PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850051

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850051

Risk Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

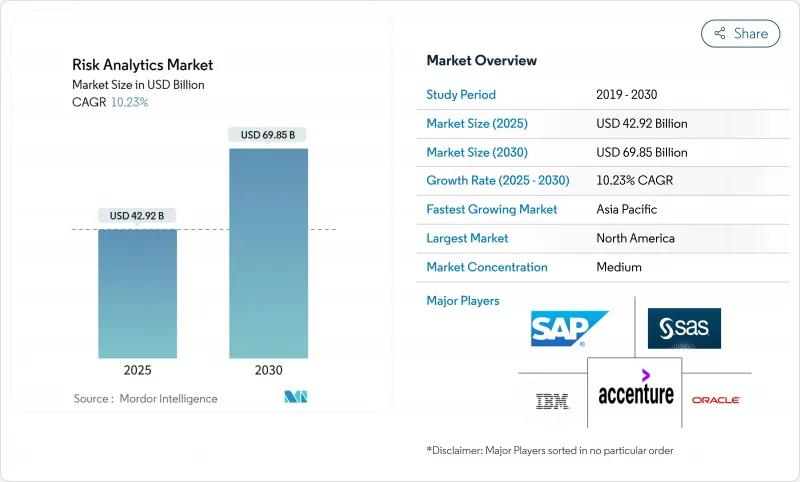

The global risk analytics market is valued at USD 42.92 billion in 2025 and is projected to reach USD 69.85 billion by 2030 at a 10.2% CAGR.

Heightened regulatory scrutiny, real-time fraud exposure on instant-payment rails, and mandatory climate-risk disclosure are making advanced analytics a strategic necessity rather than a discretionary IT spend. Financial institutions are phasing out rule-based tools in favor of AI-driven platforms that evaluate millions of data points within milliseconds to support capital optimization, fraud interdiction, and climate scenario modeling. Cloud-native architectures, quantum-resistant algorithms, and unified data fabrics are cutting total cost of ownership while enabling parallel compliance reporting across jurisdictions. The convergence of these forces is reshaping vendor strategies toward platform-as-a-service delivery that merges software, consulting, and managed operations.

Global Risk Analytics Market Trends and Insights

Real-time fraud surge in instant-payment rails

Instant settlement environments expose banks to transaction-level attacks that overwhelm batch fraud tools. Global real-time payment volumes are on track to hit 575 billion transactions by 2028, forcing institutions to deploy millisecond analytics that blend behavioral biometrics, device intelligence, and network analytics while maintaining false-positive rates below 1%. The United Kingdom's mandatory reimbursement rule for authorized push-payment fraud strengthens the economic case for AI-native platforms that score transactions as they occur. Vendors that can combine streaming data ingestion, graph analytics, and model governance within a single cloud-native stack hold a decisive edge.

Heightened post-Basel IV capital-adequacy scrutiny

The EU's January 2025 Basel IV rollout and FINMA's enhanced operational-risk ordinances oblige multinational banks to run several risk-weighted asset calculations in parallel. Cloud-based Monte-Carlo engines allow near real-time capital optimization across diverging rulesets while satisfying BCBS 239 data-aggregation tests. As regulators intensify on-site data audits, demand for unified data lineage, audit trails, and scenario libraries accelerates the migration toward service-rich platforms that embed regulatory logic natively.

Acute talent shortage in model-risk governance

Fifty-four percent of banks report gaps in quantitative validation skills, delaying model releases and inflating compliance costs. Salary inflation is steepest for specialists who combine statistics, regulatory insight, and AI competence. Institutions are adopting automated validation toolkits that replay production data and issue governance alerts, but supervisors still require human sign-off. Vendors that bundle workflow, documentation, and auto-testing capabilities mitigate the constraint yet cannot fully replace scarce expertise.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory climate-risk disclosure

- AI-powered credit scoring for thin-file borrowers

- Rising SaaS subscription fatigue among mid-tiers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Market share data show Solutions at 65% in 2024, yet the Services arm is expanding faster at 11.8% CAGR. The risk analytics market size tied to consulting, implementation, and managed operations grows as banks confront AI governance, climate stress testing, and quantum-risk modeling. Service firms help integrate advanced engines with legacy cores while aligning outputs to jurisdictional templates. In parallel, core software evolves toward low-code configurability, natural language front-ends, and quantum-resistant libraries.

Ongoing regulatory change keeps customers reliant on external specialists for model inventory curation, documentation, and validation. Managed services covering data quality, scenario libraries, and real-time monitoring reduce overhead for mid-tier players. As a result, spending tilts toward recurring service contracts even where perpetual licenses remain in place. Vendors that fuse software upgrades with outcome-based service commitments guard renewals and upsell opportunities.

On-premises systems retain 67.6% share in 2024 as institutions guard sensitive data against extraterritorial access. Yet a 12.1% CAGR for cloud indicates decisive migration momentum, raising the risk analytics market value delivered via SaaS and platform-as-a-service models. Cloud deployments support elastic compute bursts for intraday stress testing, real-time fraud scoring, and high-frequency market-risk recalculations. Providers of sovereign-cloud zones ease data-residency objections in Europe, the Middle East, and Asia.

