By Diabetes Type

- 5.2.1 Type 1 Diabetes

- 5.2.2 Type 2 Diabetes

- 5.2.3 Gestational and Others

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Homecare / Personal Use

- 5.3.3 Diagnostic Laboratories

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest Of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest Of Asia-Pacific

- 5.5.4 Middle East And Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest Of Middle East And Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest Of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 77 Elektronika Kft.

- 6.3.2 Abbott Laboratories

- 6.3.3 ACON Laboratories Inc.

- 6.3.4 AgaMatrix

- 6.3.5 ARKRAY Inc.

- 6.3.6 Ascensia Diabetes Care Holdings AG.

- 6.3.7 Bionime Corporation

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 i-SENS Inc.

- 6.3.10 LifeScan IP Holdings, LLC.

- 6.3.11 Nova Biomedical

- 6.3.12 OK Biotech Co. Ltd.

- 6.3.13 Omron Healthcare Co. Ltd.

- 6.3.14 Prodigy Diabetes Care, LLC

- 6.3.15 Rossmax International Ltd

- 6.3.16 SD Biosensor Inc.

- 6.3.17 Sinocare Inc.

- 6.3.18 TaiDoc Technology Corporation

- 6.3.19 Trividia Health Inc.

- 6.3.20 Ypsomed AG

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment