PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850068

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850068

Automotive Rain Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

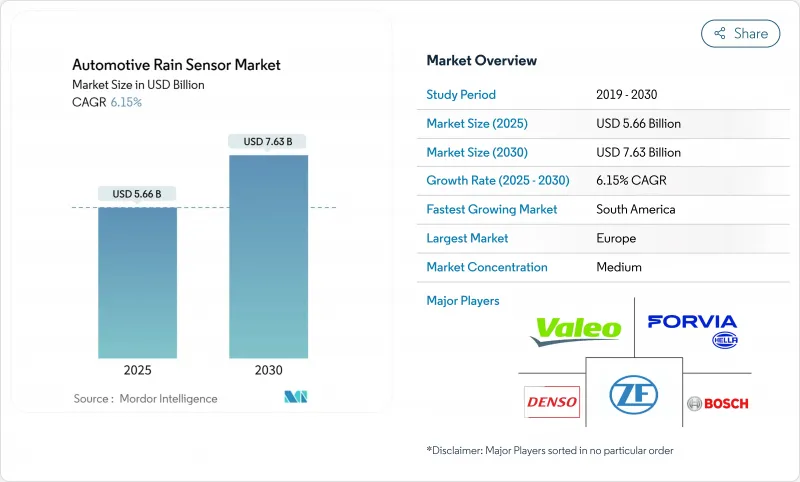

The automotive rain sensor market currently stands at USD 5.66 billion in 2025 and is predicted to reach roughly USD 7.63 billion by 2030, reflecting a 6.15% CAGR.

Steady electrification, rising Level 2+ driver-assistance adoption, and regulatory momentum continue to shift rain sensors from comfort add-ons to safety-critical perception inputs. ADAS feature bundling, semiconductor miniaturization, and subscription-ready software stacks are enlarging the addressable base, while cost-down MEMS innovation is broadening access for volume segments. Increased supplier competition from chip makers is also compressing hardware margins but accelerating functional upgrades through integrated optical, capacitive, and humidity modules. Collectively, these forces sustain a multi-year transformation trajectory for the automotive rain sensor market as OEMs reshape vehicle electrical architectures around centralized, over-the-air-update-capable domains.

Global Automotive Rain Sensor Market Trends and Insights

Rising ADAS Penetration Mandates Multi-Function Environmental Sensing

Level 2+ and Level 3 perception stacks require precise raindrop, light, and fog data to keep camera lenses and LiDAR windows clear, recasting the sensor from a comfort extra into a core safety enabler. European OEM programs pair optical rain sensors with humidity and light channels on a single PCB for reduced harness weight and unified diagnostics. Chinese brands replicate the architecture to meet forthcoming NCAP visibility scoring, while North American truck makers embed rain detection in forward-vision clusters to extend automatic emergency braking uptime. High-resolution CCD arrays improve droplet classification, feeding fusion software that modulates wiper speed, adaptive headlights, and defogger logic in one control loop. Consequently, procurement teams now benchmark performance against radar-camera synergy metrics rather than wiper latency alone, making multi-sensor wins pivotal to Tier 1 revenue pipelines.

Electrification & Higher Onboard Voltage Architectures Accelerate Adoption

E-platforms working at 400 V and 800 V offer stable power headroom for signal-processing ASICs and laser-trimmed VCSEL emitters that outperform 12 V counterparts under high-humidity transients. Centralized compute domains pull raw droplet vectors over secure CAN-FD links into zone controllers where machine-learning models refine wipe timing, extending blade life, and trimming HVAC load. Over-the-air firmware releases let OEMs iteratively sharpen detection thresholds, opening pay-per-use revenue tiers tied to predictive maintenance alerts. Battery-electric brands, therefore, market rain sensors as energy-management assets, reducing window-defog cycles by up to 6%, rather than passive glass accessories.

High Price Sensitivity in Entry-Level A/B-Segment Cars

Cost-led platforms in India, parts of ASEAN, and Latin America allocate less than USD 75 for the entire instrument-panel electronics stack, leaving marginal headroom for a USD 25-30 rain-sensing module. Domestic content rules in India amplify import tariffs on unlocalized PCBAs, compressing Tier 1 profitability and slowing take rates. OEMs resort to manual-variable-intermittent wipers in sub-4-m vehicles until integrated MEMS pricing drops below USD 15. Suppliers that secure local glass-bonding partnerships can shave freight surcharges, but low-volume orders currently deter such CAPEX outlays.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Automatic Wiper Systems

- Rising Consumer Demand for Comfort & Convenience Features

- Shortage of Automotive-Grade Photodiodes & VCSELs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive rain sensor market size for passenger cars captured 71.23% share in 2024, and is expected to lead at a robust 6.55% CAGR through 2030. Sedan programs maintain consistent attach rates across trim lines, yet hatchbacks remain price-gated to upper variants. Fleets of light commercial vans now specify automatic wiping to minimize driver distraction and insurance claims, though medium trucks lag because of retrofit complexities. Demand alignment shows that every 10-point uptick in SUV mix raises system-average BOM ceiling by USD 4, supporting margin retention for Tier 1s. Over the forecast period, SUVs' larger windshield area drives higher droplet-noise in capacitive arrays, sustaining OEM preference for optical architectures that maintain +-2 ml sensitivity accuracy in heavy downpours.

Passenger-car refresh cycles grant slower but steadier volume accrual compared with high-churn small commercial fleets. Fleet operators investigating telematics report 7% lower windshield repair claims once predictive wipe analytics are activated, strengthening business cases. Overall, SUV proliferation ensures the automotive rain sensor market remains skewed toward feature-rich packages, balancing the lower margins of high-volume hatchbacks.

Optical CCD/CMOS devices controlled 81.64% of 2024 revenue owing to proven signal-to-noise fidelity. With the top five optical controller ASICs already at silicon-revision B or later, cost curves flatten, giving MEMS entrants a price-to-performance opening. Capacitive / MEMS-based devices will clock an 8.83% CAGR as they sidestep glass-coupling tolerances, ideal for vehicles using advanced UV-blocking laminated windshields. Infrared-reflective hybrids capture niche programs needing anti-icing credibility below -25 °C, albeit at higher per-unit cost.

Strategy roadmaps show MEMS suppliers bundling ambient-light sensors and IR proximity in shared die space, trimming PCB footprint by 35%. Conversely, optical incumbents shield volumes by embedding AI-edge inference cores, enabling self-calibrating droplet recognition that sustains specification leadership. Coexistence rather than displacement defines the horizon: optical retains premium and severe-duty niches; MEMS drives democratization.

The Automotive Rain Sensors Market Report is Segmented by Vehicle Type (Passenger Cars [Hatchback, Sedan, and More] and Commercial Vehicles (Light Commercial Vehicle (LCV) and More), Technology (Optical (CCD/CMOS) and More), Sales Channel (OEM-Installed and Aftermarket Retrofit), Application (ADAS Sensor Fusion Modules, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Europe's 37.84% share reflects strict UNECE visibility norms and 2025 NCAP scoring that awards two safety points for rain-light-humidity fusion, cementing sensor fitment as an entitlement across B-segment hatchbacks upward. The continent's established premium mix also ensures high-margin optical arrays dominate. South America, led by Brazil's volume OEM hubs in Sao Paulo, is the fastest climber with a 10.33% CAGR. Consumer upgrades from entry to compact SUVs introduce room in the BOM for automated wiping, while federal incentives to localize electronic content spur sensor-housing molding ventures near Manaus.

Asia-Pacific delivers nuanced dynamics. China's New Car Evaluation Program will credit automated visibility management starting in 2027, anchoring stable shipments within a manufacturing base already scaling 25 million vehicles yearly. Hindrances lie in India and parts of ASEAN, where taxation on imported electronics inflates cost. Nonetheless, EV push grants rain sensors renewed relevance: Chinese-built sub-USD 15,000 micro-EVs that export to Thailand and Indonesia include basic capacitive sensors to ease right-hand-drive adaptation. Hence, Asia-Pacific remains both the largest growth reservoir and the most fragmented battlefield.

North America's uptake is steady rather than spectacular, yet high average transaction prices allow complex sensor-fusion packages on mainstream pickups and SUVs. Over-the-air update culture seeds subscription models for predictive windshield maintenance, producing recurring revenues that temper hardware commoditization.

- HELLA GmbH & Co. KGaA

- Valeo SA

- DENSO Corporation

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- STMicroelectronics N.V.

- Analog Devices Inc.

- ams-OSRAM AG

- onsemi

- Hamamatsu Photonics K.K.

- Sensata Technologies Inc.

- Melexis NV

- Texas Instruments Inc.

- Panasonic Holdings Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ADAS penetration mandates multi-function environmental sensing (rain, light, fog)

- 4.2.2 Electrification & higher onboard voltage architectures accelerate adoption of solid-state optical rain sensors

- 4.2.3 Regulatory push for automatic wiper systems

- 4.2.4 Rising consumer demand for comfort & convenience features across mid-segment vehicles

- 4.2.5 Integration of windshield head-up-display (HUD) modules requires cleanliness sensing (under-reported)

- 4.2.6 Automotive over-the-air updates unlock new revenue via subscription-based wiper automation (under-reported)

- 4.3 Market Restraints

- 4.3.1 High price sensitivity in entry-level A/B-segment cars limits sensor attach-rates in India & ASEAN

- 4.3.2 Shortage of automotive-grade photodiodes & VCSELs

- 4.3.3 Windshield design heterogeneity complicates optical coupling & raises validation cost (under-reported)

- 4.3.4 Competition from camera-only ADAS stacks promising software-defined rain detection (under-reported)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchback

- 5.1.1.2 Sedan

- 5.1.1.3 SUVs and crossovers

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Vehicle (LCV)

- 5.1.2.2 Medium and Heavy Commercial Vehicle

- 5.1.1 Passenger Cars

- 5.2 By Technology

- 5.2.1 Optical (CCD/CMOS)

- 5.2.2 Infra-red Reflective

- 5.2.3 Capacitive / MEMS-based

- 5.3 By Sales Channel

- 5.3.1 OEM-Installed

- 5.3.2 Aftermarket Retrofit

- 5.4 By Application

- 5.4.1 Automatic Wiper Control

- 5.4.2 Integrated Rain-Light-Humidity Sensing

- 5.4.3 ADAS Sensor Fusion Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 HELLA GmbH & Co. KGaA

- 6.4.2 Valeo SA

- 6.4.3 DENSO Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Robert Bosch GmbH

- 6.4.6 STMicroelectronics N.V.

- 6.4.7 Analog Devices Inc.

- 6.4.8 ams-OSRAM AG

- 6.4.9 onsemi

- 6.4.10 Hamamatsu Photonics K.K.

- 6.4.11 Sensata Technologies Inc.

- 6.4.12 Melexis NV

- 6.4.13 Texas Instruments Inc.

- 6.4.14 Panasonic Holdings Corp.

7 Market Opportunities & Future Outlook

- 7.1 Demand surge for combined rain-fog-light sensor modules to support L3 autonomy

- 7.2 Growth of subscription-based "feature-on-demand" wiper services post-2026

- 7.3 Localisation of sensor assembly in India, Brazil & Indonesia to bypass import duties

- 7.4 Development of hydrophobic nano-coated windshields reducing sensor calibration cycles