Hybrid architectures dominate transition roadmaps. Legacy credit engines remain on-premises while AI inference layers, visualization dashboards, and batch reporting shift to cloud micro-services. Clients use multi-cloud orchestrators to avoid lock-in and align workloads with latency, cost, and data-localization constraints. Solutions that embed workload-placement logic and cross-cloud cost analytics capture wallet share as institutions refine resource allocation strategies.

The Risk Analytics Market Report is Segmented by Component (Solution and Services), Deployment (On-Premises and Cloud), Risk Type (Credit, Operational, and More), Application (Fraud Detection and AML, Stress Testing and Scenario-Analysis, and More), End-User Industry (BFSI, Healthcare and Life-Sciences, and More), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), and Geography.

Geography Analysis

North America held 38.6% of revenue in 2024, underpinned by strict supervisory regimes and early hyperscale-cloud adoption. The Federal Reserve's climate guidance and Basel III endgame rules sustain spending on capital optimization, stress testing, and data lineage solutions. U.S. institutions also pilot quantum-resistant encryption to future-proof payment rails, supported by IBM's multi-billion dollar quantum roadmap.

Europe commands significant share and shapes regulatory templates worldwide. Implementation of the Digital Operational Resilience Act in 2025 obliges banks to integrate ICT-risk analytics with traditional financial-risk metrics. The bloc's leadership on ESG rules propels climate-scenario spending, while BCBS 239 compliance pushes real-time data aggregation investments. Fragmented member-state rules raise demand for platforms that map multiple reporting schemas onto consistent data models.

Asia-Pacific is the fastest-growing region at 11.5% CAGR. India's Unified Payments Interface processes billions of monthly transfers, heightening real-time fraud needs. China deepens supply-chain finance analytics and readies digital currency risk frameworks. Southeast Asian markets accelerate credit-scoring for first-time borrowers using alternative data. Regulators adopt sandbox schemes that speed vendor approvals, fuelling rapid deployment of scalable cloud offerings adapted to local data-localization norms.

- SAS Institute Inc.

- IBM Corporation

- Oracle Corporation

- SAP SE

- Moody's Analytics Inc.

- FIS Global

- NICE Actimize

- Fair Isaac Corp (FICO)

- AxiomSL / Adenza Group

- Capgemini SE

- Accenture plc

- OneSpan Inc.

- Risk Edge Solutions

- Provenir Inc.

- Verisk Analytics

- LexisNexis Risk Solutions

- Riskonnect Inc.

- Dun and Bradstreet Holdings

- Nasdaq Risk Platform

- Palantir Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-time fraud surge in instant-payment rails

- 4.2.2 Heightened post-Basel IV capital-adequacy scrutiny

- 4.2.3 Mandatory climate-risk disclosure

- 4.2.4 AI-powered credit scoring for thin-file borrowers

- 4.2.5 Multi-cloud risk-data fabrics cut TCO by above 25%

- 4.2.6 Quantum-computing threat to legacy crypto-algos

- 4.3 Market Restraints

- 4.3.1 Acute talent shortage in model-risk governance

- 4.3.2 Rising SaaS subscription fatigue among mid-tiers

- 4.3.3 Vendor-lock-in concerns over proprietary ML stacks

- 4.3.4 Inconsistent ESG taxonomies across jurisdictions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Risk-calculation engines

- 5.1.1.2 Risk reporting and dashboards

- 5.1.1.3 ETL / Data-management hubs

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Integration and Implementation

- 5.1.2.3 Managed / BPO Services

- 5.1.1 Solution

- 5.2 By Deployment

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Risk Type

- 5.3.1 Credit

- 5.3.2 Operational

- 5.3.3 Liquidity

- 5.3.4 Compliance / RegTech

- 5.3.5 Climate and ESG

- 5.4 By Application

- 5.4.1 Fraud Detection and AML

- 5.4.2 Stress Testing and Scenario-Analysis

- 5.4.3 Model-Risk Management

- 5.4.4 Cyber-Risk Analytics

- 5.4.5 Supply-chain / Third-party Risk

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life-sciences

- 5.5.3 Retail and E-commerce

- 5.5.4 Energy and Utilities

- 5.5.5 IT and Telecom

- 5.5.6 Others

- 5.6 By Organisation Size

- 5.6.1 Large Enterprises

- 5.6.2 Small and Medium Enterprises (SMEs)

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia and New Zealand

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAS Institute Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 Moody's Analytics Inc.

- 6.4.6 FIS Global

- 6.4.7 NICE Actimize

- 6.4.8 Fair Isaac Corp (FICO)

- 6.4.9 AxiomSL / Adenza Group

- 6.4.10 Capgemini SE

- 6.4.11 Accenture plc

- 6.4.12 OneSpan Inc.

- 6.4.13 Risk Edge Solutions

- 6.4.14 Provenir Inc.

- 6.4.15 Verisk Analytics

- 6.4.16 LexisNexis Risk Solutions

- 6.4.17 Riskonnect Inc.

- 6.4.18 Dun and Bradstreet Holdings

- 6.4.19 Nasdaq Risk Platform

- 6.4.20 Palantir Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment