PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849961

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849961

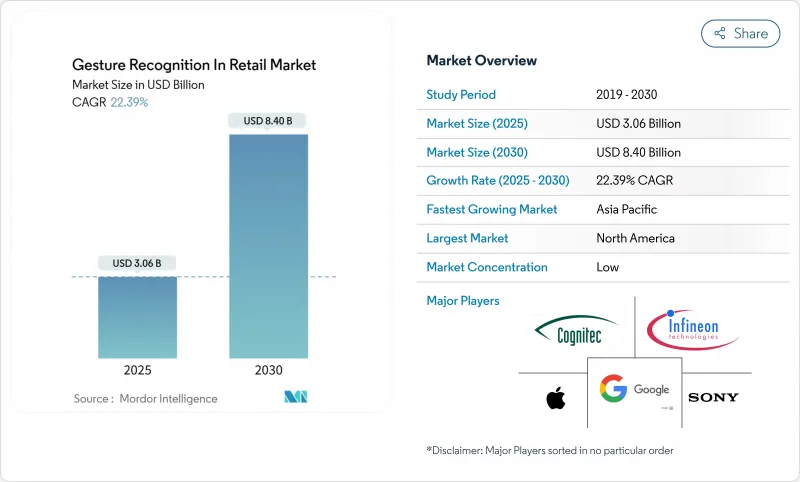

Gesture Recognition In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The gesture recognition in retail market size reached USD 3.06 billion in 2025 and is forecast to climb to USD 8.40 billion by 2030, advancing at a 22.4% CAGR.

Rising labor shortages, sustained demand for contact-free journeys, and the pairing of edge AI with millimeter-wave radar now allow through-shelf gesture detection that works without a direct camera view. Retailers gain richer in-aisle analytics, while consumer packaged goods brands monetize the resulting behavioral data streams. Hardware costs continue to fall as 3-D sensing and AI chipsets integrate into mainstream point-of-sale devices. Regulatory clarity in major markets and maturing privacy-preserving architectures further de-risk large-scale roll-outs. Collectively, these dynamics support sustained double-digit expansion for the gesture recognition in retail market through the decade.

Global Gesture Recognition In Retail Market Trends and Insights

Rising Demand for Contact-Free Shopping Experiences

Pandemic-era behaviors solidified consumer expectations for touchless journeys, and major European grocers have validated full-scale computer-vision supermarkets exceeding 1,000 m2 footprints. Retailers report measurable reductions in average checkout time and greater customer throughput, translating into higher basket sizes and repeat visits. Competitive pressure now pushes even mid-tier chains to evaluate gesture-enabled front-end redesigns. As more operators deploy privacy-preserving edge architectures, adoption accelerates without added cloud fees. These developments reinforce the near-term growth outlook for the gesture recognition in retail market.

Increasing Penetration of 3-D Sensing and AI Chips in Retail Devices

Edge silicon now executes real-time gesture inference locally, removing bandwidth constraints and cutting latency. Recent prototypes pairing 3-D depth sensors with dedicated machine-learning cores showed 99.8% gesture accuracy across 18 classes, even under variable lighting. Asian OEMs leverage scale manufacturing to push unit prices below USD 20, opening access for regional grocers and convenience stores. Lower cost of ownership and ease of retrofitting existing lanes help broaden the reachable base of the gesture recognition in retail market. Joint reference designs from chip suppliers and solution integrators also reduce integration effort for retailers with limited in-house engineering talent.

Algorithmic Complexity and Accuracy Variance in Live-Store Environments

Retail settings introduce occlusions, reflective surfaces, and crowd density that cut gesture accuracy when compared with lab results, particularly for customers carrying bags or wearing gloves. Bias across age groups and body mobility still appears in computer-vision models, raising inclusion concerns. Continuous re-training regimes and larger annotated data sets drive deployment cost upward. Merchants must tune sensor layouts per store to preserve acceptable performance, complicating multi-format roll-outs. Until middleware platforms abstract this complexity, some chains remain cautious, tempering the short-term expansion of the gesture recognition in retail market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart-Retail and Autonomous-Store Formats

- Advancements in mm-wave and UWB Radar Enabling Through-Shelf Gestures

- Privacy and Regulatory Push-Back on Continuous Vision Tracking

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Touch-based platforms represented 78.1% of gesture recognition in retail market share in 2024 as retailers favored proven systems bolted onto legacy lanes. Even so, the touch-less segment is set to record a 24.1% CAGR through 2030, underscoring a shift toward hygienic and seamlessly integrated store journeys. Pilots by big-box clubs that clear members via camera recognition at exits illustrate how touch-less can replace manual receipt checks. Hardware vendors now integrate radar sensors alongside RGB-D cameras, trimming bill-of-materials and closing the precision gap that once favored touch-based panels. As deployment confidence rises, the gesture recognition in retail market size tied to touch-less offerings is projected to exceed USD 3 billion by 2030, doubling its 2024 base.

Retailers increasingly view touch-less gesture recognition as a brand differentiator that elevates experience, especially in high-margin segments such as luxury fashion and consumer electronics showrooms. Meanwhile, touch-based platforms remain relevant for use cases that demand pinpoint accuracy, such as signature capture or build-to-order kiosks. Those dual pathways indicate a coexistence model rather than outright substitution, allowing suppliers to position modular solutions that scale with client needs. Continued iterations of neural processing units will likely lower latency to sub-30 milliseconds, preserving intuitive interactions and encouraging further penetration of the gesture recognition in retail market.

Hand and finger inputs dominated, accounting for 66.8% of the gesture recognition in retail market size in 2024, thanks to consumers already conditioned by smartphones. Full-body systems, however, register a 23.4% CAGR to 2030 as faster GPUs in edge boxes decode skeletal movement for immersive display walls and aisle-level analytics. Head-centric micro-gestures found early adoption in convenience stores and petrol marts where hands are busy handling goods. Research prototypes combining voice and gesture score higher for intent accuracy, implying a multimodal trajectory for the gesture recognition in retail market.

Wearable bands that pick up neural or muscle signals bring an additional interaction layer for differently abled shoppers, broadening accessibility. Retailers use full-body heat maps to pinpoint hotspots and redesign aisles, demonstrating that gesture data can unlock operations value beyond front-end checkout. The expanding use-case set underscores why the gesture recognition in retail industry continues to invest in advanced pose estimation algorithms despite the higher compute requirement.

The Gesture Recognition in Retail Market Report is Segmented by Technology (Touch-Based Gesture Recognition and Touch-Less Gesture Recognition), Interaction Mode (Hand and Finger Gestures, Head / Nod Gestures, and More), Function (In-Store Customer Engagement Displays, and More), Retail Format (Supermarkets and Hypermarkets, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America, with 36.5% share of the gesture recognition in retail market size in 2024, benefits from early adopter big-box chains and a comparatively permissive biometric regime. Federal guidelines remain less restrictive than Europe's, enabling chain-wide pilots that rapidly scale when ROI is proven. Over 500 grocery sites now run camera-only exit checkout, reinforcing the region's leadership.

Asia-Pacific posts the highest 22.8% CAGR through 2030 as Chinese payment ecosystems and Japanese unmanned formats integrate gesture recognition into end-to-end store automation. Government retail-digitization grants lower upfront cost barriers, while consumers show strong acceptance of biometric processes. Local hardware manufacturing density shortens supply chains and accelerates iteration cycles, further catalyzing uptake.

Europe follows with privacy-compliant architectures that blend edge processing and encrypted cloud synchronization to satisfy the EU AI Act. Multinational grocers test gesture-enabled mega-stores across Germany, France, and the Nordics, providing blueprints for pan-EU roll-outs. Emerging regions in Latin America and the Middle East start from smaller bases but see double-digit adoption as global vendors introduce turnkey packages targeted at mid-sized supermarket groups. This cascade effect supports a geographically diversified enlargement of the gesture recognition in retail market.

- Apple Inc

- Google LLC

- Microsoft Corporation

- Intel Corporation

- Infineon Technologies AG

- Sony Group Corp

- Omron Corporation

- Cognitec Systems GmbH

- Crunchfish AB

- Elliptic Labs ASA

- GestureTek Inc

- Ultraleap Ltd

- Synaptics Incorporated

- Qualcomm Technologies Inc

- PointGrab Ltd

- Neonode Inc

- Cipia Vision Ltd

- Samsung Electronics Co Ltd

- Microchip Technology Inc

- STMicroelectronics N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for contact-free shopping experiences

- 4.2.2 Increasing penetration of 3-D sensing and AI chips in retail devices

- 4.2.3 Expansion of smart-retail and autonomous-store formats

- 4.2.4 Advancements in mm-wave and UWB radar enabling through-shelf gestures

- 4.2.5 Monetisation of in-aisle gesture analytics for CPG brands

- 4.2.6 Integration of AR smart-glasses bridging online and in-store journeys

- 4.3 Market Restraints

- 4.3.1 Algorithmic complexity and accuracy variance in live-store environments

- 4.3.2 Privacy and regulatory push-back on continuous vision tracking

- 4.3.3 Edge-network latency causing gesture misfires at checkout

- 4.3.4 Electromagnetic interference from dense in-store IoT deployments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Touch-based Gesture Recognition

- 5.1.2 Touch-less Gesture Recognition

- 5.2 By Interaction Mode

- 5.2.1 Hand and Finger Gestures

- 5.2.2 Head / Nod Gestures

- 5.2.3 Full-Body Gestures

- 5.2.4 Multimodal (Gesture and Voice)

- 5.3 By Function

- 5.3.1 In-Store Customer Engagement Displays

- 5.3.2 Checkout / Point-of-Sale and Payments

- 5.3.3 Store Operations, Inventory and Analytics

- 5.4 By Retail Format

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Apparel and Department Stores

- 5.4.4 Specialty Retailers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 Intel Corporation

- 6.4.5 Infineon Technologies AG

- 6.4.6 Sony Group Corp

- 6.4.7 Omron Corporation

- 6.4.8 Cognitec Systems GmbH

- 6.4.9 Crunchfish AB

- 6.4.10 Elliptic Labs ASA

- 6.4.11 GestureTek Inc

- 6.4.12 Ultraleap Ltd

- 6.4.13 Synaptics Incorporated

- 6.4.14 Qualcomm Technologies Inc

- 6.4.15 PointGrab Ltd

- 6.4.16 Neonode Inc

- 6.4.17 Cipia Vision Ltd

- 6.4.18 Samsung Electronics Co Ltd

- 6.4.19 Microchip Technology Inc

- 6.4.20 STMicroelectronics N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